Here's Why You Should Hold Onto Nutrien (NTR) Stock for Now

Nutrien Ltd. NTR is expected to gain from higher demand for crop nutrients, its actions to reduce costs and strategic acquisitions amid headwinds from lower prices.

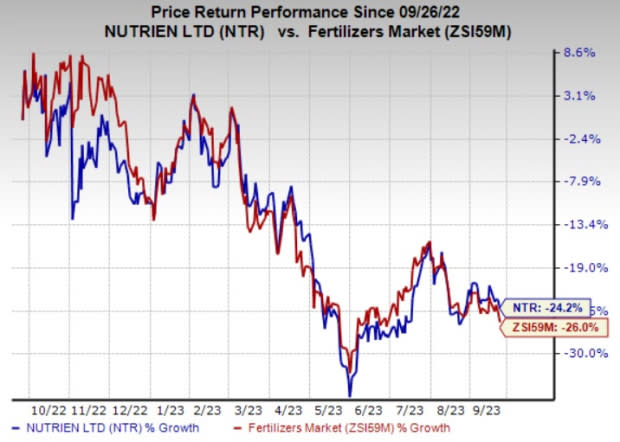

The company’s shares are down 24.2% over a year, compared with a 26% decline recorded by its industry.

Let’s find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Image Source: Zacks Investment Research

Strong Demand, Cost Reductions Aid NTR

Nutrien is well-placed to benefit from increased demand for fertilizers, backed by the strength in global agriculture markets. It is seeing strong demand in its major markets, particularly North America. Strong grower economics and higher crop commodity prices are expected to drive potash demand globally. The phosphate market is also benefiting from higher global demand and low producer and channel inventories. Demand for nitrogen fertilizer also remains healthy in major markets. Global nitrogen requirement is being driven by demand in North America, India and Brazil.

The company is also well placed to gain from acquisitions and increased adoption of its digital platform. It continues to expand its footprint in Brazil through acquisitions. The company expanded its network through the completion of 21 retail acquisitions in 2022 with a focus on expanding its Brazil network.

Cost and operational efficiency initiatives are also expected to aid the company’s performance. Nutrien remains focused on lowering the cost of production in the potash business. Moreover, the company has announced a number of strategic actions to reduce its controllable costs and boost free cash flow this year and beyond. Lower natural gas costs are also contributing to a decline in its cost of goods sold.

Weak Prices May Play Spoilsport

Lower fertilizer prices are expected weigh on the company’s performance over the near term. Prices of phosphate and potash have retreated since the back half of 2022 from their peak levels attained in the first half riding on the impacts of the Russia-Ukraine war and disruptions due to the sanctions in Belarus. Global nitrogen prices have declined since the beginning of 2023. Notably, global potash prices were under pressure in the second quarter of 2023 due to destocking in the offshore market and uncertainty surrounding the delayed Chinese potash contract settlement. Lower prices are expected to hurt NTR’s profitability in 2023.

Nutrien has lowered its full-year 2023 adjusted EBITDA guidance considering lower expected fertilizer pricing. The company now sees adjusted EBITDA of $5.5-$6.7 billion for full-year 2023, down from $6.5-$8 billion it expected earlier. The adjusted earnings per share guidance has been also lowered to $3.85-$5.60 from $5.50-$7.50. Logistical challenges such as the Port of Vancouver strike and an outage at Canpotex’s Portland terminal have also led to a downward revision in the company’s potash sales volume guidance range for 2023.

Stocks to Consider

Better-ranked stocks worth a look in the basic materials space include Carpenter Technology Corporation CRS, Hawkins, Inc. HWKN and Alamos Gold Inc. AGI.

The Zacks Consensus Estimate for current fiscal-year earnings for CRS is currently pegged at $3.48, implying year-over-year growth of 205.3%. Carpenter Technology currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Carpenter Technology has a trailing four-quarter earnings surprise of roughly 10%, on average. The stock has rallied around 110% over the past year.

Hawkins currently carrying a Zacks Rank #1. It has a projected earnings growth rate of 18.9% for the current year.

Hawkins has a trailing four-quarter earnings surprise of roughly 25.6%, on average. HWKN shares are up around 58% in a year.

Alamos Gold currently carries a Zacks Rank #2 (Buy). The Zacks Consensus Estimate for AGI's current-year earnings has been revised 7.5% upward over the past 60 days.

The Zacks Consensus Estimate for current fiscal-year earnings for Alamos Gold is currently pegged at 43 cents, implying year-over-year growth of 53.6%. AGI shares have surged around 85% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Carpenter Technology Corporation (CRS) : Free Stock Analysis Report

Alamos Gold Inc. (AGI) : Free Stock Analysis Report

Hawkins, Inc. (HWKN) : Free Stock Analysis Report

Nutrien Ltd. (NTR) : Free Stock Analysis Report