Here's Why Hold Strategy Is Apt for American Financial (AFG)

American Financial Group, Inc. AFG has been favored by investors on the back of rate increases, higher retentions in renewal business, stronger underwriting profit and improved guidance.

Growth Projections

The Zacks Consensus Estimate for American Financial’s 2024 earnings per share indicates a year-over-year increase of 4.3% from the consensus estimate of 2023. The consensus estimate for revenues is pegged at $7.84 billion, implying a year-over-year improvement of 4.2% from the consensus mark of 2023.

The consensus estimate for 2025 earnings per share indicates a year-over-year increase of 4.5% from the consensus estimate of 2024. The consensus estimate for 2025 revenues is pinned at $8.41 billion, implying a year-over-year improvement of 7.2% from the consensus mark of 2024.

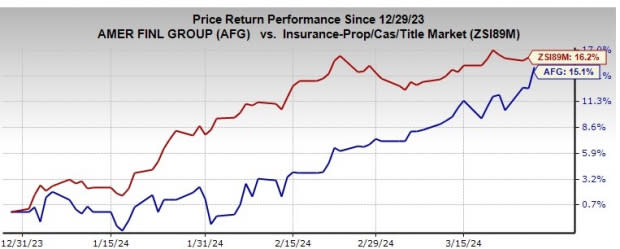

Zacks Rank & Price Performance

AFG currently carries a Zacks Rank #3 (Hold). Year to date, the stock has gained 15.1% compared with the industry’s growth of 16.2%.

Image Source: Zacks Investment Research

Style Score

American Financial has a VGM Score of B. The VGM Score helps identify stocks with the most attractive value, best growth and the most promising momentum.

Business Tailwinds

The company’s Property and Casualty (P&C) Insurance segment should benefit from business opportunities, growth in the surplus lines and excess liability businesses, rate increases and higher retentions in renewal business, which boost premium growth.

The company assumes 8% growth in net written premiums for 2024 compared with 2023. For 2024, American Financial expects that performance in line with the assumptions underlying the 2024 business plan would result in core operating earnings per share of approximately $11.

AFG witnessed average renewal pricing across the entire P&C Group. It intends to maintain satisfactory rates in P&C renewal pricing going forward. Average renewal pricing across the P&C Group, excluding workers’ compensation, grew around 7% for the fourth quarter of 2023, which was in line with renewal rates in the previous quarter. This is the 30th consecutive quarter to report overall renewal rate increases. The company expects to achieve overall renewal rate increases in excess of prospective loss ratio trends to meet or exceed targeted returns.

The insurer’s combined ratio has been better than the industry’s average for more than two decades. The underwriting profit of the insurer is likely to increase on the back of higher profit in the workers’ compensation, excess and surplus, executive liability, mergers and acquisitions liability businesses and higher underwriting profit in the trade credit and financial institutions businesses.

American Financial has successfully increased its dividends in each of the last 18 years. The robust operating profitability at the P&C segment, stellar investment performance and effective capital management support effective shareholders return. AFG expects its operations to generate significant excess capital throughout the remainder of 2024, which provides ample opportunity for additional share repurchases or special dividends over the next year.

Stocks to Consider

Some better-ranked stocks from the insurance space are HCI Group, Inc. HCI, Palomar Holdings, Inc. PLMR and Axis Capital Holdings Limited AXS. While HCI Group and Palomar Holdings sport a Zacks Rank #1 (Strong Buy) each, Axis Capital carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

HCI Group has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 522.51%. Year to date, HCI has jumped 32.2%.

The Zacks Consensus Estimate for HCI’s 2024 and 2025 earnings implies year-over-year growth of 37.9% and 11.6%, respectively, from the consensus estimate of the corresponding years.

Palomar Holdings has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 11.12%. Year to date, PLMR has rallied 51.8%.

The Zacks Consensus Estimate for PLMR’s 2024 and 2025 earnings implies year-over-year growth of 16.2% and 18%, respectively, from the consensus estimate of the corresponding years.

Axis Capital has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 102.57%. Year to date, AXS has gained 17.4%.

The Zacks Consensus Estimate for AXS’ 2024 and 2025 earnings implies year-over-year growth of 3% and 10%, respectively, from the consensus estimate of the corresponding years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Axis Capital Holdings Limited (AXS) : Free Stock Analysis Report

American Financial Group, Inc. (AFG) : Free Stock Analysis Report

HCI Group, Inc. (HCI) : Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR) : Free Stock Analysis Report