Here's Why You Should Invest in Hartford Financial (HIG) Now

The Hartford Financial Services Group, Inc. HIG has gained on growing premiums attributable to rate hikes and new business growth. Acquisitions and product launches, as well as adequate cash-generating abilities, are additional tailwinds for the stock.

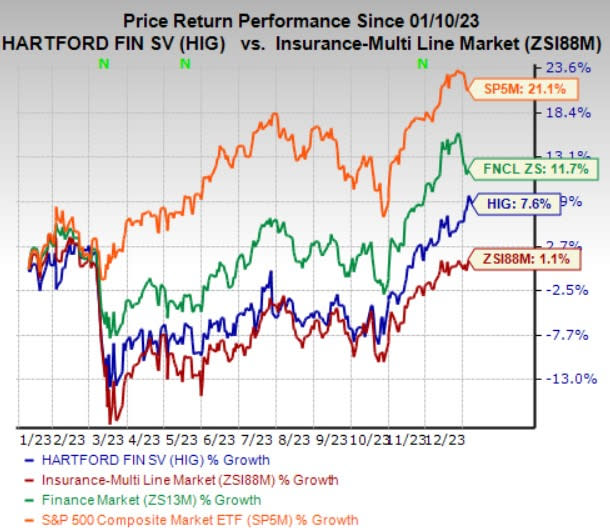

Zacks Rank & Price Performance

Hartford Financial currently carries a Zacks Rank #2 (Buy).

The stock has gained 7.6% in a year compared with the industry’s 1.1% growth. The Zacks Finance sector and the S&P 500 Composite increased 11.7% and 21.1%, respectively, in the same time frame.

Image Source: Zacks Investment Research

Rising Estimates

The Zacks Consensus Estimate for Hartford Financial’s 2023 earnings per share (EPS) is pegged at $8.14, indicating an improvement of 7.7% from the prior-year reading. The Zacks Consensus Estimate for 2023 revenues stands at $16.5 billion, implying an 8.5% increase from the prior-year actual.

The consensus mark for 2024 EPS is pegged at $9.73, suggesting 19.6% growth from the 2023 estimate. The consensus mark for 2024 revenues stands at $18 billion, which indicates a rise of 8.9% from the 2023 estimate.

HIG’s bottom line surpassed earnings estimates in three of the trailing four quarters and matched the mark once, the average surprise being 10.8%.

Solid Return on Equity

The return on equity for Hartford Financial is currently 19.1%, which is higher than the industry’s average of 13.3%. The figure substantiates the company’s efficiency in utilizing shareholders’ funds.

Key Drivers

Hartford Financial gains from strong contributions by its Commercial Lines and Group Benefits businesses. The Commercial Lines unit is aided by continued rate increases, new business growth and strong customer retention rates, which, in turn, drive premiums. The company expects premiums in excess and surplus lines to reach $200 million for 2023. It estimates Small Commercial to report written premiums exceeding $5 billion in 2023.

Improved fully insured ongoing premiums driven by robust sales and solid persistency contribute to the impressive performance of HIG’s Group Benefits business. The insurer makes efforts to bolster its suite of group benefits offerings, and its move to introduce a critical illness insurance product covering more than 160 health conditions this year bears testament to the same.

Improved premiums flowing from Commercial Lines and Group Benefits businesses bode well for the top line of Hartford Financial since premiums account for a significant chunk of any insurer’s revenues.

The company also earns through investment income by having a diversified investment portfolio in place. In 2023, it expects full yield, excluding limited partnerships, to be 80 bps higher than in 2022.

Though catastrophe losses come with their share of worries, frequent losses ramp up the policy renewal rate and sustain the steady flow of premiums to HIG. Hartford Financial also has reinsurance agreements in place, which limit the losses suffered.

HIG has been resorting to product launches or acquisitions to upgrade capabilities and strengthen its nationwide presence. It has undertaken divestitures to intensify its focus on its U.S. operations and release capital, which, in turn, offer increased financial flexibility to pursue business investments. Cost-cutting measures are an indication of Hartford Financial’s efforts to provide respite to margins in the days ahead.

A strong financial position equips Hartford Financial to engage in the tactical deployment of capital through share buybacks or dividend payments. The insurer had a leftover capacity of $1.7 billion under its share repurchase program as of Sep 30, 2023.

Other Stocks to Consider

Some other top-ranked stocks from the Insurance space are Everest Group, Ltd. EG, Assurant, Inc. AIZ and AXIS Capital Holdings Limited AXS. While Everest Group presently sports a Zacks Rank #1 (Strong Buy), Assurant and Axis Capital carry a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Everest Group has a solid track record of beating earnings estimates in three of the last four quarters, missing once, the average being 24.5%.

The Zacks Consensus Estimate for EG’s 2023 and 2024 EPS is pegged at $55.6 and $62.6, indicating a year-over-year increase of 105.3% and 12.6%, respectively.

Assurant has a solid track record of beating earnings estimates in each of the last four quarters, the average being 42.4%.

The Zacks Consensus Estimate for AIZ’s 2023 and 2024 EPS is pegged at $14.59 and $15.21, indicating a year-over-year increase of 31.1% and 4.3%, respectively.

Axis Capital has a solid track record of beating earnings estimates in each of the last four quarters, the average being 22.5%.

The Zacks Consensus Estimate for AXS’s 2023 and 2024 EPS is pegged at $8.56 and $9.55, indicating a year-over-year increase of 47.3% and 11.6%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Hartford Financial Services Group, Inc. (HIG) : Free Stock Analysis Report

Assurant, Inc. (AIZ) : Free Stock Analysis Report

Axis Capital Holdings Limited (AXS) : Free Stock Analysis Report

Everest Group, Ltd. (EG) : Free Stock Analysis Report