Here's Why You Should Invest in Penumbra (PEN) Stock for Now

Penumbra, Inc.'s PEN consistent revenue growth momentum is driven by the extraordinary patient outcomes with Lightning Flash, Lightning Bolt 7 and RED 72 with SENDit technology. The company’s vascular and neuro businesses are showing encouraging growth trends. Penumbra’s Immersive Healthcare business too is making significant progress.

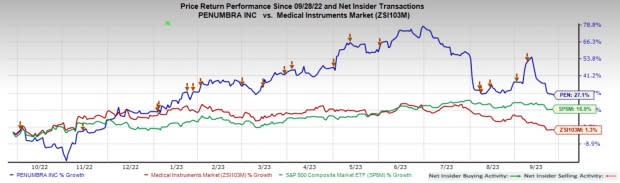

In the past year, the Zacks Rank #1(Strong Buy) stock has gained 27.1% against the industry’s 1.3% rise and the S&P 500’s 16.9% rise.

The global healthcare provider company has a market capitalization of $9.44 billion. It surpassed estimates in the trailing four quarters, the average surprise being 94.2%.

Key Growth Catalysts

Strong Portfolio Expansion: Penumbra is still in the early stages of its journey to bring the company’s proprietary thrombectomy technologies to patients in the United States and internationally. The company’s consistent revenue growth momentum is being driven by the extraordinary outcomes Penumbra is witnessing in patients treated with Lightning Flash, Lightning Bolt 7 and RED 72 with SENDit technology.

According to the company, Lightning Flash's transformative power, speed, safety and efficacy profile is the biggest driver of the exceptional early adoption of the product. In terms of Lightning Bolt 7, Penumbra is seeing an acceleration of Lightning Bolt 7 cases in the last two months of the second quarter as conversion from surgery, lytics and other mechanical thrombectomy products are gaining momentum. At the end of the second quarter, Penumbra has more than 1,000 active submissions in hospitals for either Lightning Flash or Lightning Bolt 7 approval.

Robust Vascular Business Growth: Penumbra is demonstrating strong growth within the company’s Vascular business, banking on the rapid increase in sales of the company’s vascular thrombectomy products in the United States. In this region, the company benefits from new product sales and further market penetration of existing products. Meanwhile, despite supply-related issues, the Lightning Flash launch in 2023 exceeded Penumbra’s expectations, becoming the biggest product launch in the company's history. Lightning Flash is also driving an acceleration in Penumbra’s U.S. vascular thrombectomy franchise, which grew nearly 24% year over year in the second quarter.

Stable Solvency Structure: Penumbra exited the second quarter of 2023 with cash and cash equivalents of $221 million compared with $199 million at the end of the first quarter of 2023. Meanwhile, total debt was $24 million, much lower than the corresponding cash and cash equivalent level. Also, it has no short-term payable debt on its balance sheet. This is good news regarding the company’s solvency position, particularly during the global inflationary situation and supply halt issues.

Image Source: Zacks Investment Research

At the end of the second quarter of 2023, total debt-to-capital was low at 2.2%. It also represented a drop from 2.3% in the first quarter. The industry’s debt-to-capital of 30.8% stands significantly higher than the company.

Raised Guidance: Penumbra issued updated guidance for 2023 revenues. The company expects net sales in the range of $1.05-$1.07 billion, suggesting a 24-26% improvement year over year. Previously, PEN anticipated sales to be in the band of $1.04-$1.06 billion in 2023. It expects the vascular business to grow slightly above the 24-26% range and the neuro business to remain below this guidance.

Estimate Trends

In the past 90 days, the Zacks Consensus Estimate for its fiscal 2023 earnings has moved up 10.9% to $1.73.

The Zacks Consensus Estimate for fiscal 2023 revenues is pegged at $1.06 billion, suggesting a 25% rise from the year-ago reported number.

Key Picks

Some other top-ranked stocks in the broader medical space are DaVita Inc. DVA, HealthEquity, Inc. HQY and Integer Holdings Corporation ITGR.

DaVita, sporting a Zacks Rank #1 (Strong Buy), has an estimated long-term growth rate of 12.7%. DVA’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average surprise of 21.4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita’s shares have increased 19.1% against the industry’s 0.4% decline in the past year.

HealthEquity, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 23.5%. HQY’s earnings surpassed estimates in all the trailing four quarters, with an average of 13%.

HealthEquity has increased 3.4% against the industry’s 4% decline in the past year.

Integer Holdings, carrying a Zacks Rank #2, has an estimated long-term growth rate of 12.1%. ITGR’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 8.4%.

Integer Holdings’ shares have gained 28.5% compared with the industry’s 4.2% rise in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report