Here's Why Investors Should Hold Encompass Health (EHC) Now

Encompass Health Corporation EHC has been gaining on growing patient admissions, solid demand for rehabilitation services, expanding facility count and a robust cash position. A solid 2023 business outlook also reinforces investors’ confidence in the stock.

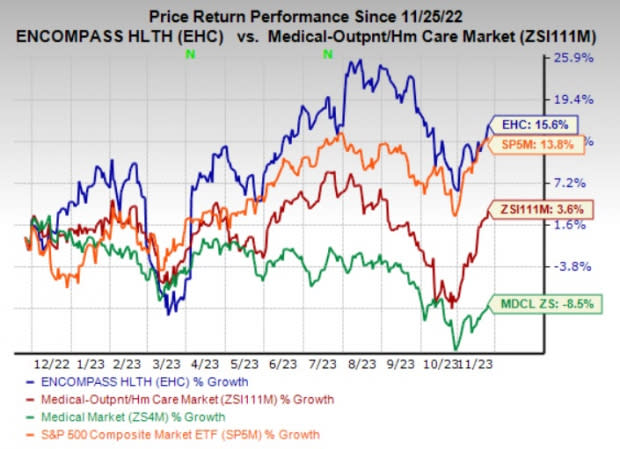

Zacks Rank & Price Performance

Encompass Health currently carries a Zacks Rank #3 (Hold).

The stock has gained 15.6% in the past year compared with the industry’s 3.6% growth. The Zacks Medical sector has declined 8.5% but the S&P 500 composite increased 13.8% in the same time frame.

Image Source: Zacks Investment Research

Favorable Style Score

EHC is well-poised for progress, as evidenced by its impressive VGM Score of B. Here V stands for Value, G for Growth and M for Momentum, and the score is a weighted combination of all three factors.

Robust Growth Prospects

The Zacks Consensus Estimate for Encompass Health’s 2023 earnings is pegged at $3.52 per share, indicating an improvement of 23.5% from the year-earlier reading. The consensus mark for 2024 earnings is pegged at $3.83 per share, suggesting 9% growth from the 2023 estimate.

The expected long-term earnings growth rate is pegged at 13.5%, better than the industry’s average of 11.5%.

Northbound Estimate Revision

The Zacks Consensus Estimate for 2023 earnings has been revised upward 2% in the past 30 days.

Impressive Earnings Surprise History

The bottom line of Encompass Health outpaced estimates in each of the trailing four quarters, the average surprise being 17.33%.

Solid Return on Equity

The return on equity for EHC is currently 18.3%, which is higher than the industry’s average of 7.6%. The figure substantiates the company’s efficiency in utilizing shareholders’ funds.

A Solid 2023 Outlook

EHC anticipates revenues to be within $4.77-$4.80 billion this year, the midpoint of which indicates 10% growth from the 2022 reported figure.

Adjusted earnings per share are estimated to lie between $3.41 and $3.52, the midpoint of which suggests 21.6% growth from the 2022 figure.

Business Tailwinds

Growing patient volumes continue to drive revenues for Encompass Health. The top line improved 10.7% year over year in the first nine months of 2023. An aging U.S. population, along with the need for effective rehabilitation services that empower individuals to resume daily activities, is likely to sustain the solid demand for EHC’s services in the days ahead.

Encompass Health’s expansion strategy remains quite commendable. It constructs inpatient rehabilitation hospitals across different U.S. communities to delve deep into regions grappling with inadequate access to rehabilitation services. EHC also adds beds to expand the operations of its existing facilities. Management expects to add 150-plus beds to its existing facilities next year.

Each hospital inauguration advances the capabilities and expands the nationwide foothold of Encompass Health. It also enters into joint ventures with regional healthcare organizations for constructing hospitals, which in turn, empower the company to gain an in-depth knowledge of the healthcare needs in its immediate surroundings. Riding on an active expansion route, the healthcare portfolio of EHC currently comprises 161 hospitals spread across 37 states and Puerto Rico.

The latest addition to its hospital count was the Wisconsin-based Rehabilitation Hospital of Fitchburg, which contains 56 beds.

To pursue such uninterrupted growth-related investments, a solid financial position is in dire need, which puts EHC at an advantage. Encompass Health boasts growing cash reserves and solid cash-generating abilities. As of Sep 30, 2023, cash and cash equivalents increased nearly five-fold from the 2022-end level. It also generated operating cash flows of $649.8 million in the first nine months of 2023.

Stocks to Consider

Some better-ranked stocks in the Medical space are Novo Nordisk A/S NVO, Centene Corporation CNC and Penumbra, Inc. PEN. While Novo Nordisk currently sports a Zacks Rank #1 (Strong Buy), Centene and Penumbra carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Novo Nordisk’s earnings surpassed estimates in two of the last four quarters, matched the mark once and missed the same on the remaining one occasion, the average surprise being 0.58%. The Zacks Consensus Estimate for NVO’s 2023 earnings indicates a surge of 51.5%, while the same for revenues suggests an improvement of 31.5% from the respective year-ago actuals. The consensus mark for NVO’s 2023 earnings has moved 1.9% north in the past 30 days.

The bottom line of Medpace beat estimates in each of the trailing four quarters, the average beat being 14.62%. The Zacks Consensus Estimate for MEDP’s 2023 earnings indicates a rise of 18.8%, while the same for revenues suggests an improvement of 29.4% from the respective prior-year tallies. The consensus mark for MEDP’s 2023 earnings has moved 1.6 % north in the past 30 days.

Penumbra’s earnings outpaced estimates in each of the trailing four quarters, the average surprise being 55.65%. The Zacks Consensus Estimate for PEN’s 2023 earnings is pegged at $2.04 per share, which indicates an increase of nearly 13-fold from the year-ago reported figure. The consensus mark for revenues suggests an improvement of 25.3% from the year-ago actual. The consensus mark for PEN’s 2023 earnings has moved 2.5% north in the past seven days.

Shares of Novo Nordisk, Medpace and Penumbra have gained 75.3%, 26.6% and 18%, respectively, in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Novo Nordisk A/S (NVO) : Free Stock Analysis Report

Centene Corporation (CNC) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report

Encompass Health Corporation (EHC) : Free Stock Analysis Report