Here's Why Investors Should Retain Abbott (ABT) Stock Now

Abbott Laboratories ABT is well-poised for growth in the coming quarters, courtesy of its strategic global expansion to address the unmet demand for advanced medical technologies. The company’s Diabetes Care business continued to benefit from the growing sales of its flagship, sensor-based continuous glucose monitoring system, FreeStyle Libre. However, forex woes and lower COVID sales impede growth.

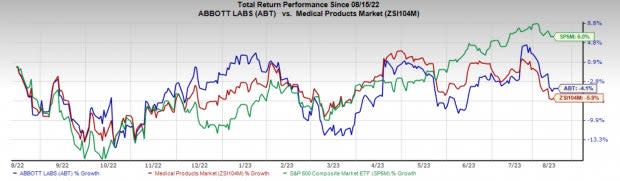

In the past year, this Zacks Rank #3 (Hold) stock has declined 4.1% compared with 5.9% decline of the industry and a 6% rise of the S&P 500 composite.

This renowned provider of a diversified line of healthcare products has a market capitalization of $183.12 billion. The company projects a 5.1% growth for the next five years and expects to maintain its strong performance. Abbott’s earnings surpassed estimates in all of the trailing four quarters, the average surprise being 12.44%.

Let’s delve deeper.

Factors at Play

Strong Prospects Within Core Diagnostics: Abbott is expanding its Diagnostics business foothold (consisting of nearly 30% of its total revenues in the second quarter of 2023). Although there has been a decline in demand for Abbott’s rapid diagnostic tests to detect COVID-19 over the past few quarters, it is largely offset by higher growth across other businesses. Abbott is experiencing increased demand for routine diagnostic testing in the United States and Europe. Further, in the United States, Abbott is registering strong growth within the blood transfusion testing business, which is consistently recovering from the impact of lower plasma donations during the COVID-19 pandemic.

Libre Drives Diabetes Care: Abbott’s Diabetes Care business continued to benefit from the growing sales of its flagship, sensor-based continuous glucose monitoring system, FreeStyle Libre. In a relatively short span, FreeStyle Libre has achieved global leadership among constant glucose monitoring (CGM) systems for Type 1 and Type 2 users. In 2023, as a major milestone for the company, Libre became the first and only CGM system to be nationally reimbursed in France. In 2023, Libre received FDA clearance for connectivity with automated insulin delivery systems. Abbott is working with leading insulin pump manufacturers to integrate their systems with Libre 2 and Libre 3.

Sales Recovery Within Nutrition: Following the massive setback due to the voluntary recall and production stoppage of certain infant powder formula products manufactured at its facility in Sturgis, MI, last year, Abbott’s Nutrition business started showing signs of recovery since the beginning of 2023. Per the last update on the second-quarter earnings call, the company has made good progress in increasing manufacturing production. It has now recovered approximately 75% of the market share in the infant formula business.

Downsides

Foreign Exchange Translation Impacts Sales: Foreign exchange is a significant headwind for Abbott due to a considerable percentage of its revenues coming from outside the United States. The strengthening of the euro and some other developed market currencies has constantly been hampering the company’s performance in the international markets.

In the second quarter, foreign exchange had an unfavorable year-over-year impact of 2.5% on sales.

Image Source: Zacks Investment Research

Declining COVID Testing Dents Growth: Through the last few months of 2022 and following the official ending of the public health emergency in May, Abbott is experiencing a continuous decline in COVID testing-related demand. Through the first six months of 2023, Abbott’s Rapid Diagnostics sales decreased 67.9% from the year-ago period due to lower demand for COVID-19 tests.

Estimate Trends

In the past 90 days, the Zacks Consensus Estimate for earnings has moved 0.5% north to $4.40.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $39.77 billion, suggesting an 8.9% decline from the year-ago quarter’s reported number.

Key Picks

Some other top-ranked stocks in the broader medical space are Penumbra, Inc. PEN, Integer Holdings Corporation ITGR and Patterson Companies, Inc. PDCO.

Penumbra, carrying a Zacks Rank of 1 (Strong Buy), reported second-quarter 2023 adjusted EPS of 43 cents, beating the Zacks Consensus Estimate by 53.6%. Revenues of $261.5 million outpaced the consensus mark by 3.3%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Penumbra has an estimated 2024 growth rate of 57.9%. PEN’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 94.2%.

Patterson Companies has an Earnings ESP of +5.66% and a Zacks Rank of 1. PDCO has an estimated long-term growth rate of 9.2%.

Patterson Companies’ earnings surpassed estimates in three of the trailing four quarters and missed once, with the average surprise being 4.5%.

Integer Holdings reported a second-quarter 2023 adjusted EPS of $1.14, beating the Zacks Consensus Estimate by 15.2%. Revenues of $400 million surpassed the Zacks Consensus Estimate by 8.9%. It currently carries a Zacks Rank #2.

Integer Holdings has a long-term estimated growth rate of 12.1%. ITGR’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 8.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abbott Laboratories (ABT) : Free Stock Analysis Report

Patterson Companies, Inc. (PDCO) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report