Here's Why Investors Should Retain Phibro (PAHC) for Now

Phibro Animal Health Corporation PAHC is well-poised for growth in the coming quarters, backed by its diverse product offerings. Year to date, product lines across the vaccine business were up 9% in the fiscal third quarter, with notable growth in the Latin America region. Progress in the development pipeline of Companion Animal is encouraging. The expansion of Phibro’s business in key growth regions also buoys optimism.

However, operating in a tough competitive space amid continued macroeconomic headwinds is concerning.

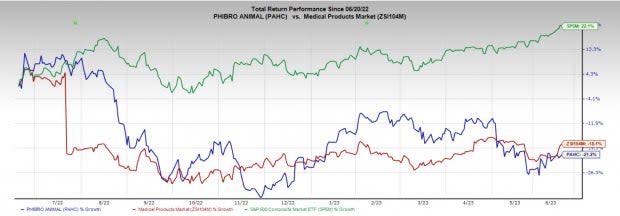

In the past year, this Zacks Rank #3 (Hold) stock has decreased 21.2% compared with the 18.1% fall of the industry and a 22.1% rise of the S&P 500 composite.

The renowned animal health and mineral nutrition company has a market capitalization of $559.8 million. PAHC carries an earnings yield of 8.97%, against the industry’s yield of -2.31%. Phibro delivered an average negative earnings surprise of 7.01% in the trailing four quarters.

Let’s delve deeper.

Factors at Play

A Diversified Product Portfolio: Phibro’s key animal health products, which comprise MFAs (Medicated Feed Additives) and nutritional specialty products, facilitate enhancing animal nutrition. In the fiscal third quarter, the company witnessed the increased demand for MFAs in the United States and Latin America and Canada, along with the growing demand for processing aids used in the ethanol fermentation industry.

In the last reported quarter, growth in nutritional specialties was led by higher domestic demand and higher selling prices for dairy products, along with growth in the companion animal product, Rejensa. The vaccine product business growth was driven by new registrations.

Image Source: Zacks Investment Research

A Prospering Vaccine Business: PAHC is focusing on new developments along with incremental registrations and the growing volumes of vaccine technologies. The company makes significant investments to expand vaccine manufacturing capacity at several locations.

In the third quarter of fiscal 2023, Phibro registered a 15% improvement in vaccine net sales, driven by increased demand and new product launches in Latin America.

Potential in Emerging Markets: Phibro’s existing operations and distribution network in more than 75 countries pave the path for global growth opportunities. Outside the United States, Phibro’s global footprint extends to countries where the livestock production growth rate is expected to be higher than the average growth rate. This includes Brazil and other countries in South America, China, India and Asia Pacific, Russia and former CIS countries, Mexico, Turkey, Australia, Canada, South Africa and other countries in Africa.

Downsides

Macroeconomic Headwinds Mar Growth in Q3: Macroeconomic and operational challenges continue to dent Phibro’s profitability. In the fiscal third quarter, supply-chain disruptions were less common but still occurred. Meanwhile, PAHC posted a year-over-year decline in earnings. Higher SG&A expenses negatively weighed on the company’s operating margin in the quarter under review.

A Tough Competitive Landscape: Phibro’s competitive position is based principally on its product registrations, customer service and support, breadth of the product line, product quality, manufacturing technology, facility location, and product prices. A few of the company’s principal competitors include Bayer AG, Boehringer Ingelheim International GMBH, Eli Lilly and Company (Elanco Animal Health), Merck & Co., Inc. (Merck Animal Health and MSD Animal Health) and Zoetis Inc.

Moreover, consolidation continues to rise in the animal health market. This might work in favor of Phibro’s competitors.

Estimate Trend

The Zacks Consensus Estimate for Phibro’s 2023 earnings per share (EPS) has remained constant at $1.24 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $982.4 million. This suggests a 4.25% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Zimmer Biomet ZBH, Penumbra PEN and Hologic, Inc. HOLX.

Zimmer Biomet has an earnings yield of 5.17% compared to the industry’s -2.31%. Zimmer Biomet’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 7.38%. Its shares have increased 41.5% against the industry’s 18.1% decline in the past year.

ZBH sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Penumbra, sporting a Zacks Rank #1 at present, has an estimated growth rate of 64.1% for 2024. Penumbra shares have risen 180.8% compared with the industry’s 20.4% increase over the past year.

PEN’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 109.4%.

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an earnings yield of 4.79% compared to the industry’s -7.19%. Shares of HOLX have risen 19.6% compared with the industry’s 20.3% growth over the past year.

Hologic’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 27.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC) : Free Stock Analysis Report

Zimmer Biomet Holdings, Inc. (ZBH) : Free Stock Analysis Report

Penumbra, Inc. (PEN) : Free Stock Analysis Report