Here's Why Maximus (MMS) is an Attractive Pick Right Now

MaximusMMS has had a decent run on the bourses over the past year, gaining 10% compared with its industry’s 30.2% growth and the S&P 500 composite’s 22.5% rise.

Let us delve deeper into the reasons that make MMS an attractive pick.

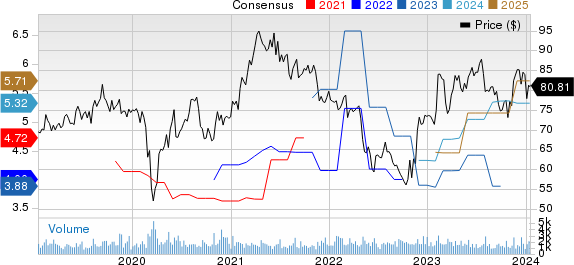

Upbeat Earnings Expectations: Earnings growth and stock price gains often indicate a company’s solid prospects. For the fourth quarter of 2023, the Zacks Consensus Estimate for earnings is pegged at $1.28 per share, suggesting a 36.2% rise from the year-ago reported figure. For 2023, the consensus mark is pinned at $5.32, indicating a 38.9% increase from the year-ago reported figure. Both have been revised slightly northward in the past 60 days.

Maximus, Inc. Price and Consensus

Maximus, Inc. price-consensus-chart | Maximus, Inc. Quote

Solid Zacks Rank and Style Score: MMS currently has a Zacks Rank #2 (Buy) and a VGM Score of A. Our research shows that stocks with a Zacks Rank #1 (Strong Buy) or 2, when combined with a VGM Score of A or B, offer the best investment opportunities. Thus, the company appears to be a compelling investment proposition at the moment.

Bullish Industry Rank: The industry to which Maximus belongs currently has a Zacks Industry Rank of 37 (of 251 groups). Such a solid rank places the industry in the top 15% of the Zacks industries. Studies show that 50% of a stock price movement is directly tied to the performance of the industry group that it hails from.

A mediocre stock in a healthy group is likely to outperform a robust stock in a poor industry. Therefore, taking the industry’s performance into account becomes necessary.

Growth Factors: Maximus relies on the specialized knowledge of its workforce in key areas, such as the design, implementation, and operation of government health and human services programs. The company maintains robust cash flow from operations, attributed to its profitable business model and effective management of receivables.

In situations requiring immediate working capital, Maximus has the option to secure $600 million through a credit agreement with JPMorgan Chase N.A. Maximus’ proficiency in managing government programs and its capability to achieve well-defined, measurable outcomes set it apart. These factors collectively grant Maximus a competitive edge over its industry peers.

MMShas actively pursued acquisitions to expand its business processes, knowledge and client relationships, while enhancing technical capabilities and acquiring additional skill sets. The 2022 acquisition of Stirling Institute in Australia bolstered its employment services, and the acquisition of BZ Bodies strengthened Maximus's services in the U.K., both contributing to the company's growth outside the U.S. segment.

In the United States, MMS' revenues are projected to reach $4.13 billion, indicating 6.9% year-over-year growth. Additionally, revenues from Australia are expected to be $200.7 million, suggesting a 16.7% increase from the 2022 reported figure. This strategic approach aligns with Maximus's long-term organic growth strategy.

The companyhas consistently demonstrated a strong history of distributing dividends. In fiscal 2022, 2021 and 2020, the company paid out cash dividends of $68.7 million, $68.8 million and $70.2 million, respectively. These actions signify Maximus's dedication to delivering value to shareholders and emphasize the company's confidence in its business.

Other Stocks to Consider

Here are some other top-ranked stocks from the broader Business Services sector that you can consider for your portfolio.

Broadridge Financial Solutions BR:The Zacks Consensus Estimate of the company’s 2023 revenues indicates 7.7% growth from the year-ago reported figure, whereas the same for earnings suggests a 10.1% rise. BR has beaten the consensus estimate in three of the past four quarters and matched once, the average surprise being 5.4%.

The company currently carries a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Booz AllenBAH:The Zacks Consensus Estimate of BAH’s 2023 revenues indicates 13% growth from the year-ago reported figure, whereas the same for earnings suggests a rise of 10.3%. The company has beaten the consensus estimate in three of the four quarters and missed once, the average surprise being 7.7%.

BAH carries a Zacks Rank of 2 at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Broadridge Financial Solutions, Inc. (BR) : Free Stock Analysis Report

Booz Allen Hamilton Holding Corporation (BAH) : Free Stock Analysis Report

Maximus, Inc. (MMS) : Free Stock Analysis Report