Here's Why You Should Retain Celanese (CE) in Your Portfolio

Celanese Corporation CE is benefiting from its cost and productivity actions, investments in high-return organic projects and synergies of acquisitions amid headwinds from demand softness.

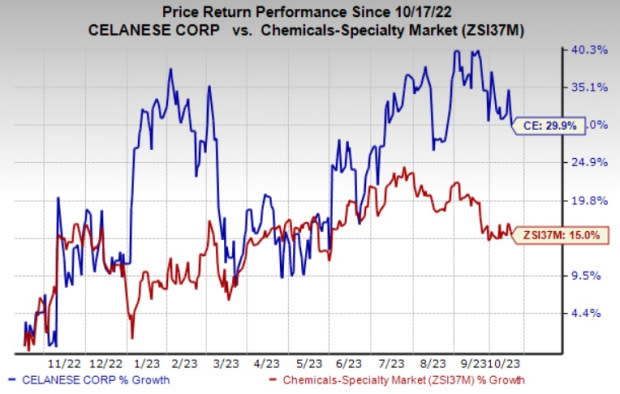

Shares of this leading chemical and specialty materials maker are up 29.9% over a year compared with a 15% rise of its industry.

Let’s find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Image Source: Zacks Investment Research

Acquisitions, Productivity to Aid Results

Celanese remains focused on executing its productivity programs that include the implementation of a number of cost reduction capital projects. Productivity actions are expected to support to its margins in 2023.

The company is proactively implementing strategic initiatives recognizing the volatility and unpredictability of the current market landscape and competitive environment. These actions involve strengthening its commercial teams, aligning production and inventory levels with prevailing demand, implementing cost-saving measures, and optimizing cash flow. These endeavors are expected to result in robust cash generation and a continuation of earnings growth during the second half of 2023. The company's incremental cost actions are expected to deliver $60-$80 million in savings in the second half.

Moreover, the company is actively pursuing acquisitions, which are providing it opportunities for additional growth, investment and synergies. The acquisition of the majority of DuPont’s Mobility & Materials (“M&M”) business has allowed Celanese to enhance its growth in high-value applications. M&M contributed $109 million to the company’s operating EBITDA in second-quarter 2023. Celanese sees a $25-$35 million sequential increase in operating EBITDA contribution in the third quarter.

The acquisitions of SO.F.TER., Nilit and Omni Plastics are also expected to contribute to earnings expansion in the company's Engineered Materials segment. The Elotex acquisition also strengthened the company’s position in the vinyl acetate ethylene emulsions space. Moreover, the purchase of Exxon Mobil's Santoprene business broadened the company’s portfolio of engineered solutions and enables it to offer a wider range of functionalized solutions to targeted growth areas, including future mobility, medical and sustainability.

Weak Demand Ails

Celanese faces headwinds from demand softness and customer destocking in certain end markets. It witnessed weak demand in several end markets and continued customer destocking in the second quarter of 2023. Soft demand has led to inventory reduction and deferral of orders by the company’s customers. Celanese is seeing weaker demand in industrial and electrical & electronics end markets. Weaker demand recovery globally and destocking are likely to continue to weigh on the company’s volumes and pricing in the third quarter.

Celanese Corporation Price and Consensus

Celanese Corporation price-consensus-chart | Celanese Corporation Quote

Stocks to Consider

Better-ranked stocks worth a look in the basic materials space include Koppers Holdings Inc. KOP, Carpenter Technology Corporation CRS and The Andersons Inc. ANDE.

Koppers has a projected earnings growth rate of 7.5% for the current year. It currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Koppers has a trailing four-quarter earnings surprise of roughly 21.7%, on average. KOP shares have surged around 65% in a year.

The Zacks Consensus Estimate for current fiscal-year earnings for CRS is currently pegged at $3.48, implying year-over-year growth of 205.3%. Carpenter Technology currently carries a Zacks Rank #2.

Carpenter Technology has a trailing four-quarter earnings surprise of roughly 10%, on average. The stock has rallied around 86% over the past year.

Andersons currently carries a Zacks Rank #2. The Zacks Consensus Estimate for ANDE's current-year earnings has been revised 3.3% upward over the past 60 days.

Andersons beat the Zacks Consensus Estimate in each of the last four quarters. It delivered a trailing four-quarter earnings surprise of 64.4%, on average. ANDE shares have rallied around 49% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Andersons, Inc. (ANDE) : Free Stock Analysis Report

Carpenter Technology Corporation (CRS) : Free Stock Analysis Report

Celanese Corporation (CE) : Free Stock Analysis Report

Koppers Holdings Inc. (KOP) : Free Stock Analysis Report