Here's Why You Should Retain CVS Health (CVS) Stock for Now

CVS Health Corporation CVS is well-poised for growth, backed by the entire range of insured and self-insured medical, pharmacy, dental and behavioral health products and services that instill optimism. The acquisition of Oak Street Health advances its care delivery strategy for consumers, which is likely to boost future growth.

However, stiff competition and poor macroeconomic conditions are a concern.

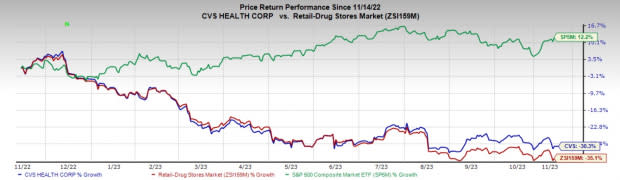

In the past year, this Zacks Rank #3 (Hold) stock has declined 30.3% compared with the industry’s 35.1% fall and the S&P 500’s 12.2% rise.

The pharmacy innovation company, with integrated offerings across the entire spectrum of pharmacy care, has a market capitalization of $87.09 billion. The company has a long-term estimated earnings growth rate of 4.5%.

Let’s delve deeper.

Tailwinds

Health Care Benefit Shows Potential: Following the colossal acquisition of health insurance giant Aetna, CVS Health has introduced its Health Care Benefits business arm.

Medical membership in the third quarter of 2023 grew to 25.7 million, an increase of 1.4 million members versus the prior year, reflecting growth across multiple product lines, including individual exchange, Medicare, and commercial. CVS Health demonstrated strong growth led by significant progress made in restoring its Medicare Advantage Star ratings. Medicare Advantage is a key strategic growth area for its business.

During the third quarter earnings update, the company stated that Aetna continues to be a leader in zero-dollar premium products and approximately 84% of Medicare eligibles will have access to Aetna plans in this category in 2024.

Health Services Business Gaining Traction: CVS Health continues to gain traction within Health Services (previously known as the Pharmacy segment) driven by pharmacy claims growth, specialty pharmacy and brand inflation.

Within Health Service, both Signify Health and Oak Street Health continue to deliver strong business performance consistent with expectations.

Image Source: Zacks Investment Research

As Oak Street expands to additional geographies, these opportunities to drive higher patient growth will continue to increase. By the end of 2023, CVS Health expects to have Oak Street clinics in 25 states, up from 21 at the close of the transaction. The company expects to build 50-60 clinics next year.

Strong Solvency and High Return to Investors: CVS Health ended third-quarter 2023 with cash and cash equivalents of $16.19 billion compared with $16.88 billion at the end of second-quarter 2023. Long-term debt came up to $59.78 billion compared with $61.41 billion at the end of second-quarter 2023.

Although the total year-end debt was much higher than the corresponding cash and cash equivalent level, the near-term payable debt is at $2.1 million, lower than the short-term cash level. This is positive news in terms of solvency level as, at least during the economic downturn, the company is holding sufficient cash for debt repayment.

Downsides

Competitive Landscape: In spite of significant new client wins in the course of a strong selling season, intense competition and harsh industry conditions are major impediments for CVS Health. Big competitors such as Walgreens, Target and Wal-Mart are expanding their pharmacy businesses.

Exposure to International Market Risks: CVS Health’s international operations present political, legal, compliance, operational, regulatory, economic and other risks. These risks vary widely by country and include several regional and geopolitical business conditions and demands, government intervention and censorship, discriminatory regulation, climate change regulation, nationalization or expropriation of assets and pricing constraints.

Estimate Trends

In the past 90 days, the Zacks Consensus Estimate for its fiscal 2023 earnings has moved down from $8.62 to $8.59 per share.

The Zacks Consensus Estimate for fiscal 2023 revenues is pegged at $352.9 billion, suggesting a 9.5% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space that have announced quarterly results are Abbott Laboratories ABT, DexCom, Inc. DXCM and Integer Holdings Corporation ITGR.

Abbott, carrying a Zacks Rank of 2 (Buy), posted adjusted earnings per share (EPS) of $1.14 in third-quarter 2023, beating the Zacks Consensus Estimate by 3.6%. Revenues of $10.14 billion outpaced the consensus mark by 3.6%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Abbott has a long-term estimated growth rate of 5.1%. ABT’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 6.8%.

DexCom reported third-quarter 2023 adjusted EPS of 50 cents, beating the Zacks Consensus Estimate by 47.1%. Revenues of $975 million surpassed the Zacks Consensus Estimate by 4%. It currently carries a Zacks Rank #2.

DexCom has a long-term estimated growth rate of 33.6%. DXCM’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 36.4%.

Integer Holdings reported adjusted EPS of $1.27 in third-quarter 2023, beating the Zacks Consensus Estimate by 20.9%. Revenues of $404.7 million surpassed the Zacks Consensus Estimate by 8.7%. It currently carries a Zacks Rank #2.

Integer Holdings has a long-term estimated growth rate of 15.8%. ITGR’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 11.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abbott Laboratories (ABT) : Free Stock Analysis Report

CVS Health Corporation (CVS) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report