Here's Why You Should Retain Globus Medical (GMED) Stock Now

Globus Medical, Inc. GMED is well-poised for growth in the coming quarters, backed by growth across its U.S. spine and trauma portfolios. The Enabling Technologies business benefits from the continued uptake of EGPS and E3D systems. However, several macroeconomic issues are denting the company’s profit margins.

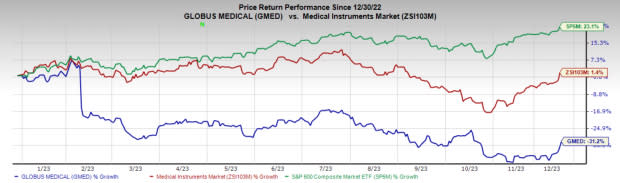

In the past year, this Zacks Rank #3 (Hold) stock has increased 31.2% compared with the 1.4% rise of the industry and a 23.1% increase of the S&P 500 composite.

The renowned medical device company has a market capitalization of $6.81 billion. Globus Medical projects a long-term estimated earnings growth rate of 11.5% compared with 13.3% of the industry. GMED’s earnings surpassed estimates in three of the trailing four quarters and missed the same in one, delivering an average surprise of 5.44%.

Let’s delve deeper.

Upsides

Musculoskeletal Prospects Strong: In the third quarter, Legacy Globus's musculoskeletal revenues rose 10.7%. Earlier, Globus Medical launched three new products — REFLECT, MARVEL and Ossifuse. The company continues to make significant progress in launching its prone, lateral patient positioning system. As Globus Medical moves into the second half of 2023 and into 2024, the company anticipates a strong cadence of product launches throughout the Musculoskeletal portfolio.

Steady Pace of Product Development: In line with the company’s business strategy to focus on its integrated product development, Globus Medical is consistently making efforts in research and development.

In September 2023, Globus Medical launched the Precice Bone Transport system commercially in the targeted areas by NuVasive Specialised Orthopaedics (NSO). The most recent addition to the less intrusive NSO portfolio recently received CE marking and approval, and it is now offered in a few regions.

Image Source: Zacks Investment Research

In Q3, the company launched Hydrone, an interior 3D printed interbody fusion device and Strato wiring system for trauma. Management noted that Surgeons would soon start gaining access to its broader expandable offerings, 3D printed interbody portfolio, cervical disc, robotic prone, lateral system, EGPS E3D and neuromonitoring solutions, improved retractors, Magic and the precise family of limb-lengthening products.

Strong Liquidity, Solvency and Capital Structure: Globus Medical exited the third quarter of 2023 with cash and cash equivalents and short-term marketable securities of $468.9 million compared with $612.8 million at the end of the second quarter. The company finished the quarter with no debt on its balance sheet.

Downsides

Macroeconomic Concerns Curb Profit: Like other industry players, Globus Medical is currently grappling with negative trends in the global economy, including interest rate fluctuations, increases in inflation, and financial market volatility. These factors are affecting the company’s operations and financial performance. Global inflation, in particular, led to a significant rise in the cost of raw materials for companies. In the third quarter, the company incurred a 139.6% surge in the cost of goods sold.

Exposure to Currency Movement: In the last nine months, Globus Medical generated 17.1% of its sales from the international market. A significant portion of the company’s foreign revenues and expenses is generated in Japan, the Eurozone, the U.K. and Australia. This makes it highly vulnerable to currency fluctuations. For 2022, the company reported a foreign currency transaction loss of $1.02 million.

Estimate Trend

The Zacks Consensus Estimate for 2023 earnings per share (EPS) moved from $2.32 to $2.30 in the past 90 days.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $1.56 billion. This suggests a 52.1% rise from the year-ago reported number.

Key Picks

Some beter-ranked stocks in the broader medical space are Haemonetics HAE, Insulet PODD and DexCom DXCM. While Haemonetics and DexCom each carry a Zacks Rank #2 (Buy), Insulet sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Haemonetics’ shares have increased 11.6% in the past year. Earnings estimates for Haemonetics have increased from $3.82 to $3.86 in 2023 and $4.07 to $4.11 in 2024 in the past 30 days.

HAE’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 16.1%. In the last reported quarter, it posted an earnings surprise of 5.3%.

Estimates for Insulet’s 2023 earnings per share have increased from $1.61 to $1.90 in the past 30 days. Shares of the company have plunged 40.9% in the past year compared with the industry’s decline of 7%.

PODD’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 105.1%. In the last reported quarter, it delivered an average earnings surprise of 77.4%.

Estimates for DexCom’s 2023 earnings per share have increased from $1.23 to $1.41 in the past 30 days. Shares of the company have fallen 7.8% in the past year compared with the industry’s decline of 7.1%.

DXCM’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 36.4%. In the last reported quarter, it delivered an average earnings surprise of 47.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report

Globus Medical, Inc. (GMED) : Free Stock Analysis Report