Here's Why You Should Retain Illumina (ILMN) Stock for Now

Illumina, Inc. ILMN is well poised for growth in the coming quarters, owing to solid long-term growth potential in the oncology space. The company ended the first quarter of 2023 with better-than-expected results. GRAIL continues to have strong demand from consumers, physicians, health systems and payers. However, expensive valuation and stiff competition raise apprehension.

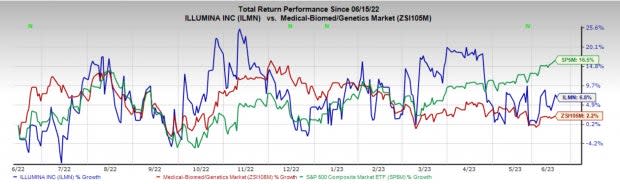

In the past year, the Zacks Rank #3 (Hold) stock has gained 6.8% compared with the 2.2% rise of the industry and the 16.5% rise of the S&P 500.

The renowned life sciences company, which provides tools and integrated systems for the analysis of genetic variation and function, has a market capitalization of $32.70 billion. Its first-quarter 2023 earnings per share surpassed the Zacks Consensus Estimate by 300%.

The company’s long-term expected growth rate of 22.2% exceeds the industry’s long-term growth expectation of 18.8%.

Let’s delve deeper

Factors at play

Q1 Upsides: Illumina delivered better-than-expected earnings and revenues in first-quarter 2023. Consolidated revenues were up 1% from fourth-quarter 2022 levels, exceeding the high end of the company’s guidance. Building on strong global interests, the company executed robust shipments of NovaSeq X instruments, exceeding its first-quarter guidance of 40-50 shipments. Core Illumina sequencing consumables revenues were up 1% sequentially. Total sequencing activity on the company’s connected high- and mid-throughput instruments rose 6% sequentially and 3% year over year. Research & Applied increased 7% sequentially. Clinical sequencing activity growth remained robust, up 7% from fourth-quarter 2022 levels and 15% year over year.

GRAIL continues to have strong demand from consumers, physicians, health systems and payers. GRAIL generated revenues of $20 million in the first quarter, up 100% year over year. The upside was primarily driven by the accelerated adoption of Galleri.

Solid Long-Term Growth Potential in Oncology Space: In the oncology business — another area of focus in its market expansion — the company developed multiple pharma partnerships to bring custom panel tests to market.

Image Source: Zacks Investment Research

In the first quarter, more than 80% of NovaSeq 6000 shipments were made to clinical customers and approximately 25% of shipments to oncology testing. Oncology testing increased 21% sequentially, driven by growing clinical testing volumes and increased product development in areas like liquid biopsy and MRD. Revenues from Illumina’s market-leading TruSight Oncology assay, TSO 500, were up 26% year over year across more than 540 accounts, driven by the increased utilization and pull-through, particularly in Europe. The company also talked about its expansion of partnership with Myriad Genetics to broaden access to homologous recombination deficiency (HRD) testing.

Upbeat Guidance: Illumina expects fiscal 2023 consolidated revenue growth in the range of 7-10% year over year (in line with the prior guidance). The adjusted earnings per share for 2023 is expected in the range of $1.25-$1.50 (unchanged).

Core Illumina revenue growth is expected in the range of 6-9% year over year. GRAIL revenues are anticipated between $90 million and $110 million. For the second quarter of 2023, Illumina anticipates consolidated revenues between $1.15 and $1.17 billion and an adjusted earnings per share of 1 cent.

Downsides

Expensive Valuation: Illumina’s P/S (F12M) ratio is expensive compared with the broader industry. The company is currently trading at a forward P/S (F12M) ratio of 6.3 for one year, whereas the current P/S (F12M) for the industry it belongs to is 1.9.

Tough Competition: Illumina faces significant competition in the sequencing, SNP genotyping, gene expression and molecular diagnostics markets with several large players already enjoying significant market share, intellectual property portfolios and regulatory expertise. Such companies include the likes of Agilent Technologies, Pacific Biosciences of California, BGI, QIAGEN N.V., Roche Holding A.G. and Thermo Fisher Scientific, among others.

Estimate Trends

In the past 30 days, the Zacks Consensus Estimate for Illumina’s 2023 earnings has been constant at $1.40.

The Zacks Consensus Estimate for 2023 revenues is pegged at $4.94 billion, suggesting a 7.71% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Hologic, Inc. HOLX, Merit Medical Systems, Inc. MMSI and Boston Scientific Corporation (BSX).

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an estimated growth rate of 5.1% for fiscal 2024. HOLX’s earnings surpassed estimates in all the trailing four quarters, the average being 27.3%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hologic has gained 15.5% compared with the industry’s 12.4% rise in the past year.

Merit Medical, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 20.2%.

Merit Medical has gained 54.1% compared with the industry’s 18.7% rise over the past year.

Boston Scientific, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11.5%. BSX’s earnings surpassed estimates in two of the trailing four quarters and missed in the other two, the average surprise being 1.9%.

Boston Scientific has gained 42% against the industry’s 23.6% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

Illumina, Inc. (ILMN) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report