Here's Why You Should Retain Medtronic (MDT) Stock for Now

Medtronic plc MDT is well poised for growth in coming quarters, backed by its expansion into the global market to address the unmet demand for advanced medical technologies. Within Cardiovascular, Medtronic is gaining market share, banking on product launches. However, forex woes and stiff rivalry do not bode well for MDT.

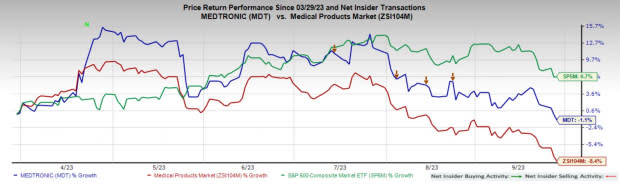

In the past six months, this Zacks Rank #3 (Hold) stock has decline 1.1% compared with the industry’s 8.4% fall and a 6.7% rise of the S&P 500 composite.

The renowned medical device company has a market capitalization of $104.07 billion. The company’s earnings surpassed estimates in all the trailing four quarters, delivering an average surprise of 3.37%.

Let’s delve deeper.

Tailwinds

Market Share Gain Within Cardiovascular to Continue: Medtronic is expanding its global foothold within the Cardiovascular business (contributing more than 37% to total revenues in fiscal 2023). Within Cardiovascular, cardiac rhythm management, one of Medtronic’s largest businesses, continued to build on the company’s category leadership. Medtronic’s pacing business continued outperforming the market within cardiac rhythm management, banking on strong global growth of its Micra leadless pacemaker family as it enters new geographies and expands penetration in existing markets.

Decent Sales Projections Within MedSurg: Within Medtronic’s Medical Surgical Portfolios, the company is gaining from the positive sales momentum with the rollout of its differentiated Hugo robotic system in many international markets. The company is also progressing well to bring Hugo to the United States. We are also impressed by Medtronic’s strong performance within Advanced Energy and Barrx, primarily driven by improved supply and continued growth in GI Genius and PillCam. Given less than 5% of surgical procedures globally are done robotically, Medtronic expects its surgical robotics business to become a meaningful growth driver soon.

Image Source: Zacks Investment Research

International Expansion Robust: in fiscal 2023, Medtronic generated nearly 48% of its revenues from the rest of the world. The company focuses on expanding in emerging markets to address the massively unmet and untapped demand for advanced medical technologies. In the fiscal first quarter, non-U.S. developed markets and Western Europe grew in the high single digits. Western Europe grew 8% again this quarter, with high-single-digit growth in Cardiovascular and Medical Surgical and high teen growth in Diabetes. Emerging markets grew 8% despite the adverse impact of new sanctions in Russia and the ongoing volume-based procurement (VBP) effect in China.

Downsides

Exposure to Currency Movement: With Medtronic recording a significant portion of its sales from the international market, it remains highly exposed to currency fluctuations. Unfavorable currency movements have been a significant dampener over the last few quarters, as with other important MedTech players. Medtronic expects its second-quarter fiscal 2024 adjusted earnings would be negatively impacted by approximately 6% from adverse currency translation.

Competitive Landscape: The presence of many players has made the medical devices market highly competitive. Medtronic earns most revenues from CRDM, Spinal and Cardio Vascular segments. The company faces intense competition in the CRDM segment from players such as Boston Scientific Corporation. Players such as Johnson & Johnson, Stryker Corporation, Zimmer and NuVasive have intensified competition, particularly in the Spinal segment.

Estimate Trends

Medtronic has been witnessing a negative estimate revision trend for fiscal 2024. The Zacks Consensus Estimate for 2024 earnings per share (EPS) has moved from $5.12 to $5.04 in the past 90 days.

The consensus estimate for the company’s fiscal 2024 revenues is pegged at $32.13 billion. This suggests a 4.4% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, HealthEquity, Inc. HQY and Integer Holdings Corporation ITGR.

DaVita, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 12.7%. DVA’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average surprise of 21.4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita has gained 19.1% against the industry’s 0.4% decline in the past year.

HealthEquity, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 23.5%. HQY’s earnings surpassed estimates in all the trailing four quarters, with an average of 13%.

HealthEquity has gained 3.4% against the industry’s 4% decline in the past year.

Integer Holdings, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 12.1%. ITGR’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 8.4%.

Integer Holdings has gained 28.5% compared with the industry’s 4.2% rise in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Medtronic PLC (MDT) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report