Here's Why You Should Retain Omnicell (OMCL) Stock Now

Omnicell OMCL is well-poised for growth in the coming quarters, backed by its ongoing efforts to automate and modernize the global medication management infrastructure. The company is building on its expense containment initiatives to bring the cost structure in line with near-term revenue expectations. Stable solvency is highly encouraging.

Meanwhile, the impacts of inflationary challenges can dent Omnicell’s performance. Intense competition from its peers further adds to the concern.

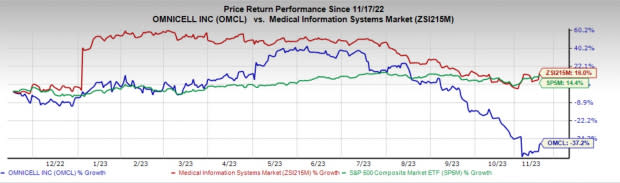

In the past year, this Zacks Rank #3 (Hold) stock has declined 37.2% against the 16% rise of the industry and the 14.4% growth of the S&P 500 composite.

The renowned healthcare technology company has a market capitalization of $1.50 billion. It has an earnings yield of 5.3% compared with the industry’s -7.8%. Omnicell surpassed estimates in all the trailing four quarters, delivering an average negative earnings surprise of 216.3%.

Let’s delve deeper.

Tailwinds

Robust Pipeline of Advanced Services Portfolio: Over the past few years, OMCL has made three key acquisitions — ReCept (later rebranded as Omnicell Specialty Pharmacy Services), FDS Amplicare and MarkeTouch Media, LL — intended to enhance advanced services offerings. Throughout the third quarter of 2023, the company continued to focus on executing the go-to-market strategy with these acquisitions, building on its momentum from the first half of the year.

Further, central pharmacy dispensing services continued to gain market traction, with several health systems choosing to automate their central pharmacy inventory and dispensing operations. In EnlivenHealth, Omnicell appears to be gaining momentum with cross-selling and upselling communication solutions to existing customers.

Image Source: Zacks Investment Research

Anticipated Benefits of Cost-Containment Measures: Last year, Omnicell introduced several restructuring initiatives to enhance and streamline certain engineering functions for its domestic operations and realign its international sales organization to better serve its customers in various international markets.

Earlier in 2023, the company committed to further reducing its headcount across many of its functions and also reducing its real estate footprint to align with its broader hybrid work strategy to lower costs. Moreover, management recently stated that more expense containment initiatives are underway to address ongoing macroeconomic headwinds.

Strong Liquidity and Capital Structure: Omnicell exited the third quarter of 2023 with cash and cash equivalents of $446.8 million, while short-term debt on its balance sheet was nil. This is indicative of a sound solvency position. Further, debt-to-capital at the third-quarter end was sequentially down by 0.4% to 32.4%.

Downsides

Rising Expenses May Strain Margins: Similar to its healthcare system partners, the company’s operations continue to be affected by persisting labor shortages and increased inflationary costs related to components’ raw materials and freight.

In the third quarter of 2023, Omnicell reported a year-over-year decrease in both gross and operating profit. For the full year 2023, management anticipates cost-savings measures to be partially offset by year-over-year increases in compensation and vendor price increases.

A Competitive Landscape: Omnicell’s operations are subjected to continued and increased competition from current and future competitors in the medication management automation solution market and the medication adherence solution market, including price competition, industry and competitor consolidation, competitor brand recognition and in terms of relationships with the suppliers and current and potential customers. This increased competition could result in pricing pressure and a reduced margin, which may have an adverse impact on the company’s performance.

Estimate Trend

The Zacks Consensus Estimate for OMCL’s 2023 earnings per share has remained constant at $1.76 in the past 60 days.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $1.14 billion. This suggests an 11.7% fall from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Haemonetics HAE, Insulet PODD and DexCom DXCM.

Haemonetics has an estimated earnings growth rate of 27.1% for fiscal 2024 compared with the industry’s 17.2%. HAE’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 19.39%. Its shares have rallied 13.2% against the industry’s 6.7% fall in the past year.

HAE carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Insulet, sporting a Zacks Rank #1 at present, has a long-term estimated earnings growth rate of 41.5% compared with the industry’s 12.2%. Shares of the company have decreased 41.6% compared with the industry’s 6.7% decline over the past year.

PODD’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 126.9%. In the last reported quarter, it delivered an average earnings surprise of 58.3%.

DexCom, carrying a Zacks Rank #2 at present, has an estimated long-term earnings growth rate of 33.6% compared with the industry’s 14.3%. Shares of DXCM have fallen 9.4% compared with the industry’s 7.2% decline over the past year.

DXCM’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 36.4%. In the last reported quarter, it delivered an average earnings surprise of 47.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL) : Free Stock Analysis Report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report