Here's Why You Should Retain QIAGEN (QGEN) Stock for Now

QIAGEN N.V. QGEN is likely to grow in the coming quarters, backed by its solid prospects in the Molecular Diagnostics space. R&D-based strategic partnerships buoy optimism for the company. Advancements in the testing menu expansion strategy are propelling QIAGEN’s growth. Meanwhile, increasing macroeconomic challenges and a competitive landscape remain concerns for the company.

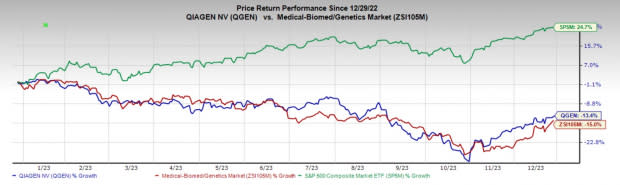

In the past year, this Zacks Rank #3 (Hold) stock has declined 13.4% compared with the 15% decrease of the industry. Meanwhile, the S&P 500 composite has witnessed a 24.7% rise in the said time frame.

The renowned global provider of sample and assay technologies has a market capitalization of $9.91 billion. QIAGEN has an earnings yield of 4.74% compared with the industry’s -34.3%. QGEN’s earnings surpassed estimates in all the trailing four quarters, delivering an average surprise of 6.3%.

Let’s delve deeper.

Upsides

Huge Potential in Molecular Diagnostics: QIAGEN offers one of the broadest portfolios of molecular technologies for healthcare. The company has built a position as a preferred partner to co-develop companion diagnostics paired with targeted drugs. It has created a rich pipeline of molecular tests that are transforming the treatment of cancer and other diseases.

Image Source: Zacks Investment Research

QIAGEN’s market-leading QuantiFERON latent TB test delivered an outstanding third quarter of 2023, with quarterly sales rising above $100 million for the first time. The QIAcuity digital PCR system delivered more than 40% sales growth at CER, driven by new placements and increasing biopharma consumable sales. The QIAstat diagnostic syndromic testing platform also did well this quarter with a combination of growth in consumables, driven by double-digit CER gains in noncoding testing and placements above the same level achieved in the third quarter of last year.

Strategic Collaborations to Drive Growth: QIAGEN’s long-term business strategy involves entering into strategic alliances as well as marketing and distribution arrangements with academic, corporate and other partners relating to the development, commercialization, marketing and distribution of certain of their existing and potential products.

In November 2023, the company announced a strategic collaboration with Element Biosciences, Inc. to offer comprehensive next-generation sequencing (NGS) workflows for Element’s sequencing platform, AVITI System. Earlier to that, QIAGEN and Myriad Genetics partnered to develop companion diagnostic tests in the field of cancer.

Progress in Test Menu Expansion: QIAGEN is progressing well with its testing menu expansion strategy, which is driving the company’s growth. In October 2023, QIAGEN expanded the QuantiFERON portfolio with the QuantiFERON-EBV RUO (Research Use Only) assay. In September 2023, the company added two new nucleic acid extraction kits — the QIAwave RNeasy Plus Mini Kit and the QIAwave DNA/RNA Mini Kit — extending its eco-friendly QIAwave product line.

Earlier, the company received FDA approval for its therascreen PDGFRA RGQ PCR kit (therascreen PDGFRA kit), which is intended to aid clinicians in identifying patients with gastrointestinal stromal tumors (GIST) who may be eligible for treatment with AYVAKIT (avapritinib).

Downsides

Macro Headwinds Hamper Global Sales: QIAGEN’s international operations are subject to a variety of risks arising from the economy, political outlook, language and cultural barriers in the countries it operates. In many of these emerging markets, QIAGEN faces several challenges, which include economies that may be dependent on only a few products and are, therefore, subject to significant fluctuations. Further, weak legal systems may affect its ability to enforce contractual rights, exchange controls, unstable governments and privatization or other government actions affecting the flow of goods and currency.

Competitive Headwinds: The company is facing increasing competition from firms that provide competitive pre-analytical solutions and other products used by QIAGEN’s customers. The markets for some of the company’s products are very competitive and price-sensitive. Other product suppliers may have significant advantages in terms of financial, operational, sales and marketing resources and experience in research and development.

According to the company, customers in the market for pre-analytical sample technologies and assay technologies display significant loyalty to their initial supplier of a particular product. As a result, it may not be easy to convert customers who have purchased products from competitors.

Estimate Trend

In the past 30 days, the Zacks Consensus Estimate for QIAGEN’s 2023 earnings per share has remained constant at $2.06.

The Zacks Consensus Estimate for the company’s 2023 revenues is pegged at $1.96 billion. This suggests a decrease of 8.4% from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Haemonetics HAE, Insulet PODD and DexCom DXCM.

Haemonetics has an estimated earnings growth rate of 28.4% for fiscal 2024 compared with the industry’s 15.2%. HAE’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 16.1%. Its shares have increased 10.3% compared with the industry’s 2.3% rise in the past year.

HAE carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Insulet, sporting a Zacks Rank #1 at present, has a long-term estimated earnings growth rate of 39.2% compared with the industry’s 11.7%. Shares of the company have decreased 25% against the industry’s 2.3% rise over the past year.

PODD’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 105.1%. In the last reported quarter, it delivered an average earnings surprise of 77.5%.

DexCom, carrying a Zacks Rank #2 at present, has an estimated long-term earnings growth rate of 33.6% compared with the industry’s 13.8%. Shares of DXCM have increased 10.2% compared to the industry’s 3.6% rise over the past year.

DXCM’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 36.4%. In the last reported quarter, it delivered an average earnings surprise of 47.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report

QIAGEN N.V. (QGEN) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report