Here's Why Science Applications International (NYSE:SAIC) Can Manage Its Debt Responsibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Science Applications International Corporation (NYSE:SAIC) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Science Applications International

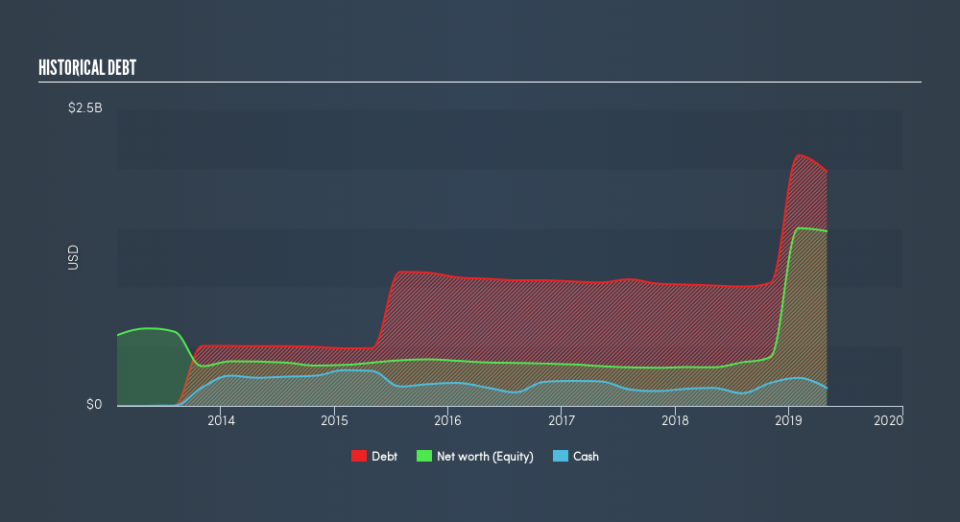

What Is Science Applications International's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of May 2019 Science Applications International had US$1.98b of debt, an increase on US$1.02b, over one year. However, it does have US$151.0m in cash offsetting this, leading to net debt of about US$1.83b.

A Look At Science Applications International's Liabilities

We can see from the most recent balance sheet that Science Applications International had liabilities of US$1.01b falling due within a year, and liabilities of US$2.12b due beyond that. On the other hand, it had cash of US$151.0m and US$1.04b worth of receivables due within a year. So its liabilities total US$1.94b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Science Applications International has a market capitalization of US$4.80b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Science Applications International has a debt to EBITDA ratio of 4.4 and its EBIT covered its interest expense 5.2 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Also relevant is that Science Applications International has grown its EBIT by a very respectable 26% in the last year, thus enhancing its ability to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Science Applications International's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Science Applications International generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Science Applications International's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But we must concede we find its net debt to EBITDA has the opposite effect. Looking at all the aforementioned factors together, it strikes us that Science Applications International can handle its debt fairly comfortably. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. We'd be motivated to research the stock further if we found out that Science Applications International insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.