Here's Why Shareholders Should Examine Route1 Inc.'s (CVE:ROI) CEO Compensation Package More Closely

Key Insights

Route1 to hold its Annual General Meeting on 29th of November

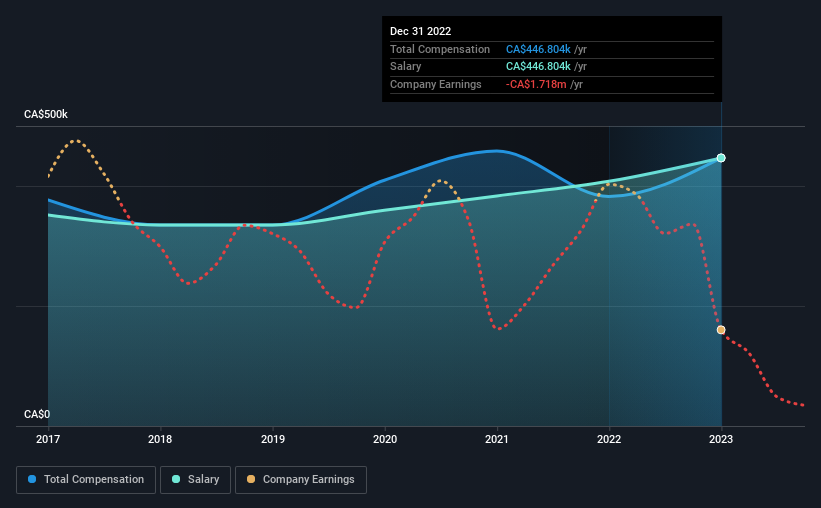

Salary of CA$446.8k is part of CEO Tony Busseri's total remuneration

The total compensation is 36% higher than the average for the industry

Route1's three-year loss to shareholders was 98% while its EPS was down 41% over the past three years

Shareholders will probably not be too impressed with the underwhelming results at Route1 Inc. (CVE:ROI) recently. At the upcoming AGM on 29th of November, shareholders can hear from the board including their plans for turning around performance. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for Route1

Comparing Route1 Inc.'s CEO Compensation With The Industry

Our data indicates that Route1 Inc. has a market capitalization of CA$1.1m, and total annual CEO compensation was reported as CA$447k for the year to December 2022. That's a notable increase of 17% on last year. Notably, the salary of CA$447k is the entirety of the CEO compensation.

On comparing similar-sized companies in the Canadian Software industry with market capitalizations below CA$274m, we found that the median total CEO compensation was CA$329k. This suggests that Tony Busseri is paid more than the median for the industry.

Component | 2022 | 2021 | Proportion (2022) |

Salary | CA$447k | CA$408k | 100% |

Other | - | - | |

Total Compensation | CA$447k | CA$383k | 100% |

Speaking on an industry level, nearly 71% of total compensation represents salary, while the remainder of 29% is other remuneration. Speaking on a company level, Route1 prefers to tread along a traditional path, disbursing all compensation through a salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Route1 Inc.'s Growth

Over the last three years, Route1 Inc. has shrunk its earnings per share by 41% per year. Its revenue is down 35% over the previous year.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Route1 Inc. Been A Good Investment?

Few Route1 Inc. shareholders would feel satisfied with the return of -98% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Route1 pays CEO compensation exclusively through a salary, with non-salary compensation completely ignored. Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 4 warning signs for Route1 you should be aware of, and 3 of them don't sit too well with us.

Important note: Route1 is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.