Here's Why Spectrum Brands (SPB) is Marching Ahead of Its Industry

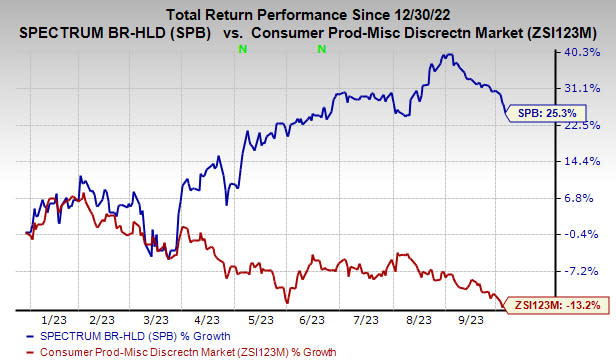

Spectrum Brands SPB has been gaining from increased pricing, cost improvements and a favorable mix. It is on track with the Global Productivity Improvement Plan and strategic transformation plans. Driven by these factors, shares of this Zacks Rank #3 (Hold) company have gained 25.3% year to date against the industry’s decline of 13.2%.

This led to a gross margin expansion of 210 bps to 35.8% in third-quarter fiscal 2023. Adjusted EBITDA advanced 23% to $98.5 million and beat our estimate of $89.3 million. Meanwhile, the adjusted EBITDA margin expanded 360 bps to 13.4%, driven by lower distribution costs, fixed-cost-reduction initiatives and positive pricing impacts, partly offset by reduced volume. Consequently, adjusted earnings were 75 cents per share, up 39% year over year.

Additionally, an uptrend in the Zacks Consensus Estimate echoes the same sentiment. The Zacks Consensus Estimate for SPB’s fiscal 2023 earnings for the current financial year has risen 51% in the past 60 days.

Image Source: Zacks Investment Research

Let’s delve deeper

Spectrum Brands is streamlining its organizational structure and re-energizing the employee base. The company is committed to improving operational efficiencies throughout and limiting risks. Management is protecting and deleveraging its balance sheet while solidifying liquidity. It is focused on transforming the company into a pure-play global Pet and Home & Garden business.

As part of its strategic transformation, the company completed the sale of HHI to ASSA ABLOY for $4.3 billion in cash on Jun 20, subject to customary purchase price adjustments. It expects $3.8 billion in net proceeds from this sale. With the sale of the HHI business, the company can refocus on its core businesses and boast a stronger balance sheet.

SPB is progressing well with its Global Productivity Improvement Plan (“GPIP”), which aims at improving the company's operating efficiency and effectiveness, while focusing on consumer insights and growth-enabling functions, including technology, marketing, and research and development. The majority of the savings are expected to be reinvested into the growth initiatives and consumer insights, R&D, and marketing across each of the businesses.

Headwinds

Spectrum Brands has been witnessing lower demand, cooler-than-expected weather and reduced retail inventory that hurt its Home and Garden business in third-quarter fiscal 2023. The segment's sales declined 6% to $186.6 million due to lower-than-expected replenishment orders for the pest control category, lower-than-expected POS and adverse weather conditions. The metric lagged our estimate of $204.3 million. Sluggishness in the small home appliance space due to lower consumer demand and continued higher-than-expected retail inventory levels acted as deterrents.

Consequently, the top line fell 10% year over year to $735.5 million and lagged the Zacks Consensus Estimate of $781 million. Organic net sales declined 9.7%. For fiscal 2023, the company expects a mid-single-digit sales decline. This includes the adverse impacts of foreign currency. It also expects short-term demand headwinds to continue in the fiscal fourth quarter.

Wrapping Up

All said, we expect Spectrum Brands to stay afloat through the ongoing tough economic landscape on the back of its transformation efforts, favorable pricing and cost-reduction initiatives.

The PEG ratio for SPB is just 0.71, lower than the industry average of 0.82. The PEG ratio is a modified PE ratio that takes into account the stock’s earnings growth rate. Clearly, Spectrum Brands is a solid choice on the value front from multiple angles. Notably, a Value Score of B raises optimism in the stock.

Stocks to Consider

Some better-ranked companies are MGM Resorts MGM, Royal Caribbean RCL and Crocs CROX.

MGM Resorts currently sports a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 81%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for MGM’s 2024 sales and EPS indicates year-over-year increases of 2.2% and 31%, respectively.

Royal Caribbean flaunts a Zacks Rank #1 at present. RCL has a trailing four-quarter earnings surprise of 26.4%, on average.

The Zacks Consensus Estimate for RCL’s 2023 sales and EPS indicates increases of 47.9% and 158.3%, respectively, from the year-ago period’s reported levels.

Crocs, which offers casual lifestyle footwear and accessories, presently carries a Zacks Rank #2 (Buy). The expected EPS growth rate for three to five years is 15%.

The Zacks Consensus Estimate for Crocs’ current financial-year sales and earnings suggests growth of 13.1% and 2.8%, respectively, from the year-ago period’s reported figure. CROX has a trailing four-quarter earnings surprise of 21.8%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

MGM Resorts International (MGM) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Spectrum Brands Holdings Inc. (SPB) : Free Stock Analysis Report