Here's Why We Think B.O.S. Better Online Solutions (NASDAQ:BOSC) Is Well Worth Watching

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like B.O.S. Better Online Solutions (NASDAQ:BOSC). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide B.O.S. Better Online Solutions with the means to add long-term value to shareholders.

View our latest analysis for B.O.S. Better Online Solutions

B.O.S. Better Online Solutions' Improving Profits

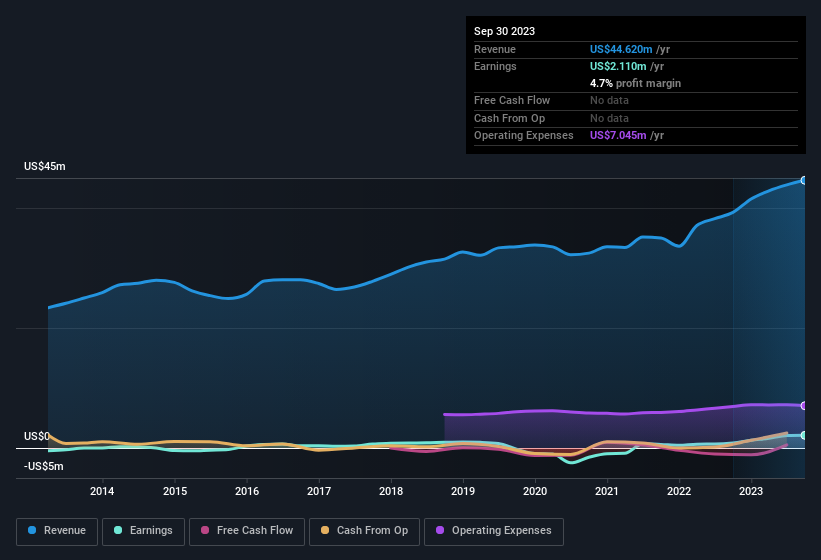

B.O.S. Better Online Solutions has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. So it would be better to isolate the growth rate over the last year for our analysis. Outstandingly, B.O.S. Better Online Solutions' EPS shot from US$0.16 to US$0.37, over the last year. Year on year growth of 136% is certainly a sight to behold.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. The good news is that B.O.S. Better Online Solutions is growing revenues, and EBIT margins improved by 2.9 percentage points to 6.1%, over the last year. Ticking those two boxes is a good sign of growth, in our book.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Since B.O.S. Better Online Solutions is no giant, with a market capitalisation of US$16m, you should definitely check its cash and debt before getting too excited about its prospects.

Are B.O.S. Better Online Solutions Insiders Aligned With All Shareholders?

Prior to investment, it's always a good idea to check that the management team is paid reasonably. Pay levels around or below the median, can be a sign that shareholder interests are well considered. The median total compensation for CEOs of companies similar in size to B.O.S. Better Online Solutions, with market caps under US$200m is around US$662k.

B.O.S. Better Online Solutions' CEO took home a total compensation package worth US$357k in the year leading up to December 2022. That is actually below the median for CEO's of similarly sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of a culture of integrity, in a broader sense.

Is B.O.S. Better Online Solutions Worth Keeping An Eye On?

B.O.S. Better Online Solutions' earnings have taken off in quite an impressive fashion. With increasing profits, its seems likely the business has a rosy future; and it may have hit an inflection point. Meanwhile, the very reasonable CEO pay is a great reassurance, since it points to an absence of wasteful spending habits. It will definitely require further research to be sure, but it does seem that B.O.S. Better Online Solutions has the hallmarks of a quality business; and that would make it well worth watching. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for B.O.S. Better Online Solutions that you should be aware of.

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in the US with promising growth potential and insider confidence.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.