Here's Why We Think Coronation Fund Managers Limited's (JSE:CML) CEO Compensation Looks Fair

Performance at Coronation Fund Managers Limited (JSE:CML) has been rather uninspiring recently and shareholders may be wondering how CEO Anton Pillay plans to fix this. They will get a chance to exercise their voting power to influence the future direction of the company in the next AGM on 22 February 2023. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. In our opinion, CEO compensation does not look excessive and we discuss why.

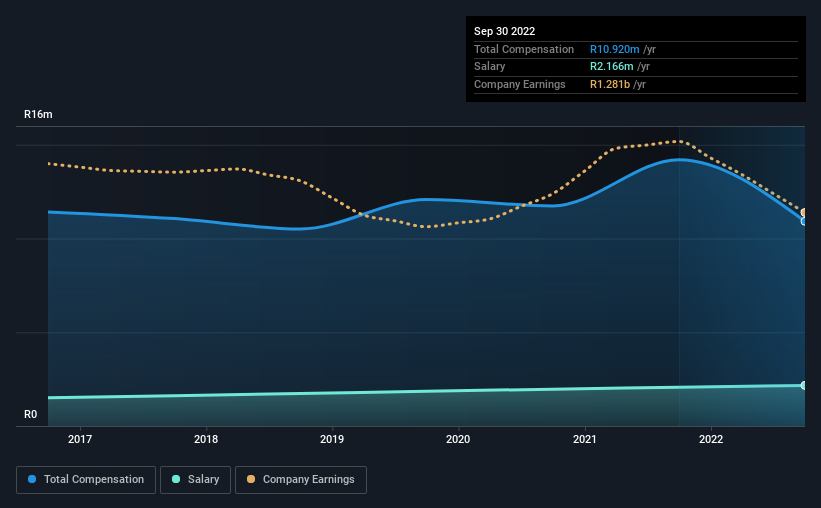

See our latest analysis for Coronation Fund Managers

How Does Total Compensation For Anton Pillay Compare With Other Companies In The Industry?

According to our data, Coronation Fund Managers Limited has a market capitalization of R11b, and paid its CEO total annual compensation worth R11m over the year to September 2022. We note that's a decrease of 23% compared to last year. We think total compensation is more important but our data shows that the CEO salary is lower, at R2.2m.

For comparison, other companies in the South Africa Capital Markets industry with market capitalizations ranging between R7.2b and R29b had a median total CEO compensation of R21m. Accordingly, Coronation Fund Managers pays its CEO under the industry median. Furthermore, Anton Pillay directly owns R151m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2022 | 2021 | Proportion (2022) |

Salary | R2.2m | R2.1m | 20% |

Other | R8.8m | R12m | 80% |

Total Compensation | R11m | R14m | 100% |

On an industry level, roughly 39% of total compensation represents salary and 61% is other remuneration. Coronation Fund Managers sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Coronation Fund Managers Limited's Growth Numbers

Over the past three years, Coronation Fund Managers Limited has seen its earnings per share (EPS) grow by 2.3% per year. In the last year, its revenue is down 14%.

We generally like to see a little revenue growth, but the modest improvement in EPS is good. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Coronation Fund Managers Limited Been A Good Investment?

Given the total shareholder loss of 5.5% over three years, many shareholders in Coronation Fund Managers Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Flat earnings growth may also be to blame for the uninspiring share price performance. Shareholders will get the chance to question the board on key concerns and revisit their investment thesis with regards to the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 2 warning signs for Coronation Fund Managers that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here