Here's Why We Think First US Bancshares (NASDAQ:FUSB) Is Well Worth Watching

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in First US Bancshares (NASDAQ:FUSB). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide First US Bancshares with the means to add long-term value to shareholders.

View our latest analysis for First US Bancshares

How Quickly Is First US Bancshares Increasing Earnings Per Share?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. That means EPS growth is considered a real positive by most successful long-term investors. First US Bancshares' shareholders have have plenty to be happy about as their annual EPS growth for the last 3 years was 48%. That sort of growth rarely ever lasts long, but it is well worth paying attention to when it happens.

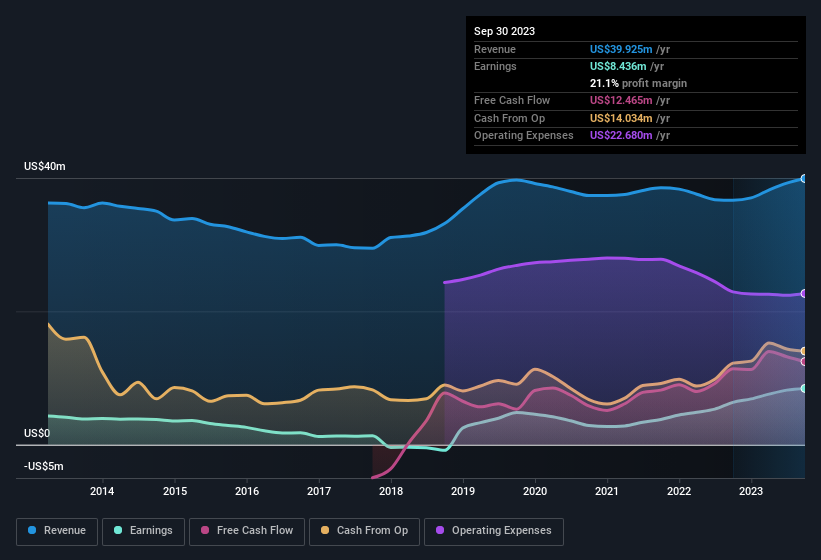

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Our analysis has highlighted that First US Bancshares' revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. First US Bancshares maintained stable EBIT margins over the last year, all while growing revenue 8.9% to US$40m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

First US Bancshares isn't a huge company, given its market capitalisation of US$55m. That makes it extra important to check on its balance sheet strength.

Are First US Bancshares Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We note that First US Bancshares insiders spent US$53k on stock, over the last year; in contrast, we didn't see any selling. That's nice to see, because it suggests insiders are optimistic. Zooming in, we can see that the biggest insider purchase was by Independent Chairman of the Board Robert Briggs for US$26k worth of shares, at about US$8.60 per share.

Is First US Bancshares Worth Keeping An Eye On?

First US Bancshares' earnings per share have been soaring, with growth rates sky high. Growth-minded people will be intrigued by the incredible movement in EPS growth. And indeed, it could be a sign that the business is at an inflection point. If this these factors intrigue you, then an addition of First US Bancshares to your watchlist won't go amiss. You still need to take note of risks, for example - First US Bancshares has 2 warning signs we think you should be aware of.

Keen growth investors love to see insider buying. Thankfully, First US Bancshares isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by recent insider buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.