Here's Why Urban Outfitters (URBN) is Thriving in the Industry

Urban Outfitters Inc. URBN has exhibited a decent run on the bourses in the past year. The company is strategically positioning itself by leveraging its diverse brand portfolio and innovative business models, and embracing technological advancements.

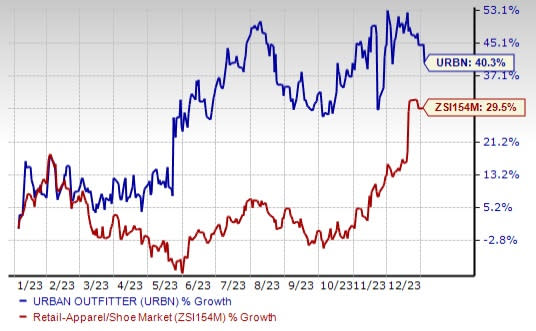

The stock has outpaced the industry over time. In the said period, shares of this presently Zacks Rank #3 (Hold) player have risen 40.3% compared with the industry’s growth of 29.5%.

Image Source: Zacks Investment Research

Let’s Delve Deeper

URBN's marketing efforts and product offerings have driven customer growth and engagement, particularly for the Anthropologie and Free People brands. This success in marketing indicates a strong connection with the target audience and effectiveness in brand positioning.

The Anthropologie, Free People and FP Movement brands all produced double-digit sales growth in stores and online in third-quarter fiscal 2024. FP Movement was driven by a 49% year-over-year rise in comp sales.

The company sees a lot of opportunity from its rental subscription business, Nuuly. Strong execution, focus on customer value and curated assortments have helped it grow, which continued in the fiscal third quarter as well. In the quarter, Nuuly experienced a remarkable 86% increase in revenues from the previous year. With nearly 39,000 subscribers added in the quarter, Nuuly's success showcases URBN's prowess in adapting to evolving consumer preferences.

The company is advancing its digital capabilities by taking several initiatives. These technologies are expected to streamline product development, improve demand forecasting, optimize inventory and enable more personalized marketing. The company is particularly excited about generative AI enhancing its creative capabilities, aiming to realize significant efficiency improvements, waste reduction and cost savings across various functions.

Urban Outfitters expects a capital expenditure of $235 million for fiscal 2024. This investment primarily focuses on additional distribution facilities. Notably, the company has opened a highly automated omni fulfillment facility in Kansas City, KS. Additionally, URBN is investing in a new rental fulfillment facility in Missouri, within the Kansas City region, slated to open in early fiscal 2025.

While the overall performance is stellar, challenges persist, particularly in the Urban Outfitters brand. With negative 14% Retail segment comps in the fiscal third quarter, the brand faces the task of repositioning itself in the market. The company is addressing this through its focus on product assortment, brand relevance and improved marketing efforts.

URBN’s effective business strategies, expansion efforts in retail and a strong foundation bode well. The company is focusing on enhancing its direct-to-consumer operations, improving productivity across its existing channels and effectively managing inventory levels. These initiatives will propel the company's prosperity in the near future.

3 Hot Stocks to Consider

A few better-ranked stocks are The Gap, Inc. GPS, Abercrombie & Fitch Co. ANF and Deckers Outdoor Corporation DECK.

The Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Gap’s current fiscal-year sales indicates growth of 387.5% from the previous year’s reported figures. GPS has a trailing four-quarter average earnings surprise of 138%.

Abercrombie & Fitch is a specialty retailer of premium, high-quality casual apparel. The company currently flaunts a Zacks Rank #1. ANF delivered a 60.5% earnings surprise in the last reported quarter.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current fiscal-year sales implies growth of 13.3% from the previous year’s reported number. ANF has a trailing four-quarter average earnings surprise of 713%.

Deckers is a leading designer, producer and brand manager of innovative, niche footwear and accessories. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Deckers’ current fiscal-year earnings and sales indicates growth of 21.9% and 11.7%, respectively, from the previous year’s reported figures. DECK has a trailing four-quarter average earnings surprise of 26.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

The Gap, Inc. (GPS) : Free Stock Analysis Report

Urban Outfitters, Inc. (URBN) : Free Stock Analysis Report