Here's Why We're Wary Of Buying Deluxe's (NYSE:DLX) For Its Upcoming Dividend

Deluxe Corporation (NYSE:DLX) stock is about to trade ex-dividend in 4 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Therefore, if you purchase Deluxe's shares on or after the 16th of February, you won't be eligible to receive the dividend, when it is paid on the 4th of March.

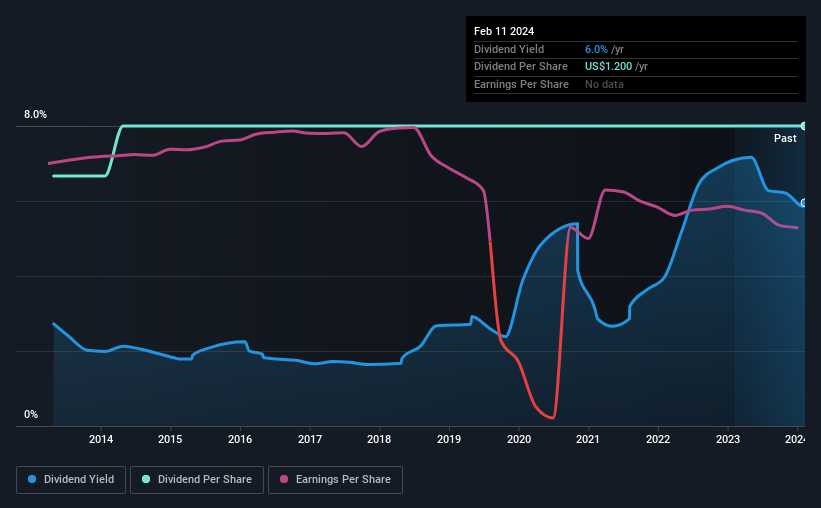

The company's next dividend payment will be US$0.30 per share. Last year, in total, the company distributed US$1.20 to shareholders. Calculating the last year's worth of payments shows that Deluxe has a trailing yield of 6.0% on the current share price of US$20.16. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Deluxe can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Deluxe

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Deluxe paid out a disturbingly high 201% of its profit as dividends last year, which makes us concerned there's something we don't fully understand in the business. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Dividends consumed 55% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Deluxe fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. Deluxe's earnings per share have fallen at approximately 28% a year over the previous five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past 10 years, Deluxe has increased its dividend at approximately 1.8% a year on average.

Final Takeaway

From a dividend perspective, should investors buy or avoid Deluxe? Earnings per share have been in decline, which is not encouraging. What's more, Deluxe is paying out a majority of its earnings and over half its free cash flow. It's hard to say if the business has the financial resources and time to turn things around without cutting the dividend. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Although, if you're still interested in Deluxe and want to know more, you'll find it very useful to know what risks this stock faces. For example, we've found 4 warning signs for Deluxe (1 makes us a bit uncomfortable!) that deserve your attention before investing in the shares.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.