Heritage Commerce Corp Just Missed Earnings And Its EPS Looked Sad - But Analysts Have Updated Their Models

Heritage Commerce Corp (NASDAQ:HTBK) shares fell 6.7% to US$11.58 in the week since its latest annual results. It was not a great result overall. While revenues of US$141m were in line with analyst predictions, earnings were less than expected, missing statutory estimates by 11% to hit US$0.84 per share. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what analysts are expecting for next year.

View our latest analysis for Heritage Commerce

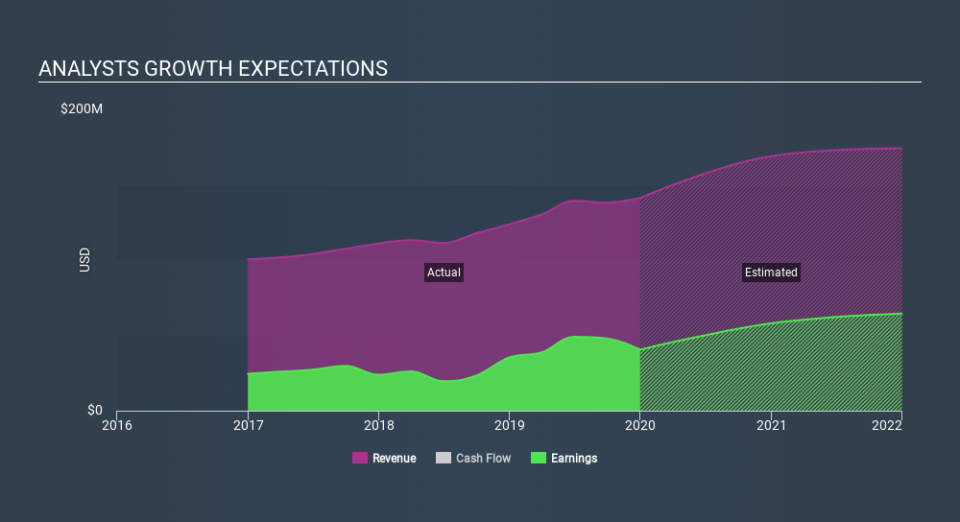

Taking into account the latest results, the most recent consensus for Heritage Commerce from five analysts is for revenues of US$168.9m in 2020, which is a notable 20% increase on its sales over the past 12 months. Statutory earnings per share are expected to step up 13% to US$0.98. Before this earnings report, analysts had been forecasting revenues of US$171.6m and earnings per share (EPS) of US$0.96 in 2020. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

Analysts reconfirmed their price target of US$14.40, showing that the business is executing well and in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Heritage Commerce analyst has a price target of US$15.00 per share, while the most pessimistic values it at US$14.00. Still, with such a tight range of estimates, it suggests analysts have a pretty good idea of what they think the company is worth.

Zooming out to look at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up both against past performance, and against industry growth estimates. Analysts are definitely expecting Heritage Commerce's growth to accelerate, with the forecast 20% growth ranking favourably alongside historical growth of 14% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.0% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Heritage Commerce is expected to grow much faster than its market.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - and our data does suggest that Heritage Commerce's revenues are expected to grow faster than the wider market. The consensus price target held steady at US$14.40, with the latest estimates not enough to have an impact on analysts' estimated valuations.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Heritage Commerce analysts - going out to 2021, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.