IDEXX (IDXX) Stock Up 18.4% YTD: Will the Rally Continue?

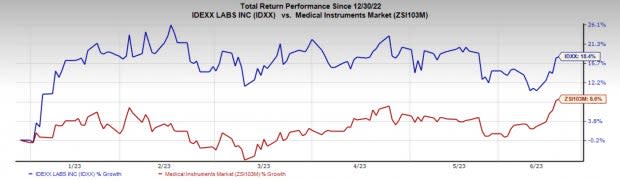

IDEXX Laboratories, Inc.‘s IDXX shares have surged 18.4% year to date compared with the industry’s increase of 8.6%. The Medical sector has declined 1.3% in the said time frame. The company has a market capitalization of $40.09 billion.

The continued solid demand for veterinary services and benefits from strong IDEXX execution and expanded global premium instrument placements continue to drive this Zacks Rank #3 (Hold) company. Its earnings increased 18.9% in the last five years, better than the industry average of 4.2%.

IDEXX’s ROE for the trailing 12 months was 117.4%, better than the industry average of (34.9%). It has a Growth Score of B. The Growth Score analyzes the growth prospects for a company and also evaluates its corporate financial statements.

Will the Upside Continue?

The Zacks Consensus Estimate for IDEXX’s 2023 earnings is pegged at $9.65, indicating a 20.2% increase from the year-ago reported figure. The consensus estimate for 2023 revenues is pegged at $3.66, indicating a year-over-year improvement of 8.6%.

IDEXX’s strong global performance represents major growth catalyst. International revenues in the first quarter were aided by a gain in CAG and Water businesses. Globally, IDEXX achieved strong organic revenue growth across its modalities in the said quarter. The year-on-year growth on global premium instrument installed base reflecting double-digit increases across Catalyst, Premium Hematology and SediVue platforms is expected to boost the company’s performance in coming quarters.

CAG premium instrument placements increased 3% in the first quarter. The quality of instrument placements continues to be excellent, reflecting a 7% growth in new and competitive Catalyst placements. ProCyte One momentum also continues to be strong globally, reflecting on a global installed base that more than doubled over the last year to 9,400 units.

Image Source: Zacks Investment Research

The solid CAG Diagnostics recurring revenue growth continues to be a key growth driver for the company, supported by global net price gains. Solid U.S. volume growth is also expected to be supported by new business gains, high customer retention levels and continued increases in diagnostic frequency and utilization at the practice level.

International CAG Diagnostics’ recurring revenue gains were supported by strong IDEXX execution. Higher net price realization, sustained new business gains and a double-digit expansion of premium instrument installed base are other tailwinds.

The raised 2023 guidance is an indicator of continued future growth. For 2023, the company expects revenue growth in the range of $3.615-$3,700, indicating growth of 7.5-10% on a reported and organic basis (up from the previous guidance of $3,590-$3,690 million). The Zacks Consensus Estimate for the same is currently pegged at $3.63 billion.

IDEXX’s full-year earnings per share guidance is now pegged in the range of $9.33-$9.75, indicating a rise of 16-21% on a reported basis (up from the previous guidance of $9.27-$9.75). The Zacks Consensus Estimate for full-year earnings per share is currently pegged at $9.61.

Estimate Trends

The Zacks Consensus Estimate for IDXX’s 2023 and 2024 has moved 0.7% and 5.2% north, respectively, in the past 90 days that indicate analyst’s optimism.

Key Picks

Some better-ranked stocks in the broader medical space are CONMED CNMD, Merit Medical Systems, Inc. MMSI and Boston Scientific Corporation BSX.

CONMED, carrying Zacks Rank# 2 (Buy), has an estimated long-term growth rate of 19.4%. The company’s earnings surpassed estimates in two of the trailing four quarters, missed once and met in another, delivering a negative average surprise of 10.54%.

CNMD’s shares have risen 53.8% in the past year compared with the industry’s 24.2% growth. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merit Medical, currently carrying a Zacks Rank #2, has an estimated long-term growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 20.2%.

Merit Medical has improved 60.2% compared with the industry’s 24.2% growth in the past year.

Boston Scientific, presently holding a Zacks Rank #2, has an estimated long-term growth rate of 11.5%. BSX’s earnings surpassed estimates in two of the trailing four quarters and missed twice, the average surprise being 1.9%.

Boston Scientific has gained 50.8% against the industry’s 18.1% decline in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

CONMED Corporation (CNMD) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

IDEXX Laboratories, Inc. (IDXX) : Free Stock Analysis Report