Should You Be Impressed By Illinois Tool Works' (NYSE:ITW) Returns on Capital?

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at Illinois Tool Works (NYSE:ITW), they do have a high ROCE, but we weren't exactly elated from how returns are trending.

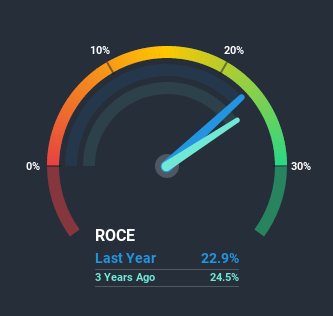

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Illinois Tool Works is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.23 = US$2.8b ÷ (US$15b - US$2.5b) (Based on the trailing twelve months to September 2020).

So, Illinois Tool Works has an ROCE of 23%. In absolute terms that's a great return and it's even better than the Machinery industry average of 10%.

See our latest analysis for Illinois Tool Works

In the above chart we have measured Illinois Tool Works' prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Can We Tell From Illinois Tool Works' ROCE Trend?

Things have been pretty stable at Illinois Tool Works, with its capital employed and returns on that capital staying somewhat the same for the last five years. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. Although current returns are high, we'd need more evidence of underlying growth for it to look like a multi-bagger going forward. This probably explains why Illinois Tool Works is paying out 58% of its income to shareholders in the form of dividends. Given the business isn't reinvesting in itself, it makes sense to distribute a portion of earnings among shareholders.

The Bottom Line On Illinois Tool Works' ROCE

Although is allocating it's capital efficiently to generate impressive returns, it isn't compounding its base of capital, which is what we'd see from a multi-bagger. Yet to long term shareholders the stock has gifted them an incredible 155% return in the last five years, so the market appears to be rosy about its future. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

If you want to continue researching Illinois Tool Works, you might be interested to know about the 1 warning sign that our analysis has discovered.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.