Improved Revenues Required Before EnQuest PLC (LON:ENQ) Shares Find Their Feet

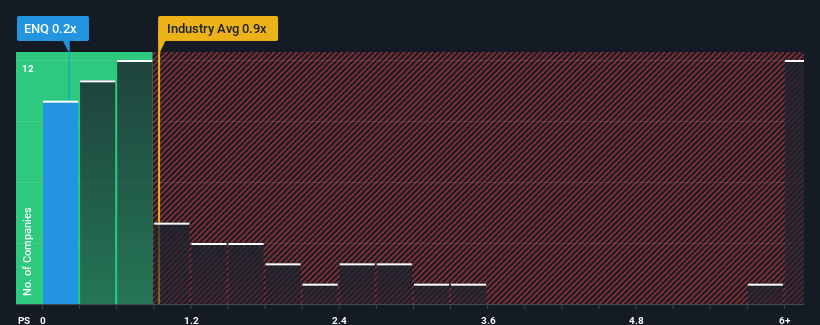

With a price-to-sales (or "P/S") ratio of 0.2x EnQuest PLC (LON:ENQ) may be sending bullish signals at the moment, given that almost half of all the Oil and Gas companies in the United Kingdom have P/S ratios greater than 0.9x and even P/S higher than 3x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for EnQuest

How Has EnQuest Performed Recently?

EnQuest's revenue growth of late has been pretty similar to most other companies. It might be that many expect the mediocre revenue performance to degrade, which has repressed the P/S ratio. If not, then existing shareholders have reason to be optimistic about the future direction of the share price.

Keen to find out how analysts think EnQuest's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Any Revenue Growth Forecasted For EnQuest?

The only time you'd be truly comfortable seeing a P/S as low as EnQuest's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 46%. As a result, it also grew revenue by 13% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to plummet, contracting by 17% each year during the coming three years according to the three analysts following the company. Meanwhile, the broader industry is forecast to moderate by 4.3% each year, which indicates the company should perform poorly indeed.

With this information, it's not too hard to see why EnQuest is trading at a lower P/S in comparison. However, when revenue shrink rapidly the P/S often shrinks too, which could set up shareholders for future disappointment. Even just maintaining these prices could be difficult to achieve as the weak outlook is already weighing down the shares heavily.

The Bottom Line On EnQuest's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As expected, our analysis of EnQuest's analyst forecasts confirms that the company's even more precarious outlook against the industry is a major contributor to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Although, we would be concerned whether the company can even maintain this level of performance under these tough industry conditions. For now though, it's hard to see the share price rising strongly in the near future under these circumstances.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for EnQuest with six simple checks will allow you to discover any risks that could be an issue.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here