Are Industrial Services of America Inc’s (NASDAQ:IDSA) Interest Costs Too High?

Industrial Services of America Inc (NASDAQ:IDSA) is a small-cap stock with a market capitalization of US$17.54M. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Since IDSA is loss-making right now, it’s crucial to understand the current state of its operations and pathway to profitability. I believe these basic checks tell most of the story you need to know. However, I know these factors are very high-level, so I’d encourage you to dig deeper yourself into IDSA here.

Does IDSA generate enough cash through operations?

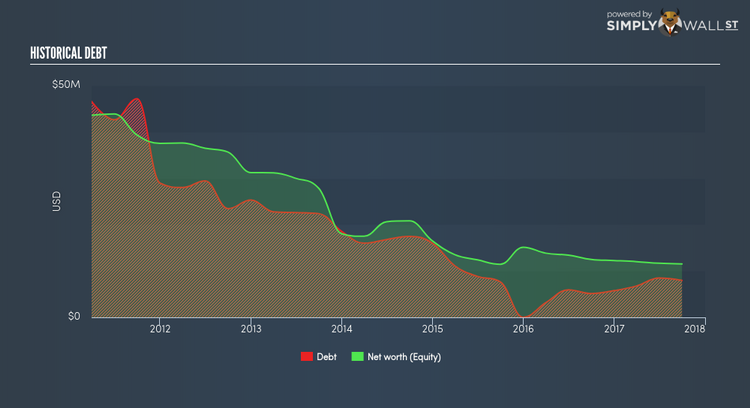

Over the past year, IDSA has ramped up its debt from US$20.00K to US$5.77M , which comprises of short- and long-term debt. With this growth in debt, IDSA currently has US$526.00K remaining in cash and short-term investments , ready to deploy into the business. Moving onto cash from operations, its small level of operating cash flow means calculating cash-to-debt wouldn’t be too useful, though these low levels of cash means that operational efficiency is worth a look. For this article’s sake, I won’t be looking at this today, but you can examine some of IDSA’s operating efficiency ratios such as ROA here.

Does IDSA’s liquid assets cover its short-term commitments?

With current liabilities at US$6.03M, it seems that the business has been able to meet these obligations given the level of current assets of US$7.70M, with a current ratio of 1.28x. For Commercial Services companies, this ratio is within a sensible range since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Can IDSA service its debt comfortably?

IDSA is a relatively highly levered company with a debt-to-equity of 69.23%. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. However, since IDSA is currently unprofitable, there’s a question of sustainability of its current operations. Maintaining a high level of debt, while revenues are still below costs, can be dangerous as liquidity tends to dry up in unexpected downturns.

Next Steps:

IDSA’s cash flow coverage indicates it could improve its operating efficiency in order to meet demand for debt repayments should unforeseen events arise. However, the company exhibits an ability to meet its near term obligations should an adverse event occur. Keep in mind I haven’t considered other factors such as how IDSA has been performing in the past. I suggest you continue to research Industrial Services of America to get a more holistic view of the stock by looking at:

1. Historical Performance: What has IDSA’s returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

2. Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.