Will Infrastructure Demand Continue to Aid Quanta (PWR)?

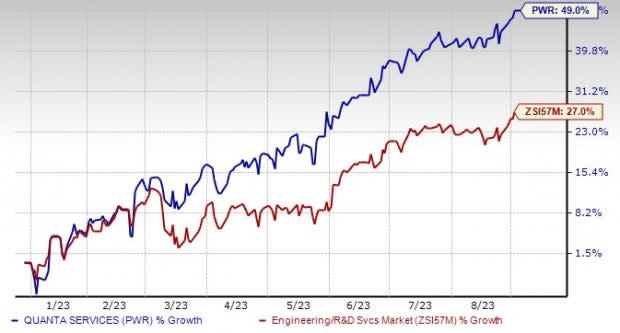

Quanta Services, Inc. PWR stock has gained 49% year to date, outperforming the Zacks Engineering - R and D Services industry’s 27% growth. The company has been gaining from the sustained demand in its end markets and the strength of its core business. The year 2023 exhibits widespread growth opportunities, with continuous growth opportunities for infrastructure solutions.

This Zacks Rank #3 (Hold) stock is also expected to gain from prudent growth strategies and accretive acquisitions.

The Zacks Consensus Estimate has witnessed an uptrend over the past 30 days as analysts raised their estimates. Over the said time frame, the Zacks Consensus Estimate for earnings of $7.09 for 2023 has increased from $7.01. The estimated figure indicates 11.8% year-over-year growth.

Image Source: Zacks Investment Research

However, project delays, supply chain risks and lower operating margins across the Electric and Renewable segments are concerns.

Let’s Take a Look at the Factors Supporting the Growth

High Infrastructural Investment: Quanta is expected to reap the rewards of its involvement in a wide range of technology solutions dedicated to decarbonization efforts. These encompass areas like carbon management mitigation, compliance consulting, and the complete spectrum of infrastructure required to facilitate carbon-free energy solutions. Quanta has been strategically positioned to capitalize on major trends driving the energy transition and fostering technological advancements. Notably, initiatives like the expansion of electric vehicle charging infrastructure and the undergrounding of electrical infrastructure are gaining significant traction, further contributing to the company's growth prospects.

Solid Backlog: The company ended the second quarter with a total record backlog of $27.2 billion and a 12-month backlog of $15.64 billion. This compares favorably with the December 2022-end’s 12-month backlog of $13.79 billion and the total backlog of $24.09 billion. The reported metrics were also up from the year-ago respective figures of $11.58 billion and $19.85 billion. This demonstrates the strength of its core operations. This robust performance underscores the company's core operational strength, and Quanta remains optimistic about its future prospects, driven by its healthy backlog levels, which are expected to continue growing.

Acquisitions: Quanta considers acquisitions as a pivotal element of its strategy to augment its market presence and expand its order backlog. As of January 2023, Quanta completed the acquisition of three companies. One of these specializes in providing services related to high-voltage transmission lines, overhead and underground distribution, emergency restoration, and industrial and commercial wiring and lighting. This acquisition primarily strengthens Quanta's presence in the Electric Power sector. Another acquired company offers solutions in the field of concrete construction services, bolstering Quanta's capabilities in both the Electric Power and Renewable Energy segments. The third acquisition involves a business focused on procuring components, assembling kits for sale, managing logistics, and installing solar tracking equipment for utility and development clients, primarily enhancing Quanta's operations within the Renewable Energy segment.

Hurdles

Lower Margins: Lower equity in earnings from its integral unconsolidated affiliates and lower utilization of Canadian resources have been impacting the Electric segment’s operating margins, which contracted 30 basis points (bps) and 50 bps in the first and second quarters of 2023, respectively.

Also, increased costs related to higher levels of resources required to support the expected increase in project activity in the second half of 2023 and into 2024 led to the contraction of the operating margin in Renewable Energy Infrastructure Solutions unit during the first and second quarters of 2023. Renewable Energy Infrastructure Solutions unit’s operating margin contracted 446 bps and 85 bps during the first and second quarters of 2023.

3 Construction Stocks to Consider

Gibraltar Industries, Inc. ROCK manufactures and distributes products to the industrial and buildings market. The Zacks Consensus Estimate for ROCK’s 2023 earnings has moved north to $3.97 per share from $3.56 in the past 30 days.

Shares of ROCK have gained 66.6% YTD. ROCK’s expected earnings growth rate for 2023 is 16.8% and sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Masco MAS manufactures, sells and installs home improvement and building products. Shares of MAS have gained 28% YTD.

Masco presently flaunts a Zacks Rank #1. The Zacks Consensus Estimate for MAS’ 2023 earnings has moved north to $3.60 per share from $3.56 in the past 30 days.

Fluor Corporation FLR benefits from its diverse presence in various markets, which allows it to reduce the impact of market fluctuations. The company adopts a strategic approach by maintaining a well-balanced business portfolio, enabling it to prioritize stable markets while taking advantage of opportunities in cyclical markets when the timing is appropriate.

FLR presently sports a Zacks Rank #1. Shares of FLR have gained 3% YTD. Nonetheless, its expected earnings growth rate for 2023 is 141.5%. The Zacks Consensus Estimate for FLR’s 2023 earnings has moved north to $1.98 per share from $1.74 in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR) : Free Stock Analysis Report

Fluor Corporation (FLR) : Free Stock Analysis Report

Masco Corporation (MAS) : Free Stock Analysis Report

Gibraltar Industries, Inc. (ROCK) : Free Stock Analysis Report