Insiders Bet on These 2 High-Yield Dividend Stocks – Here’s Why You Might Want to Follow in Their Footsteps

Trying to navigate the ups and downs of the stock market and predict its future direction can seem like a complicated and daunting task. However, as with almost anything, simplicity often holds the key. One of the most straightforward strategies is to keep an eye out for insiders’ moves.

After all, these corporate officers are privy to their companies’ inner workings. So, when an insider is seen picking up shares of the company they work for, especially in bulk, it sends a clear signal that they believe the timing is right for loading up.

And when insiders buy dividend stocks, it’s a bright neon sign. Everyone loves a passive income, and the high-yield divs definitely deliver. Investors can sit back and collect the dividends, ensuring a return regardless of the market’s volatility.

Against this backdrop, our attention turns to two specific stocks. These names not only offer dividend yields of up to 7.5%, but they have also recently witnessed insider purchases totaling six figures or more. Adding to their appeal, both stocks carry a unanimous “Buy” rating based on analyst consensus. Let’s take a closer look.

Enterprise Products Partners (EPD)

Up first is Enterprise Products Partners, a major player in North America’s hydrocarbon industry midstream sector. EPD is one of the largest public partnership companies traded on Wall Street; it boasts a market cap of $58 billion. The company’s work is based on a continent-spanning network of assets for the transport of oil, natural gas, and natural gas liquids.

EPD’s network includes over 50,000 miles worth of pipelines, moving hydrocarbon products from the well heads to a series of 25 fractionation facilities and 20 deepwater docks, along with storage assets capable of holding over 260 MMBbls of liquids, both gas and oil derivatives. The company’s ops are centered along with the Gulf of Mexico coast, in Texas and Louisiana, but branch out to the Rocky Mountains, up the Mississippi Valley, northeast to Appalachia, and into the Southeast.

The company’s revenues peaked one year ago, in Q2 of 2022, and have been trending downward since – although the firm does remain profitable. In 2Q23, EPD brought in $10.65 billion at the top line, for a 34% decline year-over-year. More importantly, the revenue missed the forecast significantly, by $1.67 billion. At the bottom line, EPD’s EPS of 57 cents per diluted share was 1 cent below expectations.

In addition to revenues and earnings, EPD’s distributable cash flow also fell year-on-year, from $2 billion in 2Q22 to $1.7 billion for 2Q23. Despite the drop in distributable cash flow, the company raised its Q2 dividend payment to 50 cents per common share from 49 cents for the previous quarter. The new dividend annualizes to $2 and provides a strong yield of 7.5%. The dividend payment went out on August 14.

On the insider front, the latest ‘informative buy’ purchase was made on August 7th by William Montgomery, a member of the company’s Board of Directors. Montgomery spent $1.33 million to acquire 50,000 shares of the company. His total ownership in the company is currently valued at $3.08 million.

Checking in with the analysts, we can find some equally upbeat takes. For analyst Selman Akyol, of Stifel, the story on EPD should spark plenty of investor interest. The company’s ability to leverage increased oil production for increased revenue is a key point for this analyst, as is the firm’s full coverage of its dividend.

“Between healthy crude prices, improved drilling and completion efficiencies, longer laterals and some cost deflation, management is confident in seeing YoY crude oil production growth in the 500 to 700 Mbpd range. We continue to favor the EPD story, given its prospects for growth, industry leading balance sheet and financial flexibility… We believe Enterprise has one of the strongest financial profiles within the midstream sector, and can withstand turbulence from a volatile macro environment,” Akyol opined.

Quantifying his stance, Akyol rates EPD a Buy, and his price target of $35 implies a one-year upside potential of 33%. (To watch Akyol’s track record, click here)

On the larger picture, EPD’s Strong Buy consensus rating is unanimous, based on 8 positive analyst reviews set in recent weeks. The shares are trading for $26.32 and their $32.88 average price target implies that a gain of ~25% is waiting for the stock in the next 12 months. (See EPD stock forecast)

Entravision Communications (EVC)

The second stock on today’s list, Entravision Communications, is based in Santa Monica, California, and is an important media provider in the Spanish-language segment of the US communications markets. Entravision owns TV, radio stations, and outdoor media, focusing its operations on the nation’s largest Hispanic marketplaces. As a media owner, Entravision is major global advertising and ad-tech solutions firm, and partners with such big names as NBC, FOX, and UniMas.

Entravision is a highly diversified communications company. It has a large TV presence, as well as radio, but also works in digital communications and online content, and has a segment-leading collection of Spanish-language media influencers. In addition, Entravision has a premium network of audio streaming providers. While the company’s business is centered in the US and reaches out to almost all of Latin America, Entravision’s communications network also reaches into Europe and Africa, as well as South, East, and Southeast Asia, 41 countries in all.

Revenues and earnings for Entravision have tracked in opposite directions over the past several quarters, with revenues continuing to show year-over-year increases while EPS has been slipping. The last report, for 2Q23, bears this out. Quarterly ad revenue was up to record levels, and powered a 23% y/y increase in net revenue. The top line increased to $273.4 million, beating the forecasts by over $11.2 million. On the bottom line, however, Entravision’s GAAP EPS fell y/y, from a 10 cent profit to a 2 cent net loss; the EPS loss came in 6 cent below estimates.

Even though Entravision ran a net loss, the company’s Board approved payment of a 5-cent dividend to common shareholders, to go out on September 29. With an annualized payment of 20 cents per common share, the EVC dividend gives a yield of 5.22%.

On the insider trades, we find that company CEO Michael Christenson made two separate purchases earlier this month, acquiring a total of 202,170 shares at a cost of $782,098. As a result of these transactions, Christenson’s total holdings in the company are now valued at $4.86 million.

All of this caught the attention of EF Hutton analyst Michael Albanese, who is impressed by Entravision’s proven ability to switch from TV and radio to digital communications. Albanese sums up his view, saying of the company, “Entravision continues to execute on its growth strategy focused around its digital marketing business. It has successfully transitioned from a traditional TV and radio broadcasting business to digital marketing with over 80% of revenues being generated from the space…”

“The digital segment has continued to see cost pressures in the near term, but we expect margins to recover longer-term with an uptick in volume and a focus on finding cost efficiencies between the portfolio. We expect to see some near term strength in 2H23 in traditional linear with expectations of increased political and national ad spending heading into the primaries,” the analyst added.

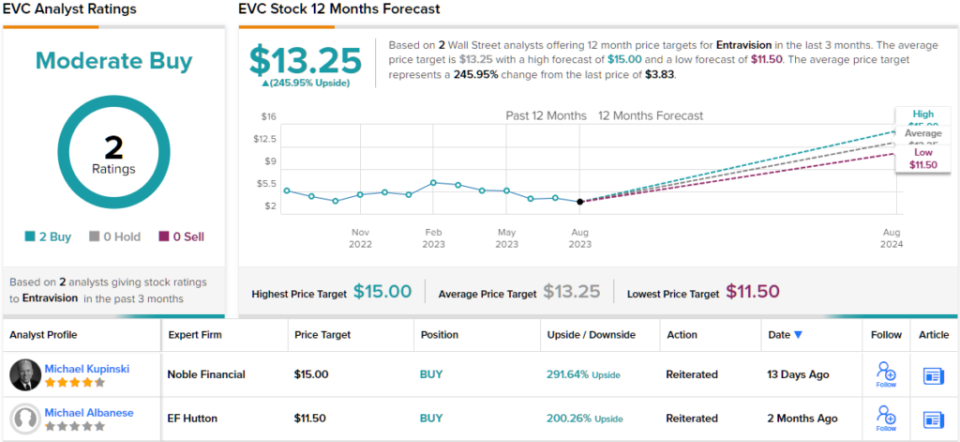

Breaking down his insights into practical advice for investors, Albanese rates EVC shares as a Buy. His price target, of $11.50, suggests the stock will appreciate by an impressive 200% on the one-year horizon. (To watch Albanese’s track record, click here)

While there are only 2 recent analyst reviews on file for Entravision, they both are positive – giving the stock its Moderate Buy consensus rating. The shares are trading for just $3.83 and have an average price target of $13.25, even more bullish than the EF Hutton take, implying a one-year upside of ~246%. (See EVC stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.