Insperity (NSP) Rides on PEO Industry Strength Amid Cost Woes

Insperity, Inc. NSP is currently benefiting from strength in the professional employer organization (“PEO”) services industry and a strong cash position while increasing expenses remain a concern.

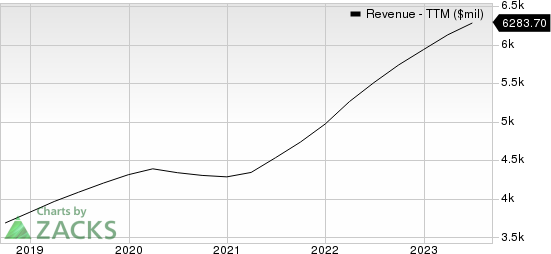

The company recently reported second-quarter 2023 adjusted earnings of 64 cents per share, which missed the Zacks Consensus Estimate by 48.4% and decreased 44.8% year over year. Revenues of $1.59 billion surpassed the consensus mark by 2.6% and increased 10.7% year over year.

Insperity’s top-line growth is directly proportional to the rise in the average number of worksite employees paid per month. In the second quarter, the average number of worksite employees (WSEE) paid per month increased 7% year over year, with revenues per WSEE increasing 3.3%.

Insperity, Inc. Revenue (TTM)

Insperity, Inc. revenue-ttm | Insperity, Inc. Quote

How is NSP Faring?

Insperity looks strong on the back of a growing PEO industry, which is currently being driven by the growth of small and medium-sized businesses, increased costs related to workers’ compensation insurance coverage, workplace safety programs, employee-related complaints and litigation, complex regulation of payroll, payroll tax and employment issues.

Insperity is an integrated human resources and business solutions provider serving multiple verticals and offering a comprehensive suite of HR services solutions through PEO services known as Workforce Optimization and Workforce Synchronization solutions. The company’s diversified revenue base ensures consistent revenue growth while providing a cushion against market risks.

Insperity's current ratio at the end of second-quarter 2023 was pegged at 1.2, higher than the prior quarter’s 1.17 and the prior-year quarter’s 1.13. A current ratio greater than 1 is desirable as it indicates that the risk of default is less.

Zacks Rank and Stocks to Consider

Insperity currently carries a Zacks Rank #3 (Neutral).

Here are some better-ranked stocks from the Business Service sector that investors may consider.

DocuSign DOCU, currently carrying a Zacks Rank #2 (Buy), beat the Zacks Consensus Estimate in all the trailing four quarters, averaging 27.1%. The Zacks Consensus Estimate for fiscal 2024 revenues and earnings indicate growth of 8.1% and 24.1%, respectively. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Automatic Data ADP, currently carrying a Zacks Rank #2, beat the Zacks Consensus Estimate in all the trailing four quarters, with an average of 3.1%. The Zacks Consensus Estimate for fiscal 2023 revenues and earnings indicate growth of 6.3% and 11.1%, respectively.

Broadridge BR, currently carrying a Zacks Rank #2, beat the Zacks Consensus Estimate in two of the trailing four quarters, missing once and matching on the remaining occasion, with an average of 0.5%. The Zacks Consensus Estimate for fiscal 2024 revenues and earnings indicate growth of 7.2% and 8.8%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Broadridge Financial Solutions, Inc. (BR) : Free Stock Analysis Report

Automatic Data Processing, Inc. (ADP) : Free Stock Analysis Report

Insperity, Inc. (NSP) : Free Stock Analysis Report

DocuSign (DOCU) : Free Stock Analysis Report