Interactive Brokers (IBKR) Hurt by Rising Costs, Overseas Risk

Interactive Brokers Group, Inc. IBKR is expected to witness a persistent rise in non-interest expenses. It also generates a larger portion of its revenues from overseas operations, which remains a major concern amid an uncertain macroeconomic backdrop. However, low level of compensation expense, development of proprietary software and steadily increasing emerging market customers are expected to keep aiding its revenues.

Interactive Brokers’ expenses witnessed a compound annual growth rate (CAGR) of 10.4% over the five-year period ended 2022, with the uptrend continuing in the first nine months of 2023. The rise was mainly due to higher execution, clearing and distribution fees. As the company continues to invest in franchises, launch new services and upgrade technology, overall costs are projected to remain elevated. We project the company’s total non-interest expenses to record a CAGR of 10.9% by 2025.

Interactive Brokers is a geographically diversified company with a presence across the globe. The company generates almost 30% of total net revenues from overseas operations. A number of risks stemming from the regulatory and political environment, foreign exchange fluctuations and the performance of local economies are likely to affect its financials. Our estimates indicate international revenues to constitute 30% of total net revenues (GAAP) in 2023.

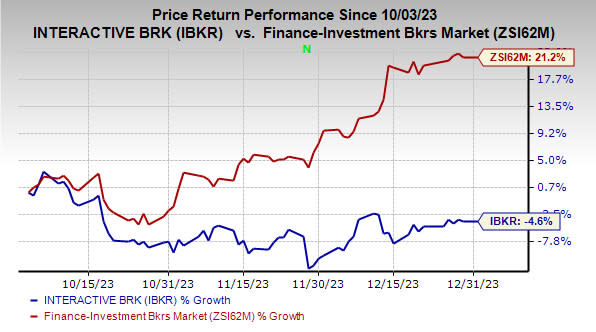

Over the past three months, shares of this Zacks Rank #4 (Sell) company have plunged 4.6% against the industry's rise of 21.2%.

Image Source: Zacks Investment Research

Despite the above-mentioned headwinds, Interactive Brokers is well-placed to grow organically. The company’s total net revenues witnessed a CAGR of 12.5% over the last five years (2017-2022), with momentum persisting in the first three quarters of 2023. Net revenues are expected to improve further in the quarters ahead, given the solid DART numbers. We anticipate total net revenues (GAAP) to witness a CAGR of 13.1% over the three years ended 2025.

The company also has a very low level of compensation expense relative to net revenues (12.2% in the first nine months of 2023), primarily driven by its technological excellence. We project compensation expenses in 2023 to be 12.5% of total net revenues, GAAP.

Stocks to Consider

A couple of better-ranked finance stocks are BrightSphere Investment Group BSIG and Prospect Capital PSEC.

BrightSphere’s current-year earnings estimates have moved 5.1% upward over the past 60 days. The stock has appreciated 3.3% over the past three months. BSIG currently carries a Zacks Rank #2 (Buy).

Prospect Capital’s current-year earnings estimates have moved up 8.1% over the past 60 days. The company’s shares have gained 1.3% over the past three months. At present, PSEC sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Interactive Brokers Group, Inc. (IBKR) : Free Stock Analysis Report

Prospect Capital Corporation (PSEC) : Free Stock Analysis Report

BrightSphere Investment Group Inc. (BSIG) : Free Stock Analysis Report