Investing in Ultra Clean Holdings (NASDAQ:UCTT) five years ago would have delivered you a 283% gain

The worst result, after buying shares in a company (assuming no leverage), would be if you lose all the money you put in. But when you pick a company that is really flourishing, you can make more than 100%. Long term Ultra Clean Holdings, Inc. (NASDAQ:UCTT) shareholders would be well aware of this, since the stock is up 283% in five years. Also pleasing for shareholders was the 57% gain in the last three months.

So let's assess the underlying fundamentals over the last 5 years and see if they've moved in lock-step with shareholder returns.

See our latest analysis for Ultra Clean Holdings

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

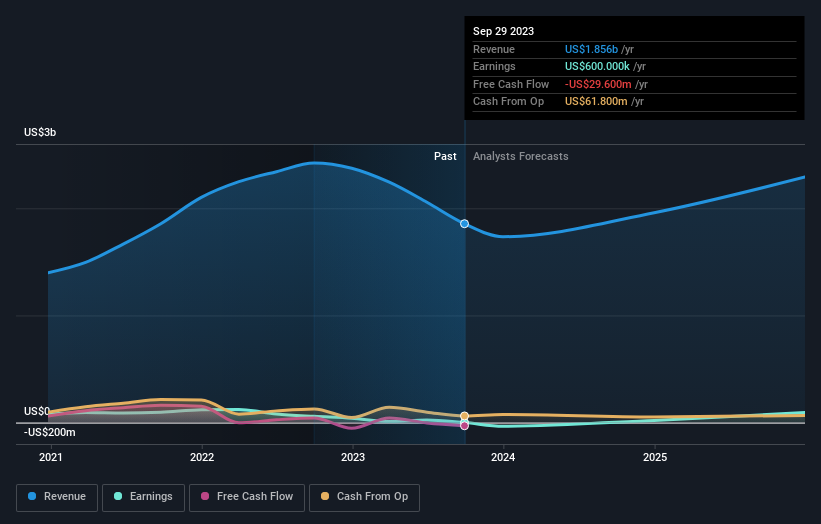

During five years of share price growth, Ultra Clean Holdings actually saw its EPS drop 61% per year. This was, in part, due to extraordinary items impacting earning in the last twelve months.

Essentially, it doesn't seem likely that investors are focused on EPS. Because earnings per share don't seem to match up with the share price, we'll take a look at other metrics instead.

In contrast revenue growth of 19% per year is probably viewed as evidence that Ultra Clean Holdings is growing, a real positive. It's quite possible that management are prioritizing revenue growth over EPS growth at the moment.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

This free interactive report on Ultra Clean Holdings' balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Ultra Clean Holdings' TSR for the year was broadly in line with the market average, at 24%. It has to be noted that the recent return falls short of the 31% shareholders have gained each year, over half a decade. Although the share price growth has slowed, the longer term story points to a business well worth watching. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Take risks, for example - Ultra Clean Holdings has 1 warning sign we think you should be aware of.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.