Investors Love Altria's 10%-Yielding Dividend: Is There Hope for More in 2024?

Tobacco stocks are a controversial niche in the investing community. But regardless of your stance toward them, cigarette makers are famous for paying huge dividends. Altria Group (NYSE: MO) has raised its payouts 58 times over the past 54 years, and it yields a whopping 10% at its current share price.

Dividends aren't everything, though. That share price is down nearly 50% from its high in 2017. Could investors finally get something positive out of Altria in 2024 besides its dividend? For that to happen, it would have to overcome some fundamental challenges.

The golden goose is getting old

Most articles you read about Altria -- or any tobacco stock -- will emphasize next-generation nicotine products like oral pouches or electronic cigarettes. These are certainly important (and increasingly so), but the long-established cigarette business is still what pays for the dividends Altria distributes to shareholders every few months.

Through the first nine months of 2023, smokeable products (mainly cigarettes) accounted for $16.5 billion of Altria's $18.5 billion in total revenue, about 89%. The company also gets about 86% of its operating profits from smokeable products. It's clear that Altria still very much depends on its cigarette business.

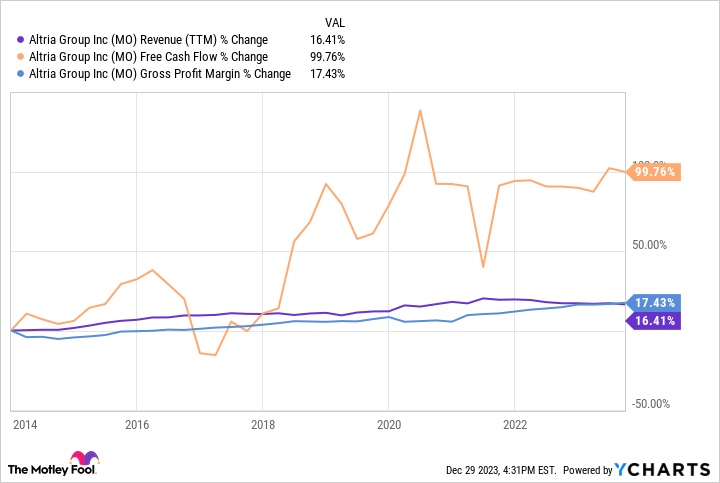

As most people know, smoking is terrible for your health, and the number of Americans who smoke declines nearly every year. Altria's cigarette sales volume is down 10.5% year-over-year through nine months of 2023. For years, Altria has offset selling fewer cigarettes by raising its prices. That's why its free cash flow and gross margin have grown more than its revenue over the past decade.

But it naturally gets harder to make up that difference on an increasingly smaller number of units. This wouldn't be as big a deal if Altria was also growing new businesses. But it has tried that and failed. It spent $12.8 billion buying a stake in Juul, an investment that blew up in Altria's face and lost $12.5 billion of its value after regulators cracked down on Juul's unethical marketing practices.

Altria's growth outlook has dimmed

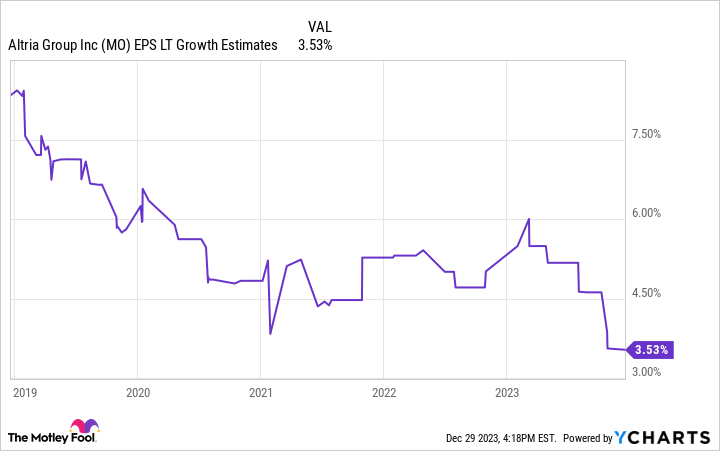

The absence of fresh growth catalysts has slowly worn down analysts' outlooks for Altria. Expected annual earnings growth has drifted from high-single-digit percentages to low-single-digit percentages over the past eight years.

It's important to note that profits are expected to grow more slowly. But investors concerned about Altria's dividend can relax. The dividend payout ratio is manageable at roughly 80%, and earnings growth should help management keep small dividend increases coming.

But Altria's lack of non-cigarette progress has weighed on the stock. The company is building up sales of some next-generation products like On! nicotine pouches. It bought a competitor to take over its electronic cigarette product. But Altria has arguably dragged its feet for years, as is evidenced by its still-alarming degree of reliance on cigarettes.

Is Altria a buy for 2024?

Without a game-changing new source of revenues, it's hard to see much upside in Altria stock in 2024. Even trading at a forward price-to-earnings (P/E) ratio of just 8, its valuation isn't great; note that its price/earnings-to-growth (PEG) ratio is over 2. (A stock with a PEG ratio of 1 is viewed as fairly valued, while a ratio below 1 indicates a bargain.) Slowing growth has offset its falling valuation. The cigarette business still carries almost all of Altria's water, and that won't change overnight.

Of course, there is potential for a game-changer. Altria owns 10% of beer giant Anheuser-Busch InBev. Should the company cash out that stake, which is currently worth $12.8 billion, it would free up enough money for management to do something dramatic like make an acquisition. But even then, shareholders would have to hope it turns out better than the Juul investment did.

Altria is a rock-solid dividend stock. Admittedly, the stock's valuation has fallen by enough that shares should have a higher floor than years ago, even if there isn't a ton of upside ahead for it unless there are notable changes in the business. Don't be shy about collecting that hefty dividend, but those more interested in total investment returns should probably steer clear.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now... and Altria Group wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 18, 2023

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Investors Love Altria's 10%-Yielding Dividend: Is There Hope for More in 2024? was originally published by The Motley Fool