Investors Title Company's (NASDAQ:ITIC) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

With its stock down 3.9% over the past week, it is easy to disregard Investors Title (NASDAQ:ITIC). But if you pay close attention, you might find that its key financial indicators look quite decent, which could mean that the stock could potentially rise in the long-term given how markets usually reward more resilient long-term fundamentals. Particularly, we will be paying attention to Investors Title's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Investors Title

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Investors Title is:

9.3% = US$23m ÷ US$253m (Based on the trailing twelve months to September 2023).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.09 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Investors Title's Earnings Growth And 9.3% ROE

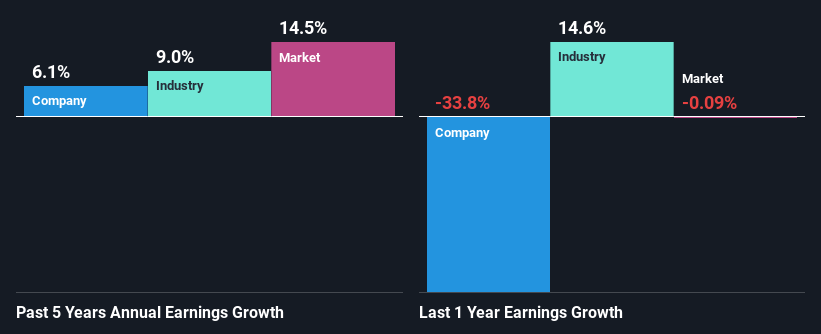

When you first look at it, Investors Title's ROE doesn't look that attractive. A quick further study shows that the company's ROE doesn't compare favorably to the industry average of 14% either. However, the moderate 6.1% net income growth seen by Investors Title over the past five years is definitely a positive. So, the growth in the company's earnings could probably have been caused by other variables. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Investors Title's reported growth was lower than the industry growth of 9.0% over the last few years, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Investors Title's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Investors Title Making Efficient Use Of Its Profits?

Investors Title's three-year median payout ratio to shareholders is 8.4% (implying that it retains 92% of its income), which is on the lower side, so it seems like the management is reinvesting profits heavily to grow its business.

Besides, Investors Title has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Conclusion

Overall, we feel that Investors Title certainly does have some positive factors to consider. That is, a decent growth in earnings backed by a high rate of reinvestment. However, we do feel that that earnings growth could have been higher if the business were to improve on the low ROE rate. Especially given how the company is reinvesting a huge chunk of its profits. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. Our risks dashboard will have the 1 risk we have identified for Investors Title.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.