IRIDEX Corporation's (NASDAQ:IRIX) Price Is Right But Growth Is Lacking

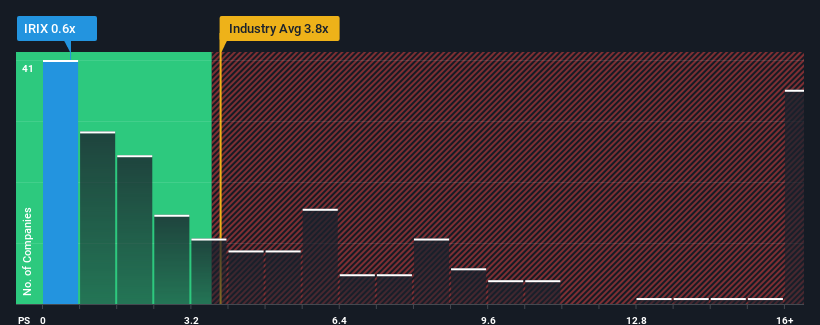

You may think that with a price-to-sales (or "P/S") ratio of 0.6x IRIDEX Corporation (NASDAQ:IRIX) is definitely a stock worth checking out, seeing as almost half of all the Medical Equipment companies in the United States have P/S ratios greater than 3.8x and even P/S above 9x aren't out of the ordinary. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for IRIDEX

What Does IRIDEX's Recent Performance Look Like?

IRIDEX could be doing better as it's been growing revenue less than most other companies lately. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on IRIDEX.

Is There Any Revenue Growth Forecasted For IRIDEX?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like IRIDEX's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 3.6%. The latest three year period has also seen an excellent 37% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 2.5% during the coming year according to the dual analysts following the company. That's shaping up to be materially lower than the 8.4% growth forecast for the broader industry.

In light of this, it's understandable that IRIDEX's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On IRIDEX's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that IRIDEX maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

And what about other risks? Every company has them, and we've spotted 3 warning signs for IRIDEX (of which 1 doesn't sit too well with us!) you should know about.

If you're unsure about the strength of IRIDEX's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here