The J.M. Smucker (SJM) Benefits From Pricing, Core Priorities

The J. M. Smucker Company SJM has been benefiting from its strong pricing endeavors amid cost-related headwinds. A focus on core categories has also been working well for this Zacks Rank #3 (Hold) company.

These upsides aided The J. M. Smucker’s fourth-quarter fiscal 2023 results, wherein the top and bottom lines increased year over year and beat the Zacks Consensus Estimate. Results reflected strength in strategies and the demand for the company’s brands. Management remains focused on sustaining momentum due to its key growth platforms — Uncrustables sandwiches, coffee portfolio (including expansion into new formats), and dog treats and cat food.

Let’s delve deeper.

Robust Q4, Encouraging View

In the fourth quarter, adjusted earnings of $2.64 per share jumped 18% year over year and surpassed the Zacks Consensus Estimate of $2.42. Net sales amounted to $2,234.8 million, which advanced 10% year over year and came ahead of the Zacks Consensus Estimate of $2,183 million.

Excluding non-comparable net sales related to divestitures and currency movements, net sales grew 11%. The uptick in comparable net sales can be attributed to the positive net price realization, mainly reflecting list price increases for the U.S. Retail, and International and Away from Home segments.

For fiscal 2024, management anticipates comparable net sales to rise 8.5-9.5%. This implies the positive impact of elevated net pricing and a favorable volume/mix. Volume growth is expected across all four segments.

The adjusted EPS for fiscal 2024 is envisioned in the $9.20-$9.60 band, suggesting growth from $8.92 recorded in fiscal 2023. The bottom-line growth reflects expected comparable sales growth, enhanced profit margins, gains from the company’s Transformation Office and the impact of recent share buybacks.

Image Source: Zacks Investment Research

Pricing – a Key Driver

The J. M. Smucker has been benefiting from positive net price realization, which was also witnessed in the fourth quarter of fiscal 2023, with higher net price realization contributing 11 percentage points to comparable sales growth.

In the U.S. Retail Pet Foods segment, net price realization had a favorable 12-percentage point impact on net sales. In the U.S. Retail Coffee, net price realization boosted net sales by 10 percentage points. The net price realization had a 12% positive impact on sales in the U.S. Retail Consumer Foods. In the International and Away from Home unit, net price realization had a positive impact of 13% on net sales.

Focus on Core Priorities

The J. M. Smucker is progressing well with core priorities, which include driving commercial excellence, reshaping the portfolio, streamlining the cost structure and unleashing its organization to win. Strength in such strategies is helping SJM navigate complex supply-chain challenges and improve in-store fundamentals and stock performance for the brands. The company is committed to increasing its focus and resources to reshape the portfolio to achieve sustainable growth across pet food and pet snacks, coffee and snacking categories.

The J. M. Smucker concluded the divestiture of certain pet food brands in the fourth quarter of fiscal 2023 to reshape the portfolio. This brings the pet business structure to include 60% pet snacks and 40% cat food. This move, which will help SJM direct more resources toward the fast-growing and higher-margin dog snacks category, is expected to enhance the product mix and profit over time.

The company anticipates increasing its dog snacks portfolio to $1 billion (in annual net sales) in the next few years. Apart from this, management has been optimizing its supply chain, lowering discretionary costs and expanding network production efficiencies.

Cost Woes to be Countered?

The J. M. Smucker has been dealing with rising costs. Though the gross margin increased year over year in the fourth quarter of fiscal 2023, the company continued to witness higher commodity and ingredient, manufacturing and packaging expenses. In its fourth-quarter earnings release, management stated that the ongoing cost inflation, supply-chain bottlenecks and the broader macroeconomic landscape continue to affect the company’s results and cause risks for fiscal 2024.

The J. M. Smucker’s selling, distribution and administrative (SD&A) costs in the fourth quarter rose to $376 million from $352.6 million reported during the corresponding period last year. The increase resulted from elevated incentive compensations.

Further, management’s bottom-line view for fiscal 2024 assumes elevated SD&A expenses. This includes pre-production costs associated with Uncrustables capacity expansion, elevated marketing expenditures and increased investments in liquid coffee.

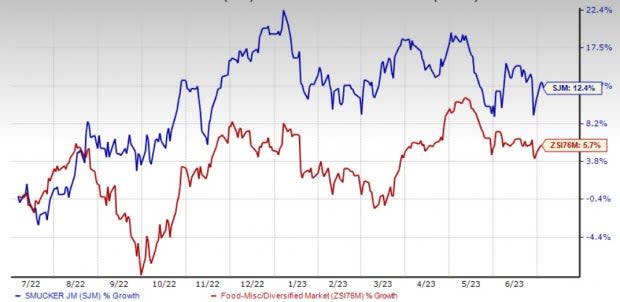

However, the aforementioned upsides are likely to help the company tide over cost woes and spur growth. Shares of SJM have rallied 12.4% in the past year compared with the industry’s growth of 5.7%.

Solid Staple Stocks

Some better-ranked consumer staple stocks are Nomad Foods NOMD, Celsius Holdings CELH and Lamb Weston LW.

Nomad Foods, a frozen food product company, currently sports a Zacks Rank #1 (Strong Buy). NOMD has a trailing four-quarter earnings surprise of 8.5%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nomad Foods’ current fiscal-year sales suggests growth of around 8% from the year-ago reported figures.

Celsius Holdings, which offers functional drinks and liquid supplements, currently sports a Zacks Rank #1. CELH delivered an earnings surprise of 81.8% in the last reported quarter.

The Zacks Consensus Estimate for Celsius Holdings’ current fiscal-year sales and earnings suggests growth of 69.6% and 154.4%, respectively, from the year-ago reported numbers.

Lamb Weston, which is a frozen potato product company, currently carries a Zacks Rank #2 (Buy). LW has a trailing four-quarter earnings surprise of 47.6%, on average.

The Zacks Consensus Estimate for Lamb Weston’s current fiscal-year sales and earnings suggests growth of 30% and 117.3%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The J. M. Smucker Company (SJM) : Free Stock Analysis Report

Lamb Weston (LW) : Free Stock Analysis Report

Nomad Foods Limited (NOMD) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report