Are Jewett-Cameron Trading Company Ltd.'s (NASDAQ:JCTC.F) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

Jewett-Cameron Trading (NASDAQ:JCTC.F) has had a rough three months with its share price down 28%. However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Jewett-Cameron Trading's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Jewett-Cameron Trading

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Jewett-Cameron Trading is:

11% = US$2.6m ÷ US$23m (Based on the trailing twelve months to November 2021).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.11 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Jewett-Cameron Trading's Earnings Growth And 11% ROE

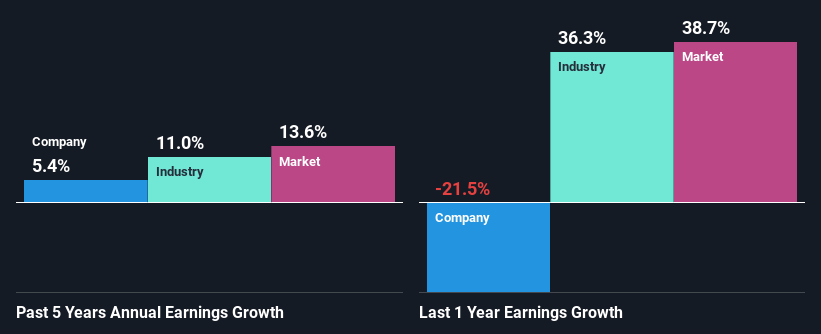

To begin with, Jewett-Cameron Trading seems to have a respectable ROE. Yet, the fact that the company's ROE is lower than the industry average of 21% does temper our expectations. However, the moderate 5.4% net income growth seen by Jewett-Cameron Trading over the past five years is definitely a positive. We reckon that there could be other factors at play here. Such as - high earnings retention or an efficient management in place. Bear in mind, the company does have a respectable level of ROE. It is just that the industry ROE is higher. So this also provides some context to the earnings growth seen by the company.

As a next step, we compared Jewett-Cameron Trading's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 11% in the same period.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Jewett-Cameron Trading's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Jewett-Cameron Trading Using Its Retained Earnings Effectively?

Jewett-Cameron Trading doesn't pay any dividend, meaning that all of its profits are being reinvested in the business, which explains the fair bit of earnings growth the company has seen.

Summary

Overall, we feel that Jewett-Cameron Trading certainly does have some positive factors to consider. Specifically, we like that the company is reinvesting a huge chunk of its profits at a respectable rate of return. This of course has caused the company to see a good amount of growth in its earnings. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. Our risks dashboard would have the 4 risks we have identified for Jewett-Cameron Trading.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.