Journey Energy's (TSE:JOY) investors will be pleased with their enviable 991% return over the last three years

The last three months have been tough on Journey Energy Inc. (TSE:JOY) shareholders, who have seen the share price decline a rather worrying 31%. But over the last three years the stock has shone bright like a diamond. Indeed, the share price is up a whopping 991% in that time. As long term investors the recent fall doesn't detract all that much from the longer term story. The share price action could signify that the business itself is dramatically improved, in that time. We love happy stories like this one. The company should be really proud of that performance!

So let's assess the underlying fundamentals over the last 3 years and see if they've moved in lock-step with shareholder returns.

Check out our latest analysis for Journey Energy

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

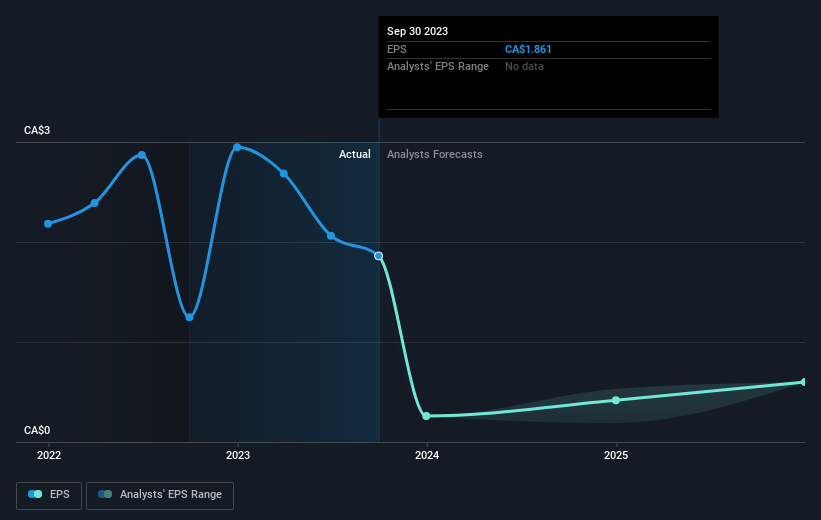

Journey Energy became profitable within the last three years. Given the importance of this milestone, it's not overly surprising that the share price has increased strongly.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

We know that Journey Energy has improved its bottom line over the last three years, but what does the future have in store? Take a more thorough look at Journey Energy's financial health with this free report on its balance sheet.

A Different Perspective

Journey Energy shareholders are down 30% for the year, but the market itself is up 4.1%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. On the bright side, long term shareholders have made money, with a gain of 14% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 3 warning signs for Journey Energy you should be aware of, and 2 of them don't sit too well with us.

But note: Journey Energy may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Canadian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.