Is JOYY Inc (YY) Modestly Overvalued? A Comprehensive Valuation Analysis

On September 27, 2023, JOYY Inc (NASDAQ:YY) experienced a daily loss of -3.06%, contrasting its 3-month gain of 26.97%. With an Earnings Per Share (EPS) of 3.27, the question arises: is the stock modestly overvalued? This article provides a detailed valuation analysis of JOYY (NASDAQ:YY), offering insights into its intrinsic value and market performance. Read on for a comprehensive understanding of the company's value.

Company Overview

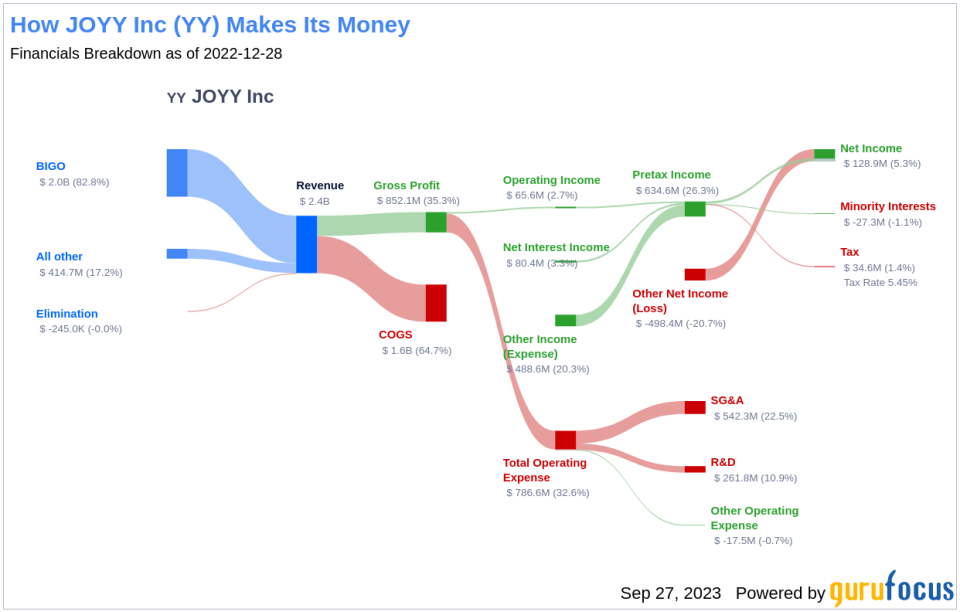

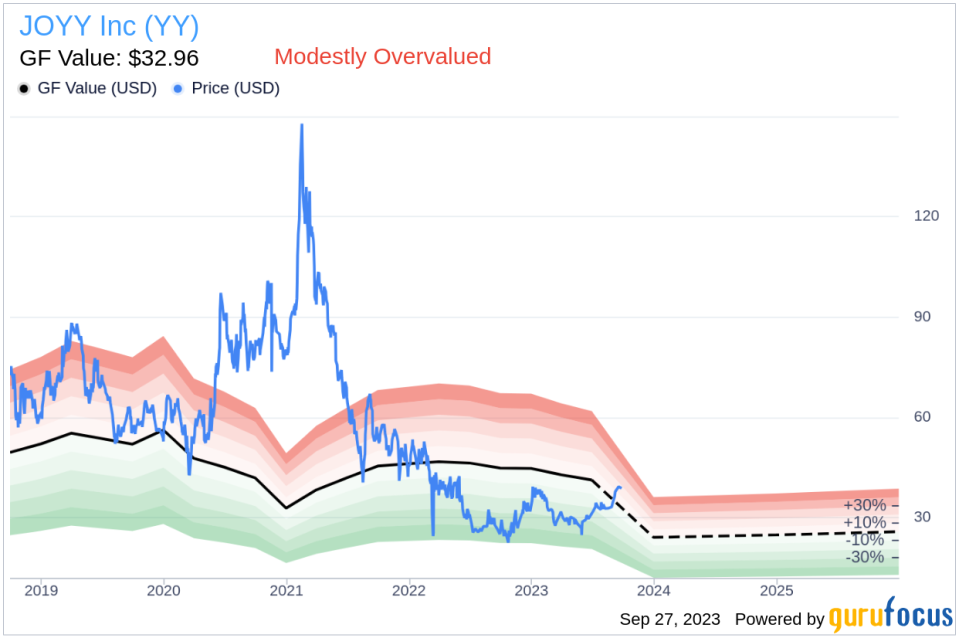

JOYY Inc is a prominent player in the social media platform industry, specializing in creating and sharing entertainment content and activities. Its interactive online live media offerings provide users with an immersive entertainment experience. With products like Bigo Live, Likee, and Hago, JOYY Inc has established a strong presence in China, developed countries, the Middle East, and Southeast Asia. As of the date of this analysis, JOYY (NASDAQ:YY) is trading at $38.7 per share, with a market cap of $2.40 billion, suggesting a modest overvaluation compared to its GF Value of $32.96.

Understanding the GF Value

The GF Value represents the intrinsic value of a stock, derived from a proprietary method. It considers historical trading multiples, a GuruFocus adjustment factor based on past returns and growth, and future business performance estimates. The GF Value Line provides an overview of the fair value at which the stock should ideally trade. If the stock price is significantly above the GF Value Line, it indicates overvaluation and a likely poor future return. Conversely, if the price is significantly below the GF Value Line, higher future returns can be anticipated.

Based on the GF Value, JOYY (NASDAQ:YY) is considered modestly overvalued. This suggests that the long-term return of its stock is likely to be lower than its business growth.

Link: These companies may deliever higher future returns at reduced risk.

Assessing JOYY's Financial Strength

Before investing in a stock, it's crucial to evaluate the company's financial strength. Companies with poor financial strength pose a higher risk of permanent loss. JOYY's cash-to-debt ratio of 6.95 ranks better than 50.26% of companies in the Interactive Media industry, indicating fair financial strength.

Profitability and Growth

Investing in profitable companies, especially those with consistent long-term profitability, is typically less risky. JOYY has been profitable for 9 out of the past 10 years, with an operating margin of 1.4%, which ranks worse than 51.97% of companies in the Interactive Media industry. However, JOYY's profitability is ranked 8 out of 10, indicating strong profitability.

Growth is a vital factor in company valuation. JOYY's 3-year average revenue growth rate ranks better than 83.07% of companies in the Interactive Media industry, and its 3-year average EBITDA growth rate is 99.2%, ranking better than 96.37% of companies in the industry. This suggests a strong growth trajectory for JOYY.

ROIC vs WACC

Comparing a company's return on invested capital (ROIC) to its weighted average cost of capital (WACC) can provide insights into its profitability. JOYY's ROIC of 0.59 is lower than its WACC of 4.63, suggesting that the company may not be creating value for its shareholders.

Conclusion

In conclusion, JOYY Inc (NASDAQ:YY) is believed to be modestly overvalued. Despite its fair financial condition and strong profitability, its current market price exceeds its intrinsic value. However, its growth ranks better than 96.37% of companies in the Interactive Media industry, indicating potential future growth. For a more detailed financial overview of JOYY, check out its 30-Year Financials here.

To discover high-quality companies that may deliver above-average returns, explore the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.