Kimberly-Clark (NYSE:KMB) Reports Q4 In Line With Expectations

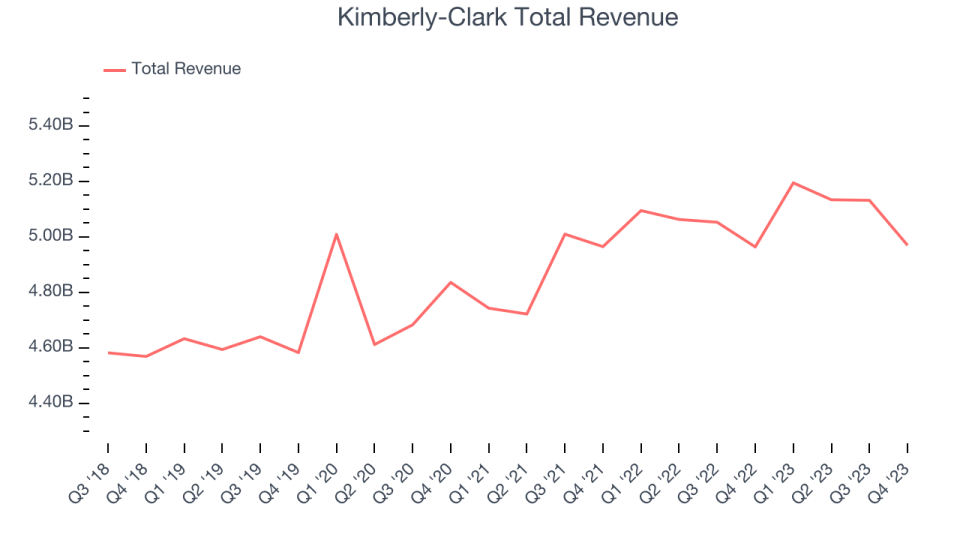

Household products company Kimberly-Clark (NYSE:KMB) reported results in line with analysts' expectations in Q4 FY2023, with revenue flat year on year at $4.97 billion. It made a non-GAAP profit of $1.51 per share, down from its profit of $1.54 per share in the same quarter last year.

Is now the time to buy Kimberly-Clark? Find out by accessing our full research report, it's free.

Kimberly-Clark (KMB) Q4 FY2023 Highlights:

Market Capitalization: $42.23 billion

Revenue: $4.97 billion vs analyst estimates of $4.99 billion (small miss)

EPS (non-GAAP): $1.51 vs analyst expectations of $1.54 (2.1% miss)

Free Cash Flow of $998 million, up 30.1% from the previous quarter

Gross Margin (GAAP): 34.9%, up from 32.8% in the same quarter last year

Organic Revenue was up 3% year on year

"We had a solid finish to 2023, delivering strong organic growth as well as cost and earnings recovery above our initial expectations," said Kimberly-Clark Chairman and CEO Mike Hsu.

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NYSE:KMB) is now a household products powerhouse known for personal care and tissue products.

Household Products

Household products companies engage in the manufacturing, distribution, and sale of goods that maintain and enhance the home environment. This includes cleaning supplies, home improvement tools, kitchenware, small appliances, and home decor items. Companies within this sector must focus on product quality, innovation, and cost efficiency to remain competitive. Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options.

Sales Growth

Kimberly-Clark is one of the most widely recognized consumer staples companies in the world. Its influence over consumers gives it extremely high negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don't have).

As you can see below, the company's annualized revenue growth rate of 2.2% over the last three years was weak as consumers bought less of its products. We'll explore what this means in the "Volume Growth" section.

This quarter, Kimberly-Clark's revenue grew 0.1% year on year to $4.97 billion, falling short of Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Volume Growth

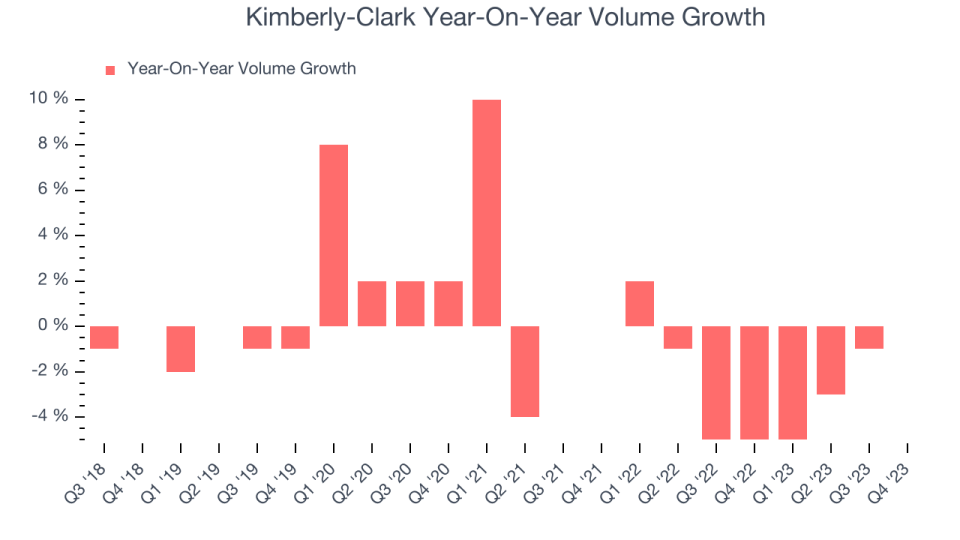

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Kimberly-Clark generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Kimberly-Clark's average quarterly sales volumes have shrunk by 2.3%. This decrease isn't ideal as the quantity demanded for consumer staples products is typically stable. Luckily, Kimberly-Clark was able to offset fewer customers purchasing its products by charging higher prices, enabling it to generate 6.1% average organic revenue growth. We hope the company can grow its volumes soon, however, as consistent price increases (on top of inflation) aren't sustainable over the long term unless the business is really really special.

In Kimberly-Clark's Q4 2023, year on year sales volumes were flat. This result was a well-appreciated turnaround from the 5% year-on-year decline it posted 12 months ago, showing the company is heading in the right direction.

Key Takeaways from Kimberly-Clark's Q4 Results

It was good to see Kimberly-Clark increase its gross margin and free cash flow, which both beat analysts' estimates. On the other hand, the company's operating margin and EPS fell short due to $170 million of currency headwinds from its developing markets experiencing hyperinflation. For organic revenue growth, its Personal Care segment carried the weight, contributing 6% growth compared to 0% and negative 1% for Consumer Tissue and Professional. In 2024, the company expects to generate low-to-mid single-digit organic revenue growth while continuing to face currency headwinds that will impact its operating margin and EPS. Overall, this was a mediocre quarter for Kimberly-Clark. The company is down 1.8% on the results and currently trades at $122.72 per share.

Kimberly-Clark may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.