Kimberly-Clark's (KMB) Focus on Core Strategies Fuels Growth

Kimberly-Clark Corporation KMB is firmly committed to three strategic growth pillars, which include strengthening its core business in the developed markets, accelerating growth of its Personal Care segment in the developing and emerging markets, and enhancing its digital and e-commerce capabilities.

With its extensive portfolio, encompassing value and premium options, the company can meet consumers’ specific needs.

Kimberly Clark is actively driving innovation and propagating technological advancements across its product range to guarantee the delivery of an exceptional value proposition to its customers. KMB is strategically positioned with brands such as Scott and Huggies Snug & Dry to cater to the value-conscious consumer. Expanding its market presence remains a key objective.

KMB is bolstering its pricing strategy across different markets, including improving large-count packages and big-box retail channels, and making entry-level prices more accessible through small-format channels.

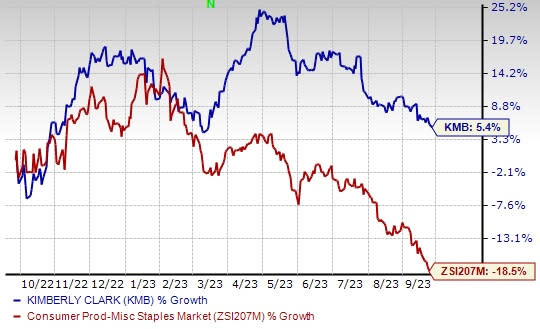

Image Source: Zacks Investment Research

The company's concentration on key commercial sectors, its effective engagement in the digital realm and its commitment to innovation are all contributing to the strong performance of the K-C Professional segment. Segmental sales advanced 11% to $887 million and boasted 13% organic growth in the second quarter of 2023. Growth was observed across all regions.

KMB has been proactively increasing investments in specific capabilities, demonstrating an ongoing dedication to enhancing revenue growth management and advancing the digital agenda. This includes upgrades to select systems like the migration to S4 HANA and the strategic development of various other capabilities throughout the organization over a multi-year period.

FORCE Program Bodes Well

Kimberly-Clark is dedicated to cost reduction and improving supply-chain efficiency through its FORCE Program. This program has consistently delivered substantial cost savings and improved the overall performance. In the second quarter of 2023, the company successfully realized savings of $80 million through the FORCE program.

Additionally, the company is actively implementing revenue management strategies to address the challenges posed by cost inflation, indicating a comprehensive approach to managing its financial performance.

Wrapping Up

On its last reported quarter’s earnings call, management raised the 2023 earnings per share (EPS) and operating profit outlook. The company envisions 2023 adjusted EPS to increase 10-14% from the adjusted EPS reported in 2022. Earlier, it was anticipated to rise 6-10%. (Read more: Kimberly-Clark Ups View on Q2 Earnings & Sales Beat)

Management expects the operating margin to grow 150 basis points (bps) compared with an increase of 130 bps stated earlier. It anticipates 2023 net sales between flat and 2% growth, whereas organic sales are projected to increase 3-5%. Earlier, organic sales were anticipated to rise 2-4%.

Shares of this Zacks Rank #2 (Buy) company have risen 5.4% in the past year against the industry’s decline of 18.5%.

3 Other Picks You Can’t Miss Out On

We have highlighted three other top-ranked stocks, namely Ollie's Bargain Outlet Holdings, Inc. OLLI, Ross Stores Inc. ROST and Walmart Inc. WMT.

Ollie's Bargain Outlet is a value retailer of brand-name merchandise at drastically reduced prices. The company currently has a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Ollie's Bargain Outlet’s current fiscal-year sales and EPS suggests growth of 19.6% and 67.3%, respectively, from the year-ago reported figures. OLLI has a trailing four-quarter earnings surprise of 1.3%, on average.

Ross Stores is an off-price retailer of apparel and home accessories. The company currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Ross Stores’ current fiscal-year sales and EPS suggests growth of 8.1% and 19.4%, respectively, from the year-ago reported figures. ROST has a trailing four-quarter earnings surprise of 11.4%, on average.

Walmart, which operates a chain of hypermarkets, discount department stores and grocery stores, currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Walmart’s current fiscal-year sales and earnings suggests growth of 9.2% and 2.2%, respectively, from the year-ago reported numbers. WMT has a trailing four-quarter earnings surprise of 11.6%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT) : Free Stock Analysis Report

Kimberly-Clark Corporation (KMB) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Ollie's Bargain Outlet Holdings, Inc. (OLLI) : Free Stock Analysis Report