Kin and Carta plc's (LON:KCT) Price Is Right But Growth Is Lacking

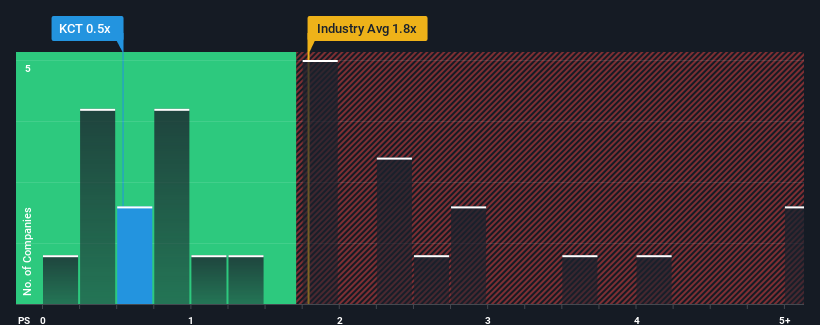

Kin and Carta plc's (LON:KCT) price-to-sales (or "P/S") ratio of 0.5x may look like a pretty appealing investment opportunity when you consider close to half the companies in the IT industry in the United Kingdom have P/S ratios greater than 1.8x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Kin and Carta

What Does Kin and Carta's P/S Mean For Shareholders?

Kin and Carta's revenue growth of late has been pretty similar to most other companies. One possibility is that the P/S ratio is low because investors think this modest revenue performance may begin to slide. Those who are bullish on Kin and Carta will be hoping that this isn't the case.

Keen to find out how analysts think Kin and Carta's future stacks up against the industry? In that case, our free report is a great place to start.

How Is Kin and Carta's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Kin and Carta's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 26%. The strong recent performance means it was also able to grow revenue by 51% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 1.2% as estimated by the three analysts watching the company. Meanwhile, the broader industry is forecast to expand by 12%, which paints a poor picture.

With this information, we are not surprised that Kin and Carta is trading at a P/S lower than the industry. However, shrinking revenues are unlikely to lead to a stable P/S over the longer term. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Bottom Line On Kin and Carta's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It's clear to see that Kin and Carta maintains its low P/S on the weakness of its forecast for sliding revenue, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 1 warning sign for Kin and Carta that you should be aware of.

If these risks are making you reconsider your opinion on Kin and Carta, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here