Knight-Swift (KNX) Lags Q2 Earnings, Posts Dull '23 EPS View

Knight-Swift Transportation Holdings KNX reported disappointing second-quarter 2023 results, wherein both earnings and revenues lagged the Zacks Consensus Estimate.

Quarterly earnings (excluding 10 cents from non-recurring items) of 49 cents per share missed the Zacks Consensus Estimate of 55 cents and tumbled 65.3% year over year.

Total revenues of $1,553 million also underperformed the Zacks Consensus Estimate of $1,591 million. The top line plunged 20.8% year over year.

Total operating expenses (on a reported basis) decreased 10.8% year over year to $1.46 billion. We had expected the metric to decline 11.6% in the reported quarter from second-quarter 2022 actuals.

Knight-Swift’s adjusted operating income fell 66.3% year over year.

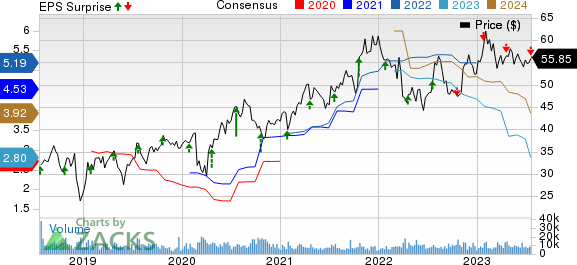

Knight-Swift Transportation Holdings Inc. Price, Consensus and EPS Surprise

Knight-Swift Transportation Holdings Inc. price-consensus-eps-surprise-chart | Knight-Swift Transportation Holdings Inc. Quote

Segmental Results

Revenues (excluding fuel surcharge and inter-segment transactions) from Truckload totaled $829.4 million, down 15.5% year over year. The actual percentage decline was steeper than our expectation of an 8.1% year-over-year fall.

Results were hurt by a 14.5% decrease in average revenue per tractor as well as a 3.3% decline in miles per tractor. Adjusted segmental operating income plunged 67% to $68.2 million. Adjusted operating ratio (operating expenses as a percentage of revenues) grew 1290 basis points (bps) to 91.8%.

The Less-Than-Truckload segment generated revenues (excluding fuel surcharges) worth $228.6 million in the June quarter, up 2% year over year. Adjusted segmental operating income dipped 28.5% to $34.2 million. Adjusted operating ratio surged 640 bps to 85.1%.

Revenues from Logistics (excluding inter-segment transactions) amounted to $117.8 million, down 52.4% year over year, owing to a 26.8% decrease in revenue per load. We had expected segmental revenues to plunge 45.5% year over year. Adjusted operating income decreased 77.5% to $9.9 million. The adjusted operating ratio rose 940 bps to 91.6%.

Intermodal revenues (excluding inter-segment transactions) totaled $104.3 million, down 21.5% year over year. We had expected segmental revenues to sink 30.8% year over year. The operating ratio (on a reported basis) soared to 106.4% from 89.3% in the year-ago quarter.

Liquidity

Knight-Swift exited the second quarter with cash and cash equivalents of $229 million compared with $196.7 million at the end of December 2022. Additionally, long-term debt (excluding current maturities) of $1.26 billion raised from $1.02 billion at December 2022 end.

Updated 2023 Guidance

For the ongoing year, Knight-Swift expects adjusted earnings per share in the range of $2.10-$2.30 (earlier view: $3.35-$3.55). The Zacks Consensus Estimate is currently pegged at $2.80. The updated adjusted earnings per share guidance includes a U.S. Xpress loss of 25-30 cents. The acquisition was completed on Jul 1.

KNX now expects net cash capital expenditures for 2023 in the $700-$750 million band (prior guidance: $640-$690 million), which now includes U.S. Xpress. The tax rate is now expected to be between 25% and 26% (prior view: 25%) for 2023.

Currently, Knight-Swift carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Q2 Performance of Some Other Transportation Companies

J.B. Hunt Transport Services’ JBHT second-quarter 2023 earnings of $1.81 per share missed the Zacks Consensus Estimate of $1.97 and declined 25.2% year over year. Total operating revenues of $3,132.6 million also missed the Zacks Consensus Estimate of $3,347.5 million. The top line fell 18.4% year over year.

The downfall was due to a decline in revenue per load of 24% in Integrated Capacity Solutions, 13% in Intermodal and 21% in Truckload. A 4% decrease in productivity in Dedicated Capacity Solutions added to the woes. Changes in customer rate, freight mix and lower fuel surcharge revenues resulted in this downtick.

Delta Air Lines’ DAL second-quarter 2023 earnings (excluding 16 cents from non-recurring items) of $2.68 per share comfortably beat the Zacks Consensus Estimate of $2.42. DAL reported earnings of $1.44 a year ago.

Revenues of $15,578 million beat the Zacks Consensus Estimate of $14,991.6 million. Total revenues increased 12.69% on a year-over-year basis driven by higher air-travel demand. The adjusted operating margin was 17.1% compared with 11.7% in the prior-year period.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Delta Air Lines, Inc. (DAL) : Free Stock Analysis Report

J.B. Hunt Transport Services, Inc. (JBHT) : Free Stock Analysis Report

Knight-Swift Transportation Holdings Inc. (KNX) : Free Stock Analysis Report