La-Z-Boy (NYSE:LZB) Misses Q3 Sales Targets

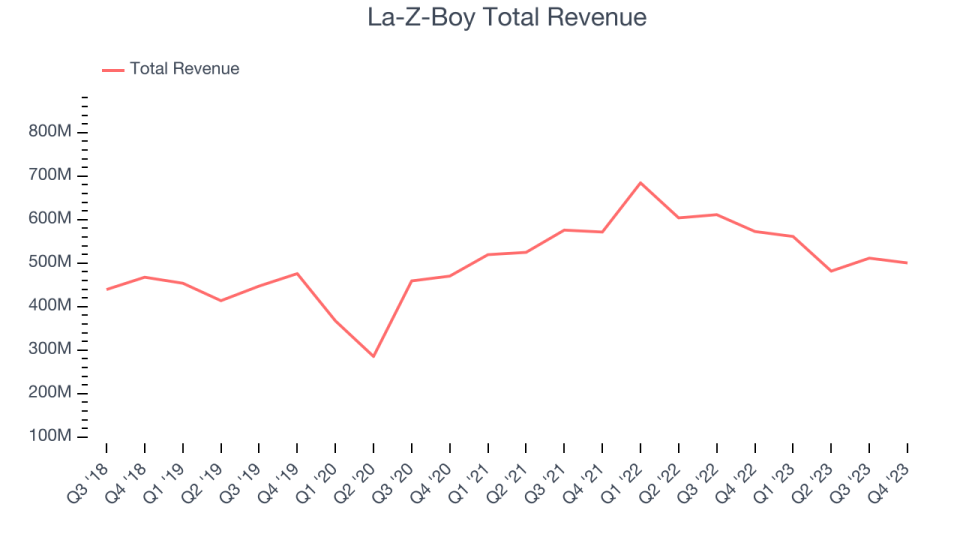

Furniture company La-Z-Boy (NYSE:LZB) fell short of analysts' expectations in Q3 FY2024, with revenue down 12.6% year on year to $500.4 million. It made a non-GAAP profit of $0.67 per share, down from its profit of $0.91 per share in the same quarter last year.

Is now the time to buy La-Z-Boy? Find out by accessing our full research report, it's free.

La-Z-Boy (LZB) Q3 FY2024 Highlights:

Revenue: $500.4 million vs analyst estimates of $523.1 million (4.3% miss)

EPS (non-GAAP): $0.67 vs analyst expectations of $0.72 (7.4% miss)

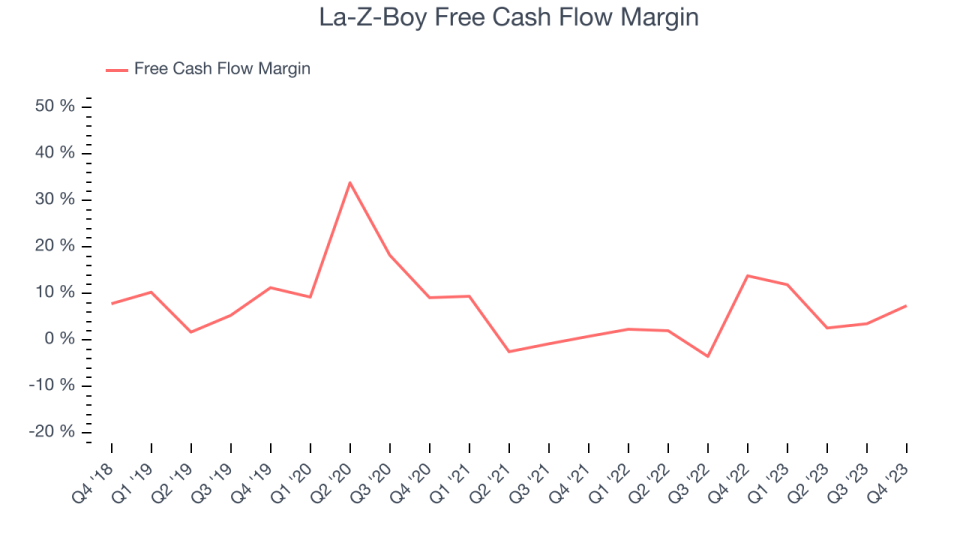

Free Cash Flow of $36.95 million, up 106% from the previous quarter

Gross Margin (GAAP): 42.6%, down from 43.2% in the same quarter last year

Market Capitalization: $1.63 billion

Melinda D. Whittington, President and Chief Executive Officer of La-Z-Boy Incorporated, said, “We remain optimistic about the mid-to-long-term growth potential for our industry, given structural housing shortages and the expectation of improvements in interest rates and housing affordability, and our ability to disproportionately grow with the consumer. In the near term, despite the furniture and home furnishings industry being in a sustained slowdown, our La-Z-Boy Furniture Galleries® network is executing well. Results in January, the third month of our quarter, were negatively impacted by winter weather events, which caused reduced store traffic throughout much of the central U.S. and delivery and production delays at our U.S.-based assembly facilities, the source of the majority of our customized upholstery finished product. After January’s weather disruptions, production and deliveries are now back to normal as we focus on servicing our customers and consumers with the high quality, comfortable products they expect from us.”

The prized possession of every mancave, La-Z-Boy (NYSE:LZB) is a furniture company specializing in recliners, sofas, and seats.

Home Furnishings

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. La-Z-Boy's annualized revenue growth rate of 3.7% over the last five years was weak for a consumer discretionary business.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. La-Z-Boy's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 3.2% over the last two years.

We can better understand the company's revenue dynamics by analyzing its most important segments, Wholesale and Retail, which are 63.5% and 36.5% of core revenues. Over the last two years, La-Z-Boy's Wholesale revenue (sales to retailers) averaged 4.3% year-on-year declines. On the other hand, its Retail revenue (direct sales to consumers) averaged 8.4% growth.

This quarter, La-Z-Boy missed Wall Street's estimates and reported a rather uninspiring 12.6% year-on-year revenue decline, generating $500.4 million of revenue. Looking ahead, Wall Street expects sales to grow 2.8% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, La-Z-Boy has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 4.8%, subpar for a consumer discretionary business.

La-Z-Boy's free cash flow came in at $36.95 million in Q3, equivalent to a 7.4% margin and down 53.3% year on year. Over the next year, analysts predict La-Z-Boy's cash profitability will fall. Their consensus estimates imply its LTM free cash flow margin of 6.5% will decrease to 5.4%.

Key Takeaways from La-Z-Boy's Q3 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its EPS fell short of Wall Street's estimates. Overall, the results could have been better. The stock is flat after reporting and currently trades at $37.75 per share.

So should you invest in La-Z-Boy right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.