Lamb Weston (NYSE:LW) Exceeds Q2 Expectations

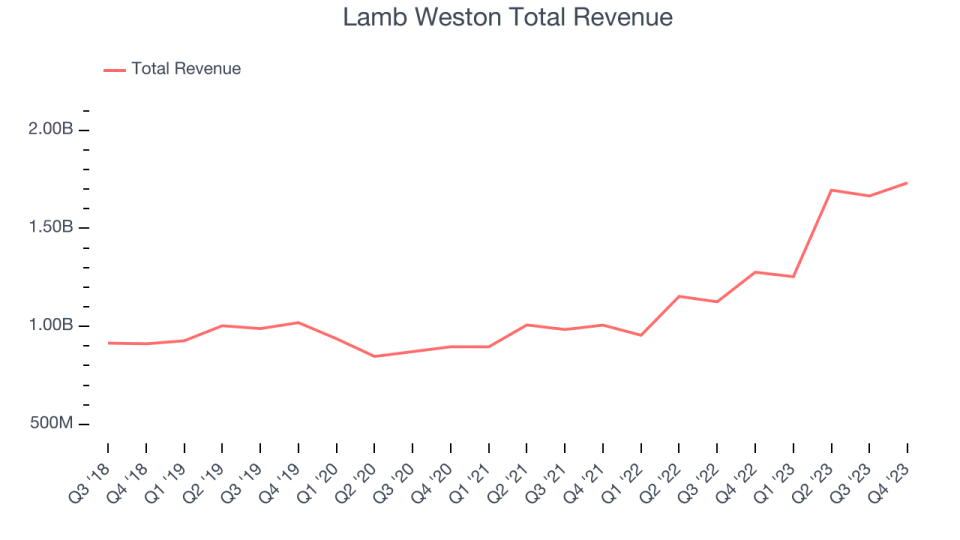

Potato products company Lamb Weston (NYSE:LW) announced better-than-expected results in Q2 FY2024, with revenue up 35.7% year on year to $1.73 billion. The company expects the full year's revenue to be around $6.9 billion, in line with analysts' estimates. It made a non-GAAP profit of $1.45 per share, improving from its profit of $1.28 per share in the same quarter last year.

Key Takeaways from Lamb Weston's Q2 Results

We were glad its revenue and EPS outperformed Wall Street's estimates. Note that revenue growth numbers this quarter--which might strike you as unusually high--included the consolidation of a joint venture, a transaction that was completed in February 2023. Looking forward, while revenue guidance was maintained from the previous outlook, EPS guidance was raised. Zooming out, we think this was a decent quarter, showing that the company is staying on track. The market was likely expecting more, and the stock is down 1.4% after reporting, trading at $103.51 per share.

Is now the time to buy Lamb Weston? Find out by accessing our full research report, it's free.

Lamb Weston (LW) Q2 FY2024 Highlights:

Market Capitalization: $15.21 billion

Revenue: $1.73 billion vs analyst estimates of $1.70 billion (1.9% beat)

EPS (non-GAAP): $1.45 vs analyst estimates of $1.42 (2.4% beat)

The company reconfirmed its revenue guidance for the full year of $6.9 billion at the midpoint, but raised it EPS guidance for the full year

Free Cash Flow was -$119.7 million, down from $67.3 million in the previous quarter

Gross Margin (GAAP): 27.5%, down from 29.9% in the same quarter last year

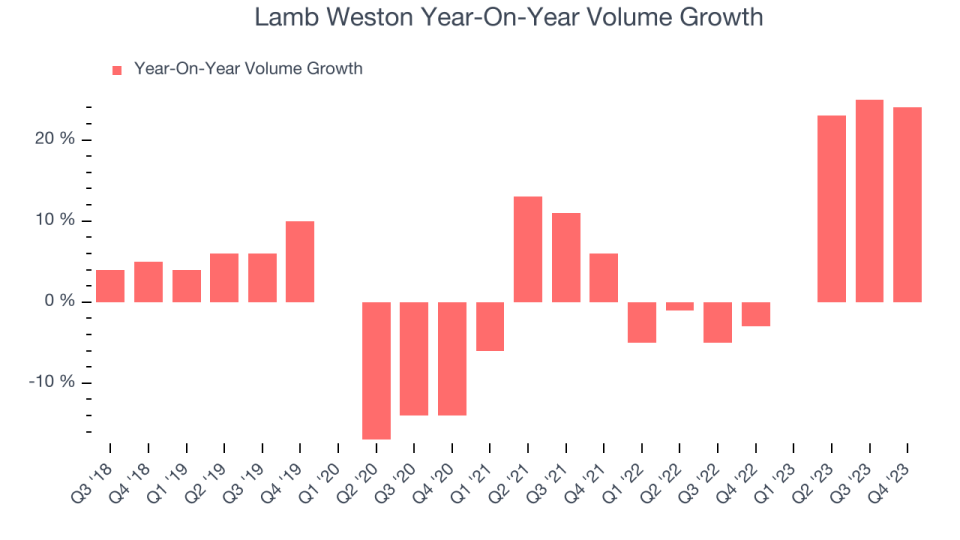

Organic Revenue was up 36% year on year (includes consolidation of joint venture, a transaction that was completed in February 2023)

Sales Volumes were up 24% year on year (includes consolidation of joint venture, a transaction that was completed in February 2023)

“We delivered solid financial results in the quarter by executing well across our customer channels in North America and in our key international markets,” said Tom Werner, President and CEO.

Best known for its Grown in Idaho brand, Lamb Weston (NYSE:LW) produces and distributes potato products such as frozen french fries and mashed potatoes.

Packaged Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods, prepared meals, or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

Lamb Weston is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

As you can see below, the company's annualized revenue growth rate of 21.3% over the last three years was exceptional as consumers bought more of its products.

This quarter, Lamb Weston reported wonderful year-on-year revenue growth of 35.7%, and its $1.73 billion in revenue exceeded Wall Street's estimates by 1.9%. Looking ahead, Wall Street expects sales to grow 11.4% over the next 12 months, a deceleration from this quarter.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Lamb Weston generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Lamb Weston's average quarterly volume growth was a robust 7.2%. Even with this splendid performance, we can see that most of the company's gains have come from price increases by looking at its 28% average organic revenue growth. Note that recent growth has been unusually high because these numbers include the consolidation of a joint venture, a transaction that was completed in February 2023. The ability to sell more products while raising prices indicates Lamb Weston enjoys inelastic demand.

In Lamb Weston's Q2 2024, sales volumes jumped 24% year on year. This result was a well-appreciated turnaround from the 3% year-on-year decline it posted 12 months ago, showing the company is heading in the right direction.

So should you invest in Lamb Weston right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.