Is Las Vegas Sands Stock a Buy?

Las Vegas Sands Corp (NYSE: LVS) is the most valuable gaming company in the world, due largely to its strong market position in Asia. The company is a leader in Macau and has one of only two gaming licenses in Singapore.

Being an industry leader is great, but it doesn't necessarily make Las Vegas Sands' stock a buy. Here's a look at whether this stock is a good buy now or already priced for perfection.

Image source: Las Vegas Sands.

All eyes on Asia

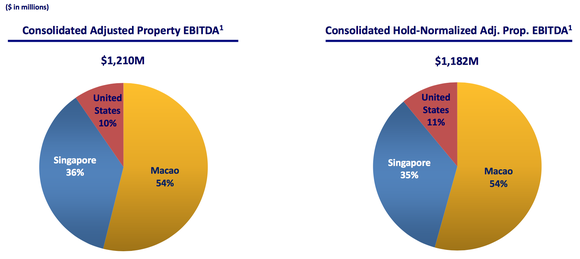

You can see in the graphic below that Las Vegas Sands gets the vast majority of its revenue and EBITDA -- a proxy for cash flow from a casino/resort -- from Asia.

Las Vegas Sands revenue (left) and EBITDA (right) by region. Image source: Las Vegas Sands.

That's been a lucrative position for Las Vegas Sands -- casinos in Macau and Singapore generate much more gaming revenue than Las Vegas. In the third quarter, for example, The Venetian Las Vegas generated $111 million in casino revenue, the Venetian Macau generated $617 million, and Marina Bay Sands in Singapore had $629 million in casino revenue.

The challenge for Las Vegas Sands is that the days of growth may be over. Wynn Resorts (NASDAQ: WYNN), MGM Resorts (NYSE: MGM), and SJM are building, or have recently completed, new properties in Macau that are attracting customers looking for new attractions and amenities. That's what has led to market share losses for Las Vegas Sands.

If Macau grows revenue, as it has recently, the rising tide may allow Las Vegas Sands to grow revenue long-term. But right now the loss of market share could lead to revenue and earnings pressure.

Is the gaming market at a top?

The other factor to consider is that gaming is very strong right now in both the U.S. and Asia, bolstered by growing economies. Ultimately, it's consumers with money to spend that drive revenue for casinos and resorts. If the economy goes into a recession it would be more bad news for Las Vegas Sands.

If the stock were cheap at a high point in the economy that would be one thing, but investors are paying a premium for the company already.

LVS PE Ratio (TTM) data by YCharts

An enterprise value/EBITDA value of 10 is where I start to think of gaming stocks as expensive, and a P/E ratio of 25 is usually reserved for companies with strong growth prospects. That may not be Las Vegas Sands.

The balance sheet is top notch

What Las Vegas Sands does have going for it is one of the best balance sheets in the industry. Net debt is just $9.6 billion, which is low leverage for a company with $4.4 billion in EBITDA over the past year. Even in an economic downturn, Las Vegas Sands would be able to weather the storm better than it could in the last recession when it had much more financial leverage.

Not a buy today

Given the loss of market share in Macau and a reliance on a booming economy, I think the risks for Las Vegas Sands outweigh the potential rewards. As a result, I don't think the stock is a buy. It's just too expensive for me to jump into today.

More From The Motley Fool

6 Years Later, 6 Charts That Show How Far Apple, Inc. Has Come Since Steve Jobs' Passing

Why You're Smart to Buy Shopify Inc. (US) -- Despite Citron's Report

Travis Hoium owns shares of Wynn Resorts. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.