This Leading Medical Supply Distributor Is Facing Headwinds

Delivering medical supplies to hospitals would seem to be a simple and successful recurring revenue business model, but it is not always that easy. The leader in this field is Owens & Minor Inc. (NYSE:OMI), a large global health care solutions company that integrates medical product manufacturing and delivery, home health supply and surgical-related services to support patient care in a hospital setting and in the home.

The company operates through two segments: Global Solutions and Global Products.

The Global Solutions segment distributes a portfolio of medical products and services to health care providers and manufacturers.

The Global Products segment manufactures and sources medical surgical products for the prevention of health care-associated infections, typically in acute care settings. Products include sterilization wraps, surgical drapes and gowns, facial protection products, protective apparel, medical exam gloves and minor procedure kits.

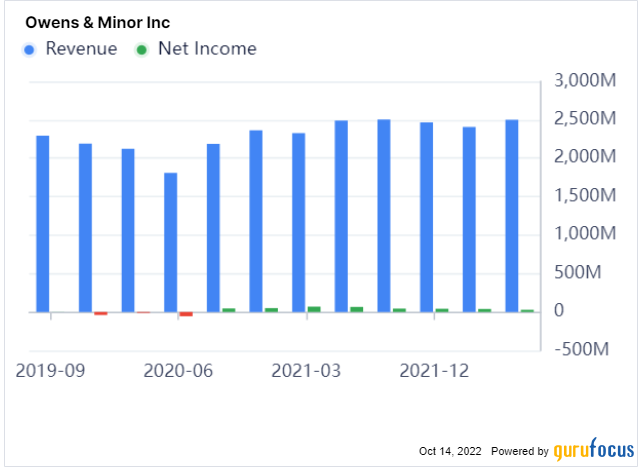

Owens & Minor has been operating continuously since 1882 from Richmond, Virginia and is expected to generate $9.8 billion in revenue in 2022. The company currently has a market capitalization of $1.2 billion.

Acquisitions

Throughout most of its history, Owens & Minor has operated as a pure distributor of medical supplies to health care facilities. This is typically a low-margin, pass-through type business, so, in 2018, the company acquired a product line from Halyard, which put it in the manufacturing and product business. The total acquisition cost was $710 million.

In 2022, the company acquired Apria for $1.6 billion. Apria produces medical products related to home respiratory, obstructive sleep apnea and negative pressure wound therapy.

These acquisitions were funded by cash and debt and left the company with very leveraged balance sheet.

Financial review

Owens & Minor reported its financial results for the second quarter on Aug. 3, which were largely in line with expectations. Revenue growth for the three months ended June 30 was essentially flat at $2.5 billion, with the product portfolio showing the most strength as Byram revenue gained 17% and Apria revenue showed 4.4% growth. The adjusted Ebitda was $156 million and the Ebitda margin came in at 6.2%, an increase of 110 basis points.

The company carries $2.6 billion in total debt and $56.4 million in cash and equivalents. With $530 million in expected Ebitda, the companys leverage ratio is high at 4.8. In the second quarter, interest expense ate up almost half of operating income. Nonetheless, the company was able to reduce debt outstanding by $69 million.

In a statement, Owens & Minor President and CEO Edward Pesicka said, "Looking to the balance of the year, we have considered the accelerating macroeconomic headwinds, as well as the unique labor and product availability challenges within acute care resulting in lower overall hospital volume. In recognition of these factors, we have revised our full-year 2022 outlook. However, in our view, the economic landscape and industry-specific challenges will eventually improve, returning hospital procedure volumes to normalized levels. Because we have the right strategy and operating model, as well as a proven business system, I am confident in our ability to successfully manage through these challenges over time."

On Oct.12, the company announced an unexpected management departure and lowered annual guidance once again. The company now expects adjusted earnings per share in the range of $2.50 to $2.60 and Ebitda of approximately $532 million. It blamed unfavorable macro conditions and lower-than-expected hospital procedure volume.

Valuation

Consensus analysts earnings per share estimates for 2022 are roughly $2.50 and for 2023, the estimate is $2.60. These low single-digit price-earnings ratios are not that meaningful as they do not account for the large debt load. The estimated enterprise value/Ebitda ratio is 7.2 for this year.

The GuruFocus discounted cash flow calculator creates a value of $31 using a long-term growth rate of 5% and a discount rate of 10%. The current share price seems to imply zero growth going forward.

The company pays a small token dividend of one cent per year, which is only a 0.07% dividend yield. On a price-sales basis, the company is trading at only 12% of revenue.

Guru trades

Gurus who purchased Owens & Minor stock during the second quarter included Steven Scruggs (Trades, Portfolio), Jeremy Grantham (Trades, Portfolio), Steven Cohen (Trades, Portfolio) and First Eagle Investment (Trades, Portfolio). Among those who sold or reduced their positions were Paul Tudor Jones (Trades, Portfolio), Jim Simons (Trades, Portfolio)' Renaissance Technologies and Catherine Wood (Trades, Portfolio).

Conclusion

Owens & Minor is facing many risks and headwinds, such as negative pricing actions, lower hospital procedure volumes after the Covid-19 pandemic, increased competition by potential players such as Amazon (NASDAQ:AMZN) and the failure to integrate recent acquisitions.

However, these risks are likely already priced into the stock as it is selling at 52-week lows and is down 71% from recent highs. As patient volumes turn around and debt paydown continues in a meaningful way, there is likely strong upside in Owens & Minor stock from these depressed levels.

This article first appeared on GuruFocus.