Lindsay Corp: A Value Trap in the Making

About the company

Lindsay Corp. (NYSE:LNN) is a leading provider of specialized water management and road infrastructure products and services. With two distinct reporting segments, Irrigation and Infrastructure, the company caters to the needs of both the agricultural and transportation industries.

The Irrigation segment, which accounts for 87% of Lindsay's total revenue, focuses on manufacturing center pivot, lateral move and hose reel irrigation systems. These advanced systems are primarily utilized in the agricultural sector to efficiently distribute water and enhance crop yields. Additionally, Lindsay also manufactures and markets repair and replacement parts for their irrigation systems, ensuring continued support and maintenance for customers.

In the Infrastructure segment, which comprises 13% of the company's total revenue, the company manufactures a range of essential products such as moveable barriers, specialty barriers, crash cushions and end terminals, which contribute to road safety and traffic management. The company also produces road marking and road safety equipment, as well as railroad signals and structures, playing a crucial role in maintaining and improving transportation infrastructure.

A stock in decline

Lindsay's stock price has experienced a decline since November 2022. This can be attributed to various factors, including a slowdown in top-line growth. The uncertainty surrounding farm income, higher cost inflation and rising interest rates have impacted the demand for Lindsay's products and services. As a result, the stock has experienced a decline of approximately 34% between November 2022 and the writing of this article, while the S&P 500 has shown a 9% increase during the same period.

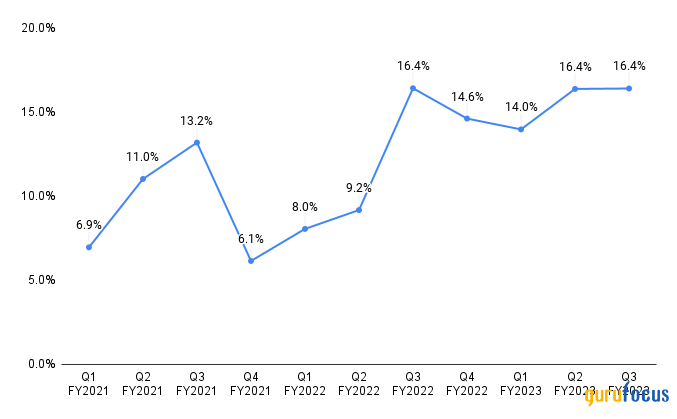

In its third quarter of fiscal 2023, Lindsay witnessed a 23% year-over-year decline in revenue, amounting to $164.6 million. This decrease can be attributed to lower volumes in the irrigation segment, as farmers opted to delay their capital investment decisions. Despite the revenue decline, Lindsay managed to maintain its operating margin at 16.4% due to a favorable product mix and improved price realization.

Top line analysis and outlook

Lindsay witnessed robust growth in both the 2021 and 2022 fiscal years, benefiting from higher net farm income driven by increased agricultural commodity prices. However, the company is currently facing challenges as agricultural commodity prices have declined from their peak in May 2022, leading to a decrease in overall revenue growth. In the third quarter of 2023, the irrigation segment experienced a significant decline in revenue, dropping by 24.5% year-over-year. The North America irrigation market witnessed a decline of 22%, primarily due to lower volumes, while the average selling price remained comparable to the previous year. On the international front, the irrigation market suffered a 27% year-over-year decline, mainly attributed to reduced sales volumes in countries such as Brazil, Australia, Ukraine and Russia compared to the third quarter of the previous year.

The Infrastructure segment also faced a decline in the top line in the last two quarters, largely due to lower sales of Road Zipper projects and road safety products. The anticipated increase in road construction and project activity, supported by higher U.S. infrastructure spending, has been slower to materialize due to delays in project startup, partly caused by slower-than-expected releases of public funding.

Looking ahead, the North America irrigation market is experiencing tepid farmer sentiment, influenced by factors such as inflation, interest rates, general economic uncertainty and lower commodity prices. This is likely to continue affecting Lindsay's top-line growth in the coming quarters, as customers adopt a cautious approach and delay equipment purchases until the profitability of the current crop year becomes more apparent. Additionally, the U.S. Department of Agriculture forecasts a 16% year-over-year decline in farm income to $136.9 billion in 2023, further indicating a potential slowdown in the purchase of farm equipment. Similar market fundamentals are impacting the international irrigation market, including lower agricultural commodity prices and a decline in net farm income. In the infrastructure business, revenue will continue to be affected by delays in project startup and slower-than-expected releases of public funding, hampering the anticipated increase in road construction and project activity.

Margin outlook

Despite facing challenges in top-line growth, Lindsay has shown improvement in its margins. In the recent quarter, the operating margin remained steady year-over-year at 16.5%, but it has exhibited consistent improvement over the past six quarters. This positive trend can be attributed to several factors, including higher price realization, an enhanced product mix and moderate inflationary cost pressures.

It is worth noting that Lindsay's margins were initially affected by the LIFO method of accounting for inventory. Under this method, the latest raw material prices are recognized in the cost of goods sold rather than in the ending inventory, creating a headwind during periods of rising raw material prices. However, as inflationary pressures begin to moderate, the company's margins should continue to improve. The previously encountered LIFO headwind during an inflationary raw material environment should transition into a tailwind as raw material prices correct. Additionally, the pricing actions implemented by Lindsay over the last few quarters are anticipated to contribute to margin enhancement. The company's focus on improving productivity and actively seeking opportunities to grow margins further underscores its commitment to sustainable profitability.

Valuation

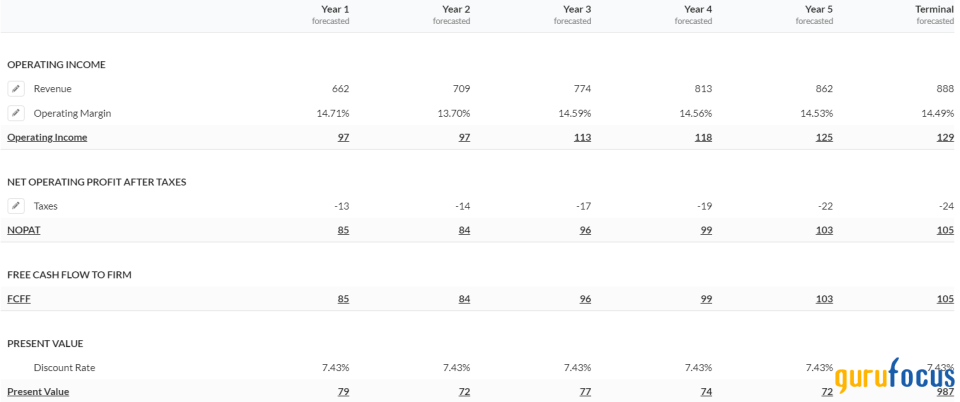

In my discounted cash flow (DCF) calculations, I assume revenue to decline in the double digits in 2023, given the weak irrigation and infrastructure markets. Beyond 2023, I have assumed growth to be in the high-single digits, with a terminal growth rate in the mid-single digits, as the company will continue to benefit from funding from government benefits, improvements in farm income and new product development. I used a discount rate of 7.43% and arrived at a fair value estimate of $125.79.

Conclusion

To summarize, I believe the near-term outlook for Lindsay suggests that its top line will continue to face challenges due to weakness in both the irrigation and road safety markets. However, there is potential for improvement in the company's margins, driven by factors such as the moderation of inflationary cost pressures, pricing actions and productivity initiatives. Considering the current market conditions and the aforementioned factors, I do not believe Lindsay offers compelling value at its current levels as my fair value estimate is not much higher than the stock price as of this writing.

This article first appeared on GuruFocus.