Live Nation (NYSE:LYV) Delivers Strong Q4 Numbers

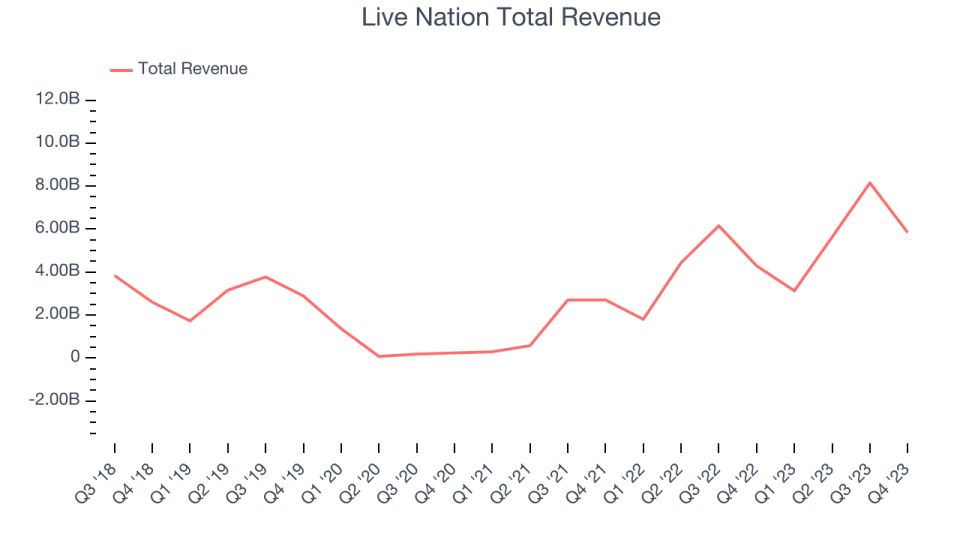

Live events and entertainment company Live Nation (NYSE:LYV) reported Q4 FY2023 results beating Wall Street analysts' expectations , with revenue up 36.1% year on year to $5.84 billion. It made a GAAP loss of $0.79 per share, improving from its loss of $1.02 per share in the same quarter last year.

Is now the time to buy Live Nation? Find out by accessing our full research report, it's free.

Live Nation (LYV) Q4 FY2023 Highlights:

Revenue: $5.84 billion vs analyst estimates of $4.78 billion (22.1% beat)

EPS: -$0.79 vs analyst estimates of -$1.04 (23.9% beat)

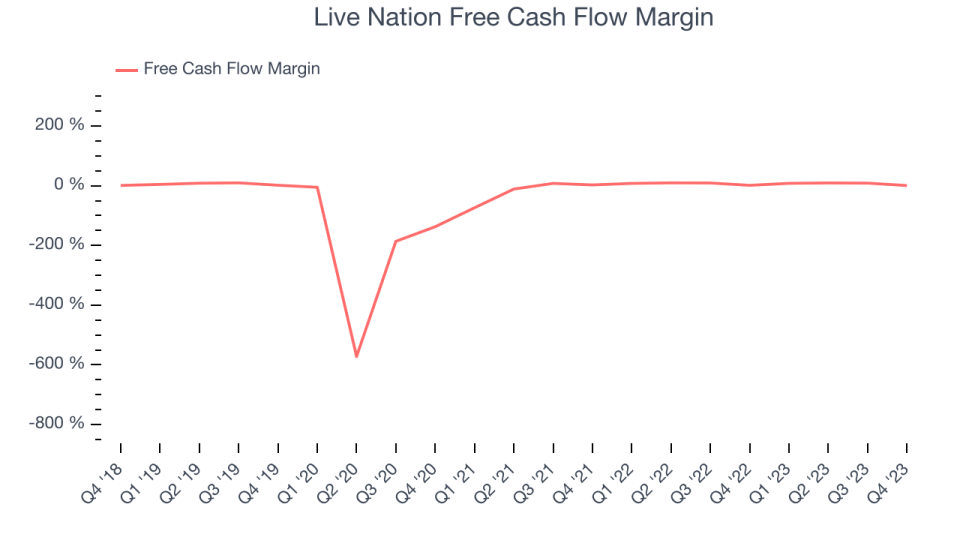

Free Cash Flow of $40.4 million, down 94.3% from the previous quarter

Gross Margin (GAAP): 19.8%, down from 23.3% in the same quarter last year

Market Capitalization: $20.82 billion

"The live music industry reached new heights in 2023, and demand for live music continues to build. Our digital world empowers artists to develop global followings, while inspiring fans to crave in-person experiences more than ever. At the same time, the industry is delivering a wider variety of concerts which draws in new audiences, and developing more venues to support a larger show pipeline. Against this backdrop, we expect all our businesses to continue growing and adding value to artists and fans as we deliver double-digit operating income and AOI growth again this year, with our profitability compounding by double-digits over the next several years."

Owner of Ticketmaster and operator of music festival EDC, Live Nation (NYSE:LYV) is a company specializing in live event promotion, venue management, and ticketing services for concerts and shows.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Live Nation's annualized revenue growth rate of 16.1% over the last five years was solid for a consumer discretionary business.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Live Nation's healthy annualized revenue growth of 90.5% over the last two years is above its five-year trend, suggesting its brand resonates with consumers.

This quarter, Live Nation reported wonderful year-on-year revenue growth of 36.1%, and its $5.84 billion of revenue exceeded Wall Street's estimates by 22.1%. Looking ahead, Wall Street expects sales to grow 3.2% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Live Nation has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 6.9%, subpar for a consumer discretionary business.

Live Nation broke even from a free cash flow perspective in Q4. This quarter's result was in line with its margin in same period last year. Over the next year, analysts' consensus estimates show they're expecting Live Nation's LTM free cash flow margin of 6.7% to remain the same.

Key Takeaways from Live Nation's Q4 Results

We were impressed by how significantly Live Nation blew past analysts' revenue expectations this quarter. We were also excited its EPS outperformed Wall Street's estimates. Qualitative commentary about the start of 2024 was also bullish, although the company did not provide specific revenue, adjusted EBITDA, or EPS guidance for the current year. Zooming out, we think this was a great quarter that shareholders will appreciate. The stock is up 4.3% after reporting and currently trades at $97.53 per share.

Live Nation may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.